The advantages of bonds include a steady cash flow and a reliable source of income. Government entities and corporations raise money to fund projects and recurring obligations. When you buy bonds, you become a lender to the issuer and earn interest in return.

Although the bond market hasn’t been attractive for quite some time, as interest rates rise, the bond benefits increase. Even so, like all long term investments, there is always some risk of bond price volatility.

However, bonds remain an important part of a well rounded investment portfolio, and a sound addition to your stock investments due to their high yields, fair prices and attractive capital gains potential.

This article provides all you need to know about bonds as a beginner or veteran in this investment niche.

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

What Are Bonds?

Bonds are fixed-income securities. When you buy a bond, you lend money to a government or company for a specific period and receive regular interest payments from the issuer. The term fixed originates from the ‘fixed’ interest payment or coupon that you get throughout the bond’s lifetime. Also, once the bond matures, the issuer returns your principal investment amount. You get back the loan in full at bond maturity date.

Bonds can add stability to a well-structured investment portfolio and offer you a reliable source of income. Bond prices are inversely correlated with market interest rates. So, when rates increase, the bond prices decrease and bond payments will rise. When interest rates drop, the bond prices increase, along with a commensurate drop in yield.

Governments issue bonds to supplement tax revenues, finance public projects, and to fund day-to-day obligations. On the other hand, companies issue bonds to fund new projects, ongoing operations and acquisitions.

There are taxable and non-taxable bonds. Tax-exempt bonds are issued by government entities and the interest received is not taxed by the federal government. If the bond is issued in your home state, you might also avoid state income taxes.

Bonds can be categorized by maturity. Short-term bonds mature in less than 5 years, medium-term, 5-10 years, while long-term bonds go up to 30 years.

Are Bonds a Good Investment?

Yes, bonds are a good investment. There are several advantages of owning bonds within an investment portfolio.

First, bonds can provide attractive capital gains – when interest rates decline. Bonds offer the agreed upon interest payments, and you will receive the par or full bond value upon maturity. If you choose to sell a bond before maturity, you might receive more or less than par value. When interest rates decline, you’ll continue to receive interest payments and capital gains, on the increased price of the bond, if you sell before maturity.

Second, the yields can improve significantly-when interest rates rise. As interest rates go up, new bonds are issued with higher interest payments. As a result, you have the opportunity for a good cash flow. In some cases, bond interest payments can exceed the inflation rate. For instance, corporate bonds typically offer higher yields than the rate of inflation. And inflation bonds, will offer interest payments in line with the inflation rate.

Third, bonds are less volatile, in general, than stocks. In contrast with stocks, bond values typically do not decline – or rise – as much as stock prices. In most cases, although not during 2022, bond values will hold up when stock prices drop, and vice versa. This leads to a more stable investment portfolio.

What Relationship Do Bond Prices And Bond Yields Have?

When a new bond is issued, it has a set price, usually $1,000, a set interest rate rate or coupon payment and a maturity date. The maturity and interest rate remain constant for the life of the bond and do not change. The price may vary.

Here’s the tricky point. When the market interest rate changes, then the price of the bond will either rise or fall.

There’s an inverse relationship between bond prices and yield. If bond prices drop, the yield will rise. If bond prices rise, the yield will decline – because you’re buying the bond at a premium.

If interest rates increase, then the value of a bond will decline, because investors aren’t willing to pay the same amount for a lower interest rate bond than the higher yield bond they can buy after a boost in interest rates. Although, the price of the bond will fall, any investor who buys a discounted bond will receive a higher yield.

For example, if you buy a 10 year bond for $5,000 with a 4.0% yield and annual coupon payment of $200, the yield is as calculated below:

Yield = (Bond interest/Bond Market Price) x 100

= (200/5000) x 100% = 4% yield

Suppose market interest rates decline and the bond price rises to $6,000. It now trades 20% higher than the issue price but at a lower yield to maturity, as the coupon payment of $200 remains.

Yield = (200/6,000) x 100% = 3.33%

The increased bond price has led to a decrease in the bond’s yield to maturity from 4% to 3.33%.

At this point, you could sell the bond and receive a capital gain of $1000 ($6,000 – $5000). If you did nothing, and held the bond until maturity, you would be getting your same 4.0% yield on the original $5,000 purchase price. When you bond matures, you’ll receive your principal payment of $5,000.

The same process works in reverse and illustrate the inverse relationship between bond price and bond yield.

When to Buy Bonds Vs. Stocks

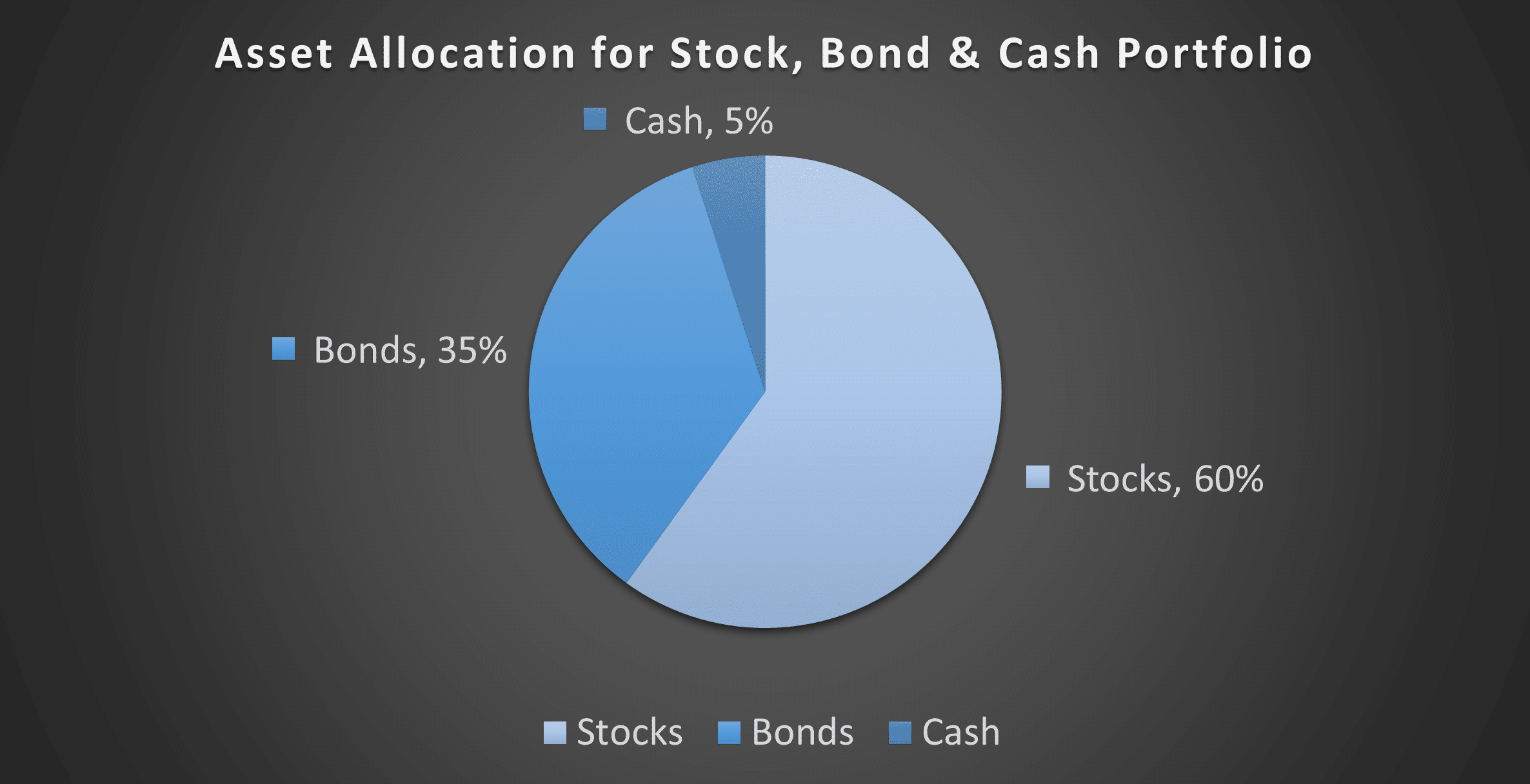

When investing, start by creating an asset allocation in line with your risk tolerance. Asset allocation is the percent of your total investment portfolio that’s invested in stocks, bonds, cash and other assets. Most financial professionals recommend conservative investors allot greater percentages to bonds and aggressive and younger investors invest more in stocks.

When to buy bonds? It’s best to buy bonds when interest rates are higher, so you can lock in higher yields. That said, there are reasons to buy bonds and stocks regularly, to grow your investment portfolio for the long term.

The main difference between bonds and stocks is the access to the issuing entity’s ownership. Stocks give you partial ownership of the issuing organization, while bonds don’t. Instead, bonds are a loan you lend to the issuer -government or company. You’re the bond issuer’s lender and recipient of interest payments on the loan.

Bonds are a more conservative investment than stocks. Bonds have a fixed interest rate that assures you specific returns, if held to maturity. Even if the bond value fluctuates, you’re promised a certain percent yield on your principal investment. Bond yields are typically higher than stock dividend payments.

Stocks are more volatile and riskier.

Consider is risk vs. reward. Bonds are safer than stocks but have lower expected total returns. Conversely, stocks are riskier due to their price volatility, but offer potentially higher long term returns. .

Historically, bonds have returned approximately 5% over time, while stocks have returned roughly 9%.

When you aren’t sure whether to invest in bonds or stocks, diversify your investment portfolio. Since the two react differently to market adverse events, having both stabilizes your portfolio. Set up a plan to regularly invest in the investment markets, through an auto invest feature or robo advisor. Keep your asset allocation of stocks vs bonds vs cash vs other steady.

What Should You Consider Before You Buy Bonds?

There are several things you should consider before you buy bonds, including the following:

- Bond risk

- Your risk tolerance

- Interest rate

- Maturity period

- Bond price

- Bond yield

- Redemption features

Bond Risks

Like any other investment, bonds carry some level of risk, including interest rate risk, credit risk, inflation risk, and liquidity risk. Hence, you need to assess the current degree of each risk before investing your money in these debt securities.

Luckily, various management tools like bond ratings are used to assess, analyze, and manage bond risks. Independent rating service providers assign a letter grade to the bond showing its credit quality: It evaluates the issuer’s financial strength (ability to pay the principal and interest at the right time).

A good grade indicates minimal chances of default and vice versa. Even so, it’s good to note that the higher the risk, the higher the returns, and low the risk, the lower the returns. The strongest quality bonds have a AAA credit quality. While the lowest quality bonds have C or D ratings and are typically called ‘junk bonds’ because of their poor credit quality and higher default risk.

Your Risk Tolerance

Understanding your risk tolerance is vital. You need to know how much risk you can handle: What to take and what to avoid. Hence you should consider factors such as:

- Potential cost of each risk

- Investment’s overall returns

- Negative effect of a failed investment

The assessment helps you to understand the risk-return tradeoff. That way, you know whether to invest in higher-quality bonds, investment-grade bonds, or both. Here’s a quick risk tolerance quiz. Or you can search online for more complex risk tolerance quizes.

If you were investing during 2022, when the S&P 500 dropped -19.44%, you know how well you handle risk. If you avoided selling at the market bottom, you are risk averse and can handle owning a portfolio with a greater allocation to stocks with less money in the bond market.

Interest Rate

Decide whether fixed, floating, or payable at maturity interest rate works for you. A fixed interest rate is determined when the bond is issued and interest is payed semiannually without changing.

Conversely, a floating interest rate is reset periodically depending on the current interest rate. Finally, with the payable at-maturity option the bond interest is paid when the bond matures.

Maturity Period

Bonds mature between 1-30 years: Short-term (below 5 years), medium-term (5-10 years), and long-term (more than 10 years) bonds.

Generally, short-term bonds are more stable and safer than the rest, as you’ll get back your principal after a short while with fewer chances of default. Thus, their returns are typically lower than long term bonds, although not always. On the other hand, long-term bonds are riskier due to price fluctuations and other market risks. Hence, their returns are usually higher.

Although, if investors believe that future interest rates will be lower in the future, than they are today, then long term bonds might not offer the premium of higher interest rates.

Bond Price

Factors such as interest rate, demand and supply, and tax status, among others, affect the bond price. Therefore, you should know if your potential bond investment sells above face value (at a premium) or below the face value (at a discount). New bonds sell close to 100% face value while existing ones’ prices keep fluctuating.

Bond Yield

Calculate the total profit you’ll gain after investing in the bond market. The return/yield to maturity you earn from a bond is based on the price you pay and the interest/coupon rate of the bond. When investing in a bond, it’s important to determine if there are other investments offering a comparable yield, with less risk.

If you’re investing for the short term, you might be better off investing in a high yield money market mutual fund, than a short term bond fund.

Redemption Features

Although the maturity date indicates how long the bondholder will loan the issuer, some bonds allow the issuer (call provision) or the holder (put provision) to change the date that the bond matures. Hence, knowing if such terms are present before you buy bonds is necessary.

How to Invest In Bonds for Beginners

Investing in bonds as a beginner requires you to understand the fundamentals of this type of investment. Below are some questions to consider:

How Do Bonds Work?

Bonds work by the investor lending money to the issuer (purchasing bonds) while the issuer sells the bonds to them, pays regular interest, and repays the principal upon the bond maturity.

For example, you can buy $20,000 worth of bonds for 10 years at an interest rate of 4%. In return, the issuer pays you $800 annually in 2 equal installments of $400 each. After 10 years, the issuer repays your $20,000.

How Do I Make Money from Bonds?

You have two ways to make money from bonds:

- Holding the bond until the maturity date and collect interest payments

- Sell them at a premium price (a higher price than the initial one).

There are typically two reasons behind a bond’s price increase: Issuer’s credit risk improves or interest rates decline and new bonds are issued with lower interest rates. Since the price and yields have an inverse relationship, an increase in the price leads to a decrease in yields. Hence, the profitable move might be to sell the bond for a capital gain.

What Are the Different Types of Bonds?

There 5 major types of bonds, including the following:

- Treasury

- Municipal

- Corporate

- Agency

- Savings

Each of the above types of bonds has its issuer, buyer, purpose, and risk vs. return levels.

- Treasury/government bonds: Issued by the federal government under the U.S. Treasury Department to fund government activities. Your income from treasury securities is federally taxable but free from local and state taxes. Treasuries are further subdivided according to maturity duration: Bills (up to 1 year), Notes (1-10 years), Bonds (more than 10 years), and TIPS- TIPS- Treasury Inflation-Protected Securities (5, 10, and 30 years).

- Municipal (muni) bonds: Local and state governments sell munis to fund public projects and their daily activities. Some of the bonds offer taxable income, while others are tax-exempt: Your bond yields are exempt from federal tax and, sometimes, local and state taxes. However, the tax-free ones are more popular, making munis an attractive investment if you’re looking for tax-free retirement income or you’re a high-net-worth investor.

- Corporate bonds: Debt securities issued by companies (private or public) to finance their daily obligations, ongoing projects, or acquisitions. Companies might prefer this fund-raising option as they can control the terms of the debt. Also, these debt securities are riskier than government bonds and, consequently, have higher rates of return.

- Agency bonds: Issued by Government Sponsored Enterprise (GSEs) like Fannie Mae and Freddie Mac. The raised funds finance the federal mortgage, agricultural, and education lending programs. Moreover, income generated from these bonds is federally taxed but may be exempt from local and state taxes.

- Savings bonds: The U.S. Treasury Department issues these debt securities to raise money for the government’s borrowing needs payment. The target buyers of savings bonds are individual investors. Thus, their prices are low enough for you to afford. Inflation bonds have become quite popular, due to their high current yields.

What Are the Pros and Cons of Bonds?

Pros:

- Offers greater diversification for better risk-adjustment returns and capital preservation.

- Preserves principal as you enjoy the regular fixed income from your investment.

- Provides fair yields that protect the bond value against inflation.

- Offers tax benefits as some bonds provide tax-exempt income.

- Have a lower default risk than other securities like stock.

- Provides more stable less-volatile income than equities

Cons:

- Risk of loss where the issuer has high credit risk: Unable to pay interest or repay the principal amount.

- Interest rate fluctuation, where a rising rate leads to a decline in the value of your bond portfolio.

- Potential loss if you need to sell the bond at a discount after and interest rate increase.

- Unexpected issuer downgrade leading to lower the bond prices.

You might benefit more from bonds by buying bond mutual funds or bond exchange traded funds (ETFs).

Individual Bond Funds Vs. Bond Funds

The main difference between individual bonds and bond funds is the maturity date and number of bonds that you own. Individual bonds have a specific time to recover your principal, while most bond funds are comprised of hundreds or thousands of bonds and have no maturity date.

An individual bond is ideal when you want to hold it until maturity without the risk of principal loss. Conversely, bond funds are the better option when you are seeking broad bond diversification within one fund.

To have a diversified bond portfolio, you need to own 10 or more individual bonds. For many, it is more convenient and affordable to own bond funds than individual bonds.

In short, individual bonds have less risk of principal loss because you can hold them to maturity and avoid the interest rate risk. Interest rate risk is the change in the bond’s value due to changes in the market interest rate. Although, if you buy lower quality individual bonds you might have a higher default and credit risk. A bond might default if the bond issuer experiences a bankruptcy.

On the other hand, bond funds have a higher interest rate risk. Should interest rates rise, the value of your bond fund might dip. But default and credit risk in a bond fund are negligible, due to the number of bonds owned within the fund.

Over time, the performance of owning individual bonds vs funds will be similar. When buying a bond fund, consider those funds with the lowest expense ratios, to ensure more of your dollars are going into the investment and not the fund managers pocket.

What Is the Outlook of Bonds in 2024?

The outlook of bonds for 2024 is optimistic. Their yields will likely remain relatively high in the year’s first six months. The high yields take bonds to their historical track record of being a reliable, low-risk income source for those who use the buy-to-hold-to-maturity strategy.

Should interest rates rise, bond fund owners might experience a small drop in fund prices, but new bonds that are added to the portfolio will have higher coupon payments, and increase the fund’s yield.

When market interest rates decline, bond owners will have an opportunity for capital gains.

Should You Buy Bonds Now?

Yes, you should buy bonds now. This is the most attractive bond market we’ve had since 2008. Many bonds outperform the expected inflation, meaning the prices are stable enough to withstand inflation.

Additionally, bonds have many benefits to qualify them for a place in your investment portfolio. These include a stable low-volatile source of income, investment portfolio diversification, principal preservation, tax benefits, and lower default risk.

However, these debt securities have some downsides that you should consider before you take the move. Bonds risk loss in case of an issuer’s low credit, lower prices when interest rates go up, or the issuer’s unexpected degradation, and potential capital losses should you need to sell, after a price drop.

When buying a bond fund, expense ratios matter. Consider bond index funds with expense ratios below 0.08% or eight basis points.

Investing is an art, not a science. Learn as much as possible, create a plan, and invest through thick and thin. Diversifying your investment portfolio minimizes the default and interest rate risks significantly.

FAQs

Yes, bonds are a good investment right now. Including bonds in your investment portfolio this year is a brilliant move: The venture is more attractive now than it has been for some time. Although future returns in any investment are rarely guaranteed.

Yes, you should buy bonds when interest rates are high. Investing at such a time can increase the overall returns of your bond portfolio. However, that only applies to long-term bond investors, as rising interest rates can negatively affect portfolio value in the short run.

Government bonds investors in the US include the Federal Reserve, foreign holders, individual investors and US financial institutions. Among the three, the US financial institutions segment is the largest buyer. The category includes state and local governments, pension funds, mutual funds, insurance companies, and commercial banks.

Mixing stock and bonds in your investment portfolio would be a good idea as it enhances diversification. Although bonds have lower long-term returns than stocks, they’re generally more stable. Hence, diversified portfolios minimize single-type investment-related risks.

Treasury bonds are a good investment. They’re considered low-risk investments and generally risk-free if you hold them to maturity. US government bonds have an negligible default risk. Treasury yields can be lower than those of corporate bonds, but enjoy freedom from state and local taxes.

When interest rates are rising, it’s best to invest in shorter term bonds and bond funds. That’s because shorter term bonds are less subject to interest rate risk. When interest rates rise, shorter term bonds will decline in value, less than longer term bonds. Also, bonds with shorter maturities can be replaced with higher yield bonds, when interest rates rise.

Mixing stocks and bonds in your investment portfolio is a good idea as it enhances diversification. Although bonds have lower long-term returns than stocks, their prices are generally more stable. Hence, diversified portfolios minimize single-type investment-related risks.

Treasury bonds are a good investment. They’re considered low-risk investments and generally risk-free if you hold them to maturity. US government bonds have an negligible default risk. Even so, treasury yields can be lower than those of corporate bonds, but do enjoy freedom from state and local taxes.

Related

- Groundfloor Review: Real Estate Crowdfunding with Good Returns

- Low Risk Investments For A Rising Interest Rate Environment

- Are I Bonds A Good Investment?

- Should I Invest In Bonds Even Though I Might Lose Money?

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.