Invest Like a Woman and Become a Millionaire by Investing

Want to know the secret to building wealth as a woman investor? Here’s a surprising truth: women outperform male investors by 0.4% annually, according to Fidelity’s research on over 5 million investors. Yet despite this proven success, 58% of women report lacking confidence in their investment decisions. If you’re ready to overcome investment anxiety and start building real wealth—this guide reveals the exact investment strategy for women that has helped countless female investors achieve millionaire status by retirement. As a former portfolio manager and university finance instructor with decades of investing experience, I’ll show you why investing for women beginners is simpler than you think, and how you can start today with a proven, low-stress approach that actually works.

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

Key Takeaways: Investment Strategy for Women

In this comprehensive guide, you’ll discover:

✅ Why women are naturally better investors – and how to leverage your strengths for maximum returns.

✅ The simple 6-step investment strategy that beats 80% of professional fund managers (without the complex jargon).

✅ How to become a millionaire by 65 – starting at age 40 with just $1,236 per month in strategic investments.

✅ Best investment tips for women beginners – including exact fund recommendations with fees under 0.05%.

✅ How to invest with confidence – even if you’ve never opened a brokerage account before

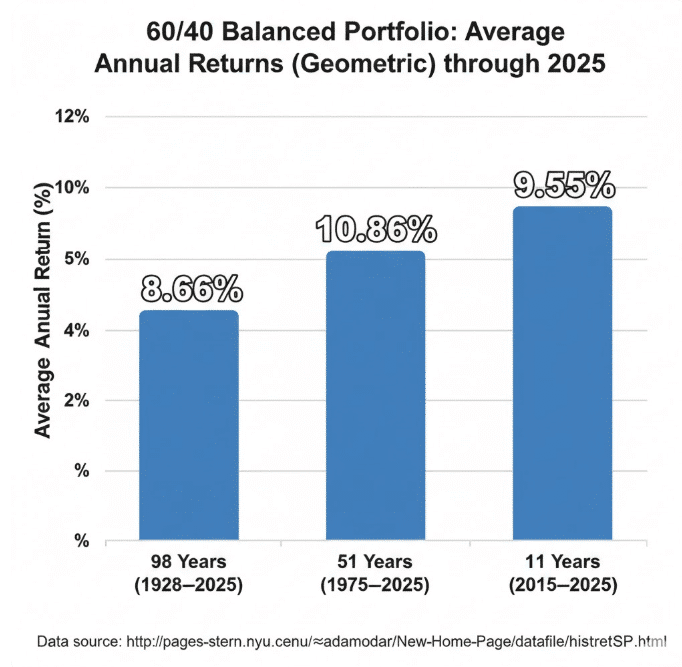

✅ Asset allocation secrets – the 60/40 portfolio strategy that generated 8.66% average annual returns over 97 years

✅ Free tools and calculators – to help you start investing today, no financial advisor required

Bottom line: You don’t need to be a finance expert to build lasting wealth. Women who follow these proven strategies consistently outperform men—and I’ll show you exactly how to start investing for women in 2026 with confidence and clarity.

What is the Best Investment Strategy for a Woman?

Long term, investing in the financial markets is a brilliant way to build wealth. Investing in a diversified portfolio of low fee index funds, in line with your risk tolerance, leads to long term wealth. Although female investors might lack confidence in managing an investment portfolio, women’s past investment performance typically surpasses that of their male counterparts. Simple investment strategies like passive index fund investing, outperforms active trading and attempting to time the markets.

Women investors, striving for financial security benefit from creating a financial plan and understanding investment history. Women who understand investment history, gain confidence and are less likely to flee the markets after the occasional stock market decline.

Data source; http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html

For the past 97 years, stocks returned 10.02%, bonds, 6.62% and cash 3.32%. In every subsequent period, you’ll the stock market, dominated returns, with bonds and cash following. Clearly, to meet your financial goals, women must understand that the stock market has delivered the highest long-term returns, albeit with the greatest amount of volatility.

In reality, many investors do not achieve the average annualized return over time on their long term stock investments, because they trade in and out of the markets. Fortunately, women investors are more likely to stay the course and not attempt to outperform the investment markets. Investors with the lowest returns tend to sell after a loss and buy back in after the investment rebounds, leading to sub par returns.

Consider WiserAdvisor if you’re looking for help with investing:

6 Investment Tips for Womeninners

1. Invest for the long term. If you cannot leave your money in a stock index fund, for at least 8-10 years, do not invest. Markets are volatile and over the short term, your returns are random. Over the long term if you believe U.S. and global companies will grow and prosper, then their underlying stocks will advance as well.

2. Cut investment expenses to the bone. Realize that investment expenses are taken off the top. If you invest in a managed mutual fund charging 1% per year, then out of every $1,000 you invest, only $990 is going towards building wealth. Many low fee index ETFs charge negligible fees. For example, VTI, Vanguard Total Market Index ETF and BND, Vanguard Total Bond ETF charge, 0.03% per year while the category average is 0.33+%. Less money toward annual management fees means more money in your pocket.

3. Don’t fight the market. Accept the fact that it is highly unlikely that you will beat the market, so choose diversified low fee investment funds for your portfolio. Active investors, those that think they can beat the average market returns by buying and selling, typically deliver lower returns than passive, lazy, index fund investors.

4. Choose your asset allocation carefully. Divide your investment pie among stock index mutual funds or ETFs, and fixed income investments like bonds and cash. Plan your investment pie according to how much risk or volatility you can stomach. If you are risk averse and don’t like the ups and downs in value of stock investments then place a smaller percent in those types of financial assets and skew your asset allocation toward a greater percent in bonds and fixed income assets.

For low fee model portfolios, check out one of my favorite investment platforms, M1 Finance.

Automatically invest for retirement with a tax-advantaged brokerage account. Custom-build your portfolio or choose a pre-made Expert Pie based on your long-term goals.5. Stick with your plan through market downturns. No one has a problem when their investment values surge. The problem comes when fear kicks in and you get scared during market downturns. I know more than a few folks who let fear get the best of them and sold during market downturns only to miss the subsequent rebound.

If you sell during a market downturn, you have to be right twice, once when you sell and another time when you buy back in.

6. Seek investment advice from a financial advisor or robo-advisor. Financial advisors can offer support with your investment decisions including crafting long term goals and saving strategies. Ellevest offers a low-fee robo-advisor with access to discounted financial advisory advice. While WiserAdvisor will match you with three fee-only, vetted financial advisors.

Women, Become a Millionaire in 25 Years of Investing

Here’s how women can become millionaires by investing, even when you start at age 40.

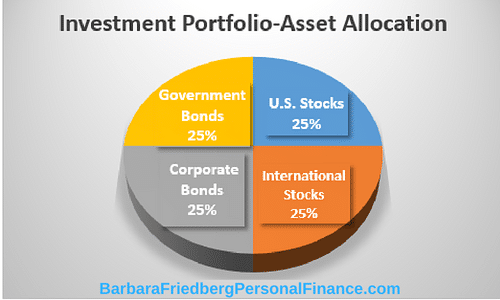

Women, become a millionaire by age 65, even if you have not begun investing and have nothing saved at age 40. A woman could start investing $1,236 per month in a portfolio equally divided between a U.S. stock index fund, an international stock index fund, and a diversified bond fund. You can choose a mutual fund or an ETF.

Review; Quicken vs. Empower – Which is the Best Money Management Tool?

Assume historical returns prevail. If you earn 6.9% annually, then at the end of 25 years, your $370,800 investment will be worth $1,000,000.

Of course, if you start investing younger, you can achieve $1,000,000 with less money.

Start at age 25 and you only need to invest $385 per month to achieve $1,000,000 by retirement. And if your employer kicks into your 401k retirement account, you can invest less and still reach $1,000,000 or more by retirement.

Asset allocation secrets

Women, here’s the the 60/40 portfolio strategy that generated 8.66% average annual returns over nearly 100 years.

Invest 60% of your portfolio in a diversified stock ETF, similar to this all-world stock fund by Vanguard (VT). Invest the remaining 40% in a diversified bond ETF such as Vanguard Total Bond Market ETF (BND).

The recent decade and the 50-year annualized returns of the 60/40 balanced portfolio enjoyed tremendous growth, due to the robust stock market returns. Despite periodic market declines, those smart women investors (and men) who chose a conservative asset allocation, reinvested dividends and stayed invested over decades, built significant wealth.

Women Investing Resources

Here’s some help to get you started with your investing:

- Best Investment Advice for Millennial Women

- Free microbook; How to Invest and Grow Your Wealth

- Free budgeting, cash management, retirement planning, investing dashboard (I use this myself). Sign up required. Sponsored by Empower.

FAQ

The best investment for a woman is a well diversified stock and bond market portfolio. For example, depending upon your risk tolerance, and age, you might invest 70% in an all world stock market ETF like VT, and 30% in a broadly diversified bond fund like BND. Read more about asset allocation in this free microbook.

Open a Roth IRA and invest in a broad US or US and International stock ETF. You might choose either the Vanguard Total US Market ETF, VTI, or Vanguard’s all-world ETF VT. Since this investment is for long term growth, you can expect high single digit annualized returns over the upcoming decades. .

A 2018 MassMutual Womens Risk Survey found that women typically invest in diversified portfolios and take on less risk than men. Extrapolating from this research, you might expect women to invest in stock and bond fund portfolios, in line with their risk tolerance levels. This might include target date funds or passively managed stock and bond index funds. Women also gravitate towards investing with financial advisors, according to the MassMutual Survey.

If your workplace offers a 401k or a 403b account, that is an ideal vehicle for your investments. Within that retirement account, you might choose a target date fund or several low-fee passively managed stock and bond mutual funds. It’s also helpful for new investors to familiarize themselves with the investment basics. You can learn more about how to invest in this free microbook called Invest and Grow Your Wealth or other investment information websites such as Investopedia or Morningstar.

Women can invest with little money with free apps like Acorns. Set the round ups feature to divert up to $10 into an investment account, every time you spend. If your employer has a 401k or 403b plan, divert as much as you can into that investment vehicle every pay period. Your employer frequently matches your contribution, up to a certain percent of your salary. Or, open a Roth or Traditional IRA and set up a regular transfer from your bank account into an investment account.

How to Start Investing for Women Roadmap

Developing the best personal investment strategy for women isn’t about chasing the latest crypto craze or predicting the next market peak—it’s about consistent, evidence-based habits that protect your financial future. As we navigate the current economic landscape, the fundamentals of building wealth for women (and men) remain centered on low-cost index funds, smart asset allocation and tax-advantaged accounts like a Roth IRA or 401(k). By automating your contributions and maintaining a diversified portfolio, you can combat inflation and rising healthcare costs while ensuring your money works as hard as you do. Whether you are starting with $1,000 or $100,000, the secret to becoming a millionaire is simple: stay the course, minimize fees, and let the power of compounding turn your small monthly investments into a lasting legacy.

Related

Sources:

https://www.massmutual.com/global/media/shared/doc/mm-womens-risk-study.pdf

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.

3 thoughts on “How To Start Investing For Women ”

Thank You for sharing this amazing article as I was looking to Invest.

Really great information, thanks for sharing this.

Hi Barbara,

This is Brij.

If you are at my life stage who has lots of ETFs in both the Rollover and Roth Accounts. How to cut down to Make like your portfolio?

Comments are closed.