Are Your Investment Returns Good or Bad?

Do you know how well your investments are performing?

Are you wondering if a 10% return is good or bad?

Do you know the annual rate of return of your investments?

What about how well your investments are performing when compared with a standard benchmark?

Ever since a friend asked me to look over her investments and tell her if she’s doing well I’ve wanted to help investors answer this question;

“What is a good rate of return and what is a bad rate of return?”

Most individuals don’t know if their investment returns are good or bad. Even investors with financial advisors don’t know how to evaluate their rates of returns. Many financial advisors don’t offer their clients the investment portfolio annual rate of return compared with the returns of unmanaged indexes. And that’s a big problem.

You’re hiring a financial advisor to help you manage your money and get a good annual investment return. Yet, if you don’t know your annual return, or even if you do, you still need to know if that return is good or not.

When managing your own finances, you need to know if you’re making the best investment decisions as well.

What is a Rate of Return?

Your investment rate of return is the percent increase or decrease in the value of your investment, typically over a one year period.

If you invest $1,000 on January 1 and at the end of the year your investment value is $1,100, then you’ve earned a 10% rate of return.

To calculate your rate of return percentage, use this formula, or an online calculator.

Rate of Return = [(New value of investment – Original value of investment)/Original value of investment] x 100

Rate of Return =[($1,100 – $1,000)/$1,000] x 100 = 10%

What is a Good Rate of Return?

The answer is – it depends.

Whether a rate of return is good or bad is relative.

In general, because stocks are riskier, they typically offer higher rates of return than bonds. Since bonds tend to be safer, they will offer lower rates of return.

From 1928 through 2019, the S&P 500 – a proxy for the US stock market – returned over 9% annually. And during that same period, the 10 year US treasury bond returned nearly 5%.

So, using historical stock and bond returns as a guide you might consider that a 9% stock market return and a 5% bond return is a good rate of return.

But, there’s much more to evaluating investment returns than just matching a long term average.

What is a Good Investment Return? – Video

What is a Bad Rate of Return?

Using the example above, you might think that a bad rate of return would be a return lower than the average for the category.

So, if your stock market portfolio returned 5% and your bonds 3% you might think your investment portfolio failed and earned a bad rate of return. But that’s not necessarily true.

A 9% rate of return on your stock portfolio might be considered bad during a year when the S&P 500 index earned 13%.

In contrast a 5% return on your stock portfolio might be a good return, if the S&P 500 lost 4% during the same year.

Is a 10% Return Good or Bad?

Think about Keisha. She was thrilled in January when her advisor-managed all-stock investment portfolio returned 10% during the previous year. She knew that her bank savings account was not earning much, so she rejoiced in what looked like a stupendous 10% return.

Here’s why Keisha should have been disappointed – even though her stock portfolio beat the long term historical stock average.

During the same time, the unmanaged S&P 500 index returned 13.48%. All of a sudden Keisha’s 10% return doesn’t look too good. She thought, why am I paying my investment advisor 1% to manage my stock portfolio for a lower return than the unmanaged S&P 500 index fund?

That’s a legitimate question.

Here’s how Keisha could have gotten close to a 13.48% return in that same year and thereby beaten the returns of her investment manager by 3%.

Whether your return is good or bad depends upon whether you could have gotten a better return with the same amount of risk. And Keisha could have earned a better return, saved money on her investment fees, with the same or less risk.

Passively Managed Index Funds Are the Way to Invest

Years of investing research, Warren Buffett, John Bogle, and Nobel Prize winners agree that most investors would do well to invest in a portfolio of passively managed index funds.

An index mutual or exchange traded fund is a passive investment. It simply mimics the investments in a basket or index of stocks (or bonds). The S&P 500 index is one of the most popular indexes and holds a market capitalization weighted group of large U.S. companies. This index is frequently used to reflect the complete U.S. stock market.

You can buy shares in a fund that mirrors the S&P 500 Index. If you choose to buy index funds for your investment portfolio, your investment returns will approximate that index.

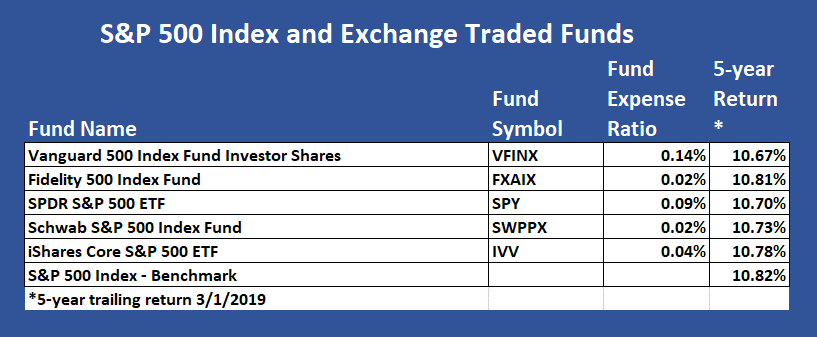

Following are several low-fee S&P 500 index mutual and exchange traded funds (ETFS).

Notice that the returns are similar, with the Fidelity, low-fee fund yielding the highest 5-year return.

When investing in an unmanaged index mutual or exchange traded fund, your returns are slightly less than those of the actual index. The difference in return between the fund return and that of the index is typically explained by the expense ratio.

Although it’s wise to invest in low fee, passively managed index funds, I wouldn’t worry about several hundreds of a percent difference in fees or returns.

Is 10% a good or bad return? The answer is, it depends.

In Keisha’s case, since her advisor invested in a diverse portfolio of U.S. stocks and her return was well below the S&P 500 index returns that year, 10% wasn’t a good return. Had she forgone the advisor and invested all of her stock investment portfolio in one of the above S&P 500 index funds, her return would have been closer to 13.40%. (13.48% index return less a 0.09% fund fee)

Figure Out If You’re Getting a Good or Bad Rate of Return

You shouldn’t look at your investment returns in a vacuum. The return is meaningful only in light of potential returns available for similar investments.

You wouldn’t compare the returns of your all stock portfolio with the annual return of a 50% stock and 50% bond portfolio. That’s because bonds, typically offer a lower rate of return than stock investments.

Here’s a simple approach to figure out whether your investment portfolio is getting a good return or not. The goal is to match or beat an unmanaged index invested in a comparable asset allocation.

You use a benchmark to compare assess your returns because that is an achievable rate of return. Despite how easy it is to invest in a market-matching index fund, most investors fail to reach that benchmark.

Click here for Free micro book-How to Invest and Outperform + Wealth Tips Newsletter

Follow these steps to figure out your investment return:

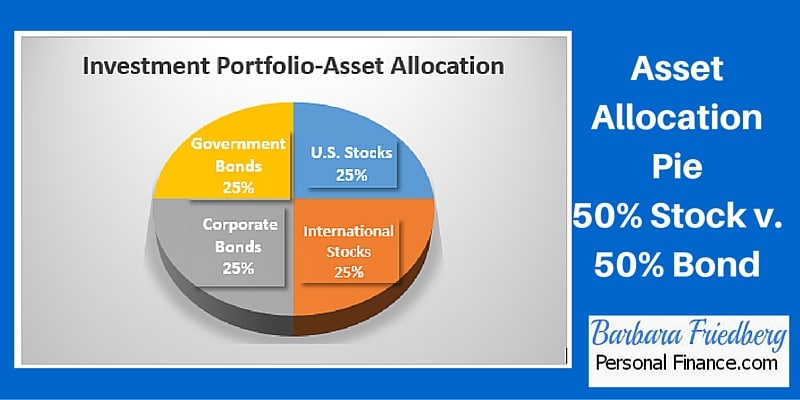

1. Create your asset allocation pie. What percent of your assets (or asset allocation) are in stocks, bonds, and cash? You may need to drill down even further into various types of investments. For example, if you want to go into depth you could examine the percent of your total investment assets are in large capitalization U.S. stocks, developing market international stocks, emerging market stocks, value U.S. stocks, small capitalization stocks etc.

When creating your asset allocation pie, next move on to the fixed portion of your portfolio. Do you have a U.S. bond fund, corporate bond fund, government bond fund, etc.?

The next step is a job for you or your financial advisor.

2. Find out which index funds relate to your asset allocation. In other words, categorize your individual stocks, bonds, and/or funds according to type. For example, imagine that your investment portfolio-asset allocation pie looks like this:

In each of these categories you might have individual stocks and/or mutual funds that fit the category.

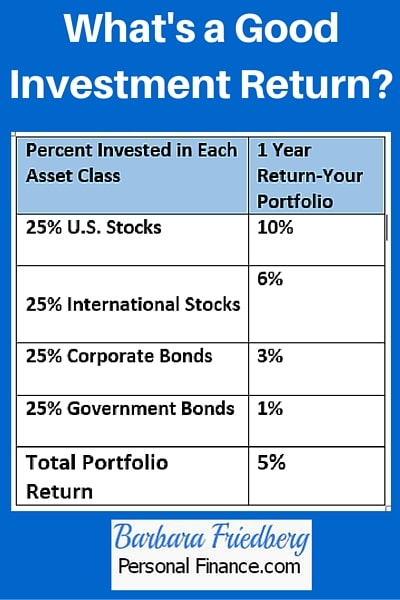

3. Calculate the returns on each of your asset classes and list those alongside the percent invested in each asset category.

Here’s how to calculate rate of return on your portfolio:

Your annual portfolio return is 5%. [(.25 * .10) + (.25 * .06) + (.25 * .03) + (.25 * .01)]

Now, you know your one year investment return is 5%.

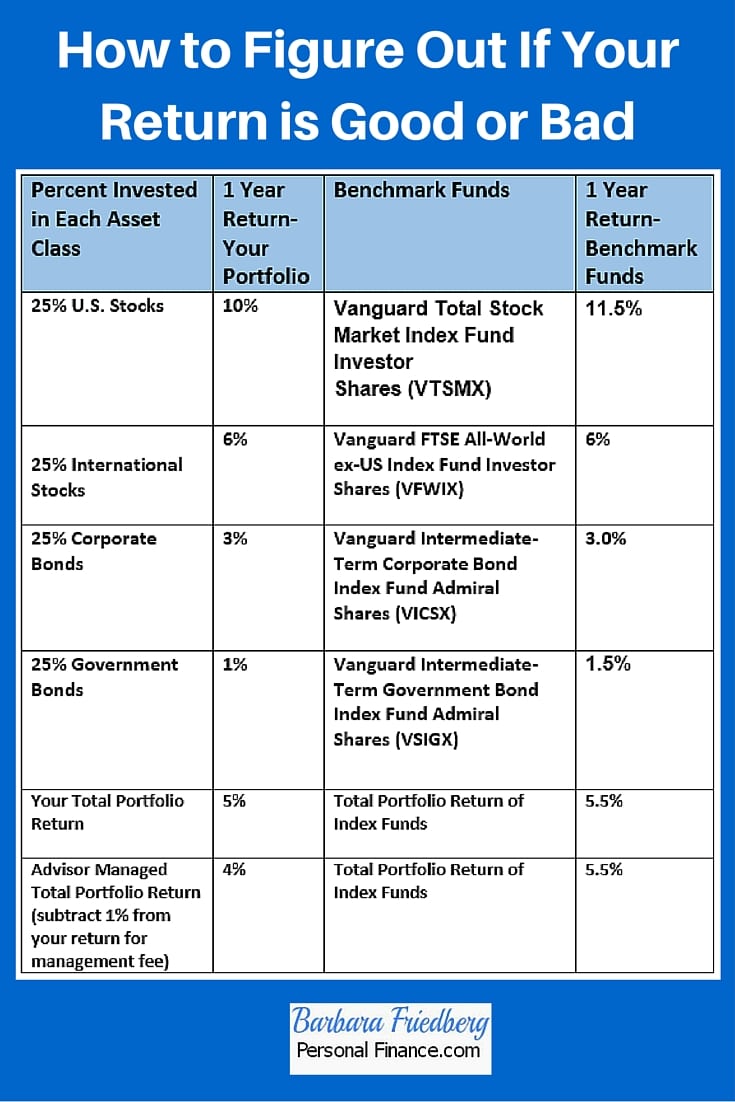

4. Compare your returns with the returns of a benchmark portfolio.

But how do you know whether this is a good or bad return?

As we discussed earlier, you know whether you’re getting a good return if your returns are equal to or better than your portfolio’s comparison benchmark. Since you know your asset allocation pie, all you need to do is find out the benchmark returns.

Following are the hypothetical benchmark returns compared with your returns:

Did You Get a Good or Bad Return?

Now you’re equipped to answer this question. You invested in stocks, bonds and funds and your annual return was 5%. Had you gone the easy route and chosen 4 index funds, in your desired asset allocation, you would have beaten your own returns by 0.5% per year. Your stock picking efforts weren’t rewarded.

Imagine if you had hired a portfolio manager who diversified your investment portfolio, invested in a broad mix of stocks, bonds, and mutual funds and earned a 5% return. But the manager’s fee was 1% and was subtracted from the 5% return. Now your advisor managed fund only earned 4% (5%-1% fee).

Compare your 5% return or the advisor managed 4% return with the 5.5% index fund portfolio return. The unmanaged index fund portfolio outperformed both your own and the advisor managed investments. The results are clear, the passively managed portfolio of index funds outperformed your own and the advisor managed investments.

Is that always the case? You won’t know unless you or your advisor compares your investment portfolio with that of the comparable benchmarks.

You decide if your return is good or bad. The best way to answer that question is to compare your own returns with the returns you might have received on a comparable passively managed index fund portfolio.

If you’d like a free investment manager that offers thousands of funds and stocks, consider investing with M1 Finance.

Click here to read an M1 Finance Review

Click here to go directly to the M1 Finance Website

Related

- What to Invest in if I’m in a High Tax Bracket

- 4 Best Investment Managers to Watch

- How to Save for Retirement at 30 and Become a Millionaire

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.

2 thoughts on “Is a 10% Return Good or Bad? What is a Good Investment Return?”

Hi Barbara My name is Dean Richards I am 61 years old I have about $400,000 I would like to invest. I would like to get about $5000 – $6000 per month income can you help me . I have my money in a solo 401k thru Nabers group. I am looking for safe, but it sound like I can invest in anything.

Hi Dean, Thank you for writing in. You’ve raised an important question. $400,000 is a sizeable nest egg, congratulations. Unfortunately, in order to earn $5,000 monthly or $60,000 per year from $400,000, you would need to find an investment that earns a consistent high double digit return. $60,000 is 15% of $400,000. Given that it’s likely that the stock market will earn 7-9% average going forward, any return higher than that would be extremely speculative.

Before investing, it is important to educate yourself and get an understanding of how investing works as well as what is a reasonable rate of return. Then you can use a retirement calculator to help you figure out a way to meet your financial needs given your income, expenses and savings.

Here is a link to a credible list of top investing books: https://money.usnews.com/investing/investing-101/slideshows/best-investing-books-for-beginners?slide=15

My favorite retirement calculator is included within these free Personal Capital financial tools: https://barbarafriedbergpersonalfinance.com/go/personal-capital/ {affiliate link]

Also, the Nabers Group provides the opportunity for you to speak with an investment consultant here: https://www.solo401k.com/talk-to-an-expert/

You might get some recommendations of how to proceed. Just be wary of any recommendations to purchase high fee investment products and offers that promise returns of more than 9%.

Please let us know if we can help you in any other way.

Best of luck,

Barbara