Investment Tips for Beginners

If you want to learn the best tips for investing in stocks and funds, it’s key to learn a bit before you begin. Despite the glitzy Robinhood, Webull and investment app commercials, long term investing isn’t a game.

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

Tips for Investing In Stocks from Derek Sall, from Life and My Finances

During the pandemic, there are those that made a lot of money from investing in stocks. I wasn’t one of them.

But that didn’t put me off. I had my mind set on successful investing. I wanted to be good at it—so I kept educating myself and learning through experience. It felt good being a part of “the next big thing”. But I quickly realized that following the hype is foolish, something I’ll definitely touch upon in this article.

I felt really confident in the beginning, putting in 80% of my savings into investing. Eventually, I made double my yearly salary on the Covid Bull run, but I also lost half of those earnings (for reasons we’ll hit on in this article). That was pretty tough, and there’s a lot I’d have done differently and wish I’d known. You can’t simply fake it til you make it.

This article will cover actionable and insightful investing tips. If I had known them at the time, I would have saved a lot of money. Perhaps, they will help you start your investing journey.

Learn How to Realize Profits and Avoid Losses

Create a Sell Price When You Buy

One of the best tips for long term investing includes knowing when to sell a winner. Before you even buy a stock, it’s appropriate to consider what factors might cause you to sell it.

Most of the money that I lost was when I failed to recognize the ideal point in time to sell. The lesson learned is—don’t get too greedy! Don’t wait for the value to rise even more, because stock prices don’t go up forever. Be weary of stocks that balloon in value too quickly.

One of the best tips for long term investing is to consider selling some of your position if it becomes overly large—e.g., if it represents more than 5% of your investment portfolio. This can help to ensure that your investments are balanced and not overly concentrated in any one area, which can help to mitigate risk. Keep in mind that the 5% is a guideline and you should determine what level of risk you are comfortable with.

Also consider selling some of your position if the stock becomes excessively overvalued. We’ll talk more about stock valuation later.

Use Stop Loss Orders Cautiously

Some investors, in an attempt to avoid losses, create a “stop loss order.” This order becomes active when a stock reaches a specific price. In theory, a stop loss order helps to minimize losses if the stock experiences a sharp downturn.

But, there are risks to a stop loss order. A stop loss helps protect against significant losses—but also means you may sell the stock before it has a chance to recover. This is because selling at a target percentage may allow you to minimize losses, it also means you might miss out on future profits if the stock rebounds and continues to increase in price.

Evaluate the Stock Market News

Moreover, keep an eye out for warning signs such as negative news about an industry or company—or announcements of reduced or eliminated dividend payouts—may indicate financial struggles that could lead to a decline in the stock price.

Deciding whether to sell on bad news depends upon whether you believe that the news indicates a negative trend in the company’s growth or whether the firm will soon rebound.

It may be wise to sell a stock if it has experienced significant growth and reached your target price. This target price should represent a realistic future value for the stock based on your evaluation of its worth. Keep in mind that if a stock is overvalued in the market, it may eventually decrease in price.

Know Fair Value

“Buy Low Sell High”—easy to say, harder to execute. It’s crucial to get educated because our emotions can control our actions. Knowledge and experience will help you decide whether stocks or funds are overvalued or undervalued.

There are online calculators and websites that will provide an approximate “fair value” of a stock or fund. Through education and study, you can learn to assess fair value of a stock, typically through fundamental analysis.

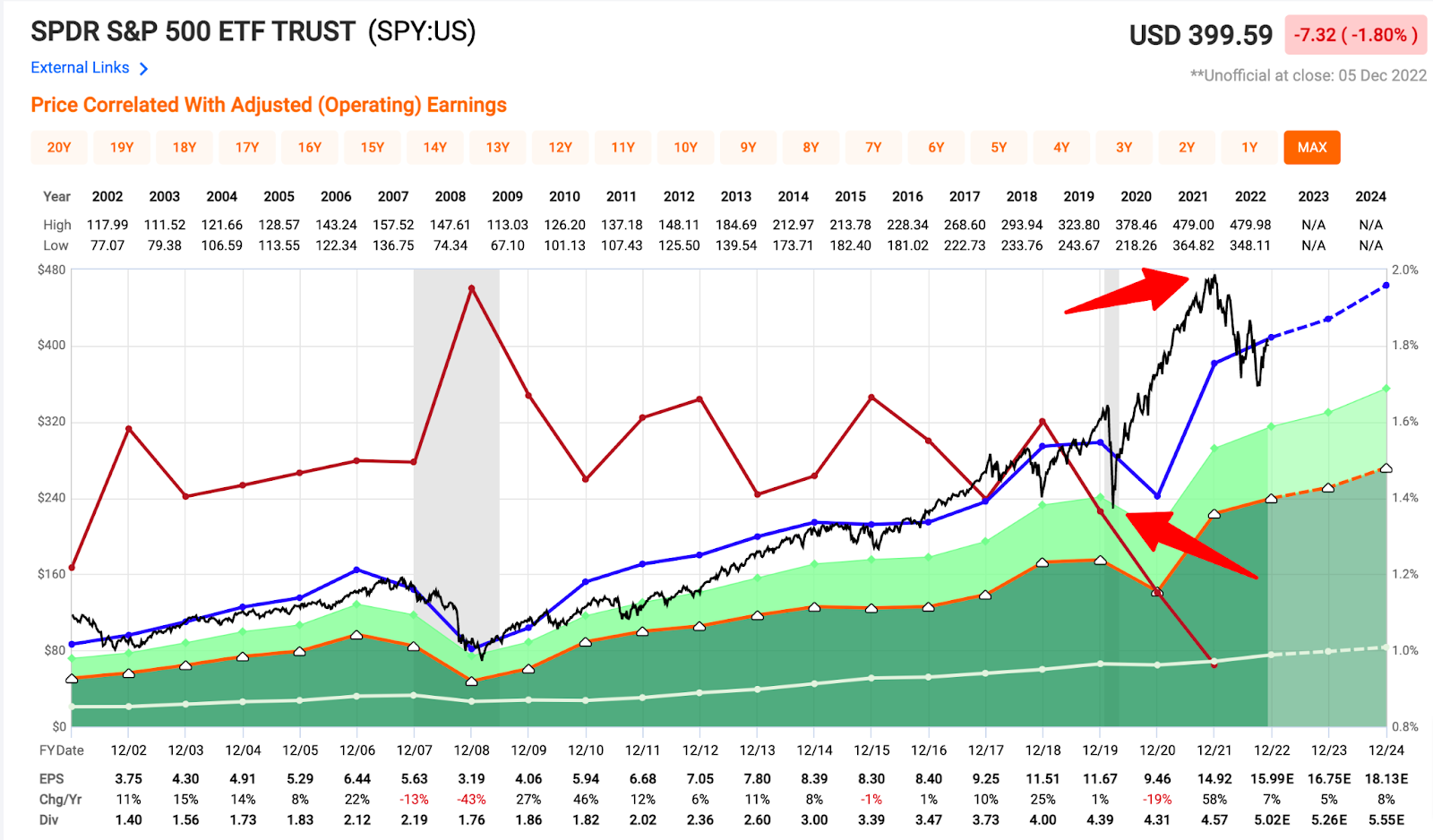

In general, a stock price will follow the company’s earnings. When earnings rise, the stock price should rise soon as well.

Earnings and Price Chart of S&P 500 ETF

Image credit: FastGraphs

Most of the time, the black price line follows the blue earnings line. Generally speaking, the blue earnings line is more stable than the more volatile price line. The earnings graph is smoother because companies will publish their earnings four times a year.

The price of a stock or fund represents not only earnings but the emotional responses of investors (specifically greed and fear). The price of a stock can sometimes deviate from its true value based on the emotional responses of investors. That said, It’s important to understand when stocks are overvalued or undervalued.

Over time, the price of a stock tends to follow the earnings of the company over time.

The stock price often outpaces the fundamental value of a company. When this happens, the stock may be considered undervalued. However, sometimes the price of the stock is lower than the fundamental value and the stock is considered overvalued. In the long term, the stock price tends to return to the mean and align with the company’s earnings.

But it may take months or even years for a stock price to return to “fair value.”

The investing tip of “knowing fair value” might be useful over the long term, but in the short term -not so much. Stocks and stay over or undervalued for a very long time. So selling an overvalued stock or fund can result in years of missed performance, as the asset remains overvalued. While buying an undervalued asset doesn’t mean that it will return to fair value soon.

Minimize Investment Costs

This investing tip is within your control and a proven way to improve investment returns.

if you planning to invest in ETFs and mutual funds then you need to examine fund expense ratios. The investment firm charges a certain percent of the fund’s assets as a “management fee” or “expense ratio.”

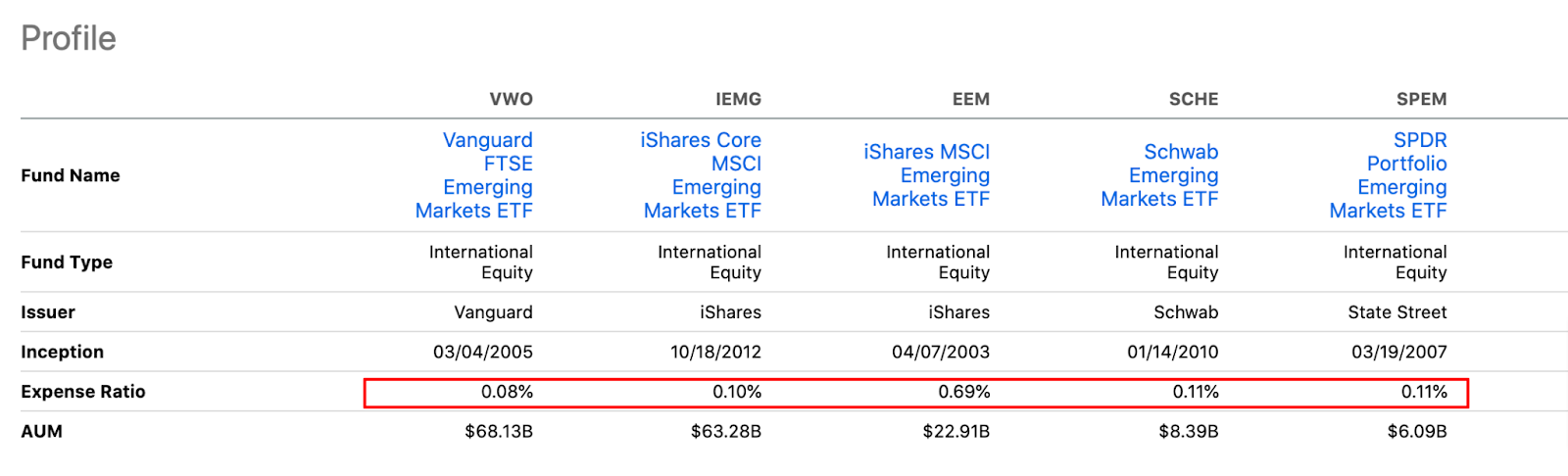

For example, EEM and EMG are similar ETFs from emerging markets, yet their cost differences are significant (0.69% and 0.10% of AUM respectively).

Some ETFs—like popular Vanguard’s VWO—cost even less at 0.08%. You might be paying up to eight times more for an ETF tracking the same index.

Take a look at the management fees of 5 emerging markets exchange traded funds:

Image credit: seekingalpha.com

The Personal Capital free investment tools and calculators can show you how fees can hurt long term investment performance.

Even more interestingly—if we compare the performance of these five emerging market fund, Vanguard’s ETF (the one with the lowest expense ratio) had the best return over the last 10 years:

Image credit: Koyfin.

To put this difference into perspective let’s see how fund expense fees influence your investments over 30 years. Notice how investing in a low fee, passively managed index fund with a 0.04% expense ratio instead of a higher 0.29% fee could save you roughly $7,000 over 30 years. A high fee fund has to outperform the lower fee investment by quite a large margin in order to justify paying the higher management fee.

Difference in Returns of Low vs. High Fee ETFs

| Fund Expense Ratio | 0.04% | 0.29% |

| Initial Investment | $10,000 | $10,000 |

| Time Invested | 30 years | 30 years |

| Average Annual Rate of Return | 8.0% | 8.0% |

| Ending value (net of fees) | $99,514 | $92,828 |

| Cost of fees | $1,112 | $7,798 |

Source: https://www.nerdwallet.com/article/investing/mutual-fund-calculator

There are reams of studies that show low fees correlate with higher returns and better fund performance.

Diversify

You might be thinking—what exactly is diversification in this context? Well, diversification is a strategy used in investing to spread out your capital across different types of investments and industries. By doing so, you can potentially increase your returns and reduce your overall risk. It may be worth looking into whether you want to manage your own portfolio, or have a professional’s help.

So, why exactly is diversifying your portfolio useful?

Portfolio diversification involves selecting investments that don’t move in the same direction in all market conditions. By investing in assets that are not closely related, you can decrease the overall risk of your portfolio—even if the individual investments themselves are risky. By risk, we mean the volatility, or ups and downs in your investment portfolios value.

For example, a portfolio manager might invest in a package delivery company (Investment A) and a video conferencing platform company (Investment B). If there were a gas shortage that negatively impacted the package delivery company, the stock price of Investment A might drop. However, Investment B’s stock price could potentially go up, as the demand for videoconferencing may rise because more people would work from home. This is how risk is mitigated by “spreading out” your capital across different investments.

Here are three ways to diversify your portfolio:

- Individual Asset Diversification: This involves investing in a variety of assets within a single asset class, such as stocks. This can be achieved by buying a market index fund that includes a range of high- and low-risk stocks across different industries. Alternatively, you can choose to invest in industries that are complementary to one another.

- International Market Diversification: This involves looking beyond your own country and investing in international markets. This can help to mitigate risk in the event that your own country’s market performs poorly. Keep in mind that investing in other countries may have different rules and regulations.

- Asset Class Diversification: This involves investing in a range of asset classes—such as stocks, bonds, cash, and alternative investments. Alternative investments have fewer regulations, and are a great way to provide additional levels of diversification—such as gold, REITs, real estate, etc.

In general, the simplest way to diversify your portfolio is by choosing several low-fee ETFs from various asset classes.

Reverse Test Your Portfolio

You can reverse test your portfolio once you decide what kind of instruments you want to invest in. Reverse testing—or backtesting—is a way to test the performance of a trading strategy or model using historical data. It allows traders and analysts to evaluate how well a strategy would have worked in the past—and can give them confidence in using it in the future.

The process involves simulating the application of a strategy or model to past data—and analyzing the results to see if it would have been successful. This can help you identify any potential weaknesses or problems with the strategy—and make any necessary adjustments before implementing it in live trading.

The data set used for backtesting should include a wide range of stocks—including those from companies that may have gone bankrupt or been sold or liquidated. Failing to include such stocks can lead to artificially high returns in backtesting.

It’s also important to consider all trading costs—even small ones—as these can accumulate over the backtesting period, and significantly affect the appearance of a strategy’s profitability.

The basic idea behind backtesting is that the performance of a strategy in the past can be used to predict its future performance. This is based on the assumption that financial markets follow certain patterns and trends—and that these patterns and trends are likely to repeat themselves over time.

The following tool helps you test what would have historically happened if you invested in XYZ. It’ll bring a new perspective onto whether you’re choosing the right or wrong instrument for you https://www.portfoliovisualizer.com/backtest-portfolio. Just remember, using historical data to backtest your portfolio isn’t perfect. There’s no guarantee that prior investment performance patterns will repeat in the future.

Avoid the Hype

The hard truth is, most people lose money on IPOs. Sure, you can buy them, get lucky and make some money temporarily—but most people trade them. With IPOs, it’s crucial to understand the best time to sell.

According to CNBC, IPOs are not worth it—don’t invest into them. They can be okay if they sell early, but generally speaking—as a rule of thumb—don’t get into them.

A similar logic applies to thematic ETFs. Over a longer period of time, it’s really difficult to beat passive ETFs—and there aren’t many thematic ETFs that actually stood the test of time. Morningstar said, “During the 15 years through Dec. 31, 2021, more than 80% of thematic funds worldwide closed their doors”. More often than not, thematic ETFs are based on hype and enthusiasm or current hype, like “artificial intelligence.”

At the end of the day, the best companies will be included in passive index fund ETFs—which is why they survive long periods of time. Historical information shows that it is very difficult for active investing, like trading individual stocks and funds, to outperform the returns of investing in market matching index funds.

Here are some examples of companies that were hyped up in the past, and where they are now. Don’t fall for the bait.

Image source: Compounding Quality

Following the crowd typically leads to subpar investment results.

The Bottom Line

It really comes down to how determined you are in learning how to invest. If you’re still wondering about the best long term investing tips – education will go a long way to help you learn about investing basics. You can do this by reviewing educational articles on your investment firm’s website. Or join AAII – American Association of Individual Investors. Or take one of the top notch investment courses on Investopedia or Morningstar. Another top investing tip is to realize that investing is not a get rich quick scheme, but a long term path to turn a portion of your current earnings into long term wealth for the future.

Bio: Derek Sall is the founder of LifeAndMyFinances.com where he helps his readers get out of debt, save money, and build wealth

Related

- What Is An ETF and How To Invest In ETFs

- Why You Should Invest In Index Funds

- Why Is Asset Allocation Important?

- How To Choose Mutual Funds? Reader Question

- American Association of Individual Investors Review – by a Lifetime Memeber

- Ziggma vs Empower Investment Tracking App Review

- A Penny Doubled Every Day For 30 Days Or $1 Million – Which Would You Choose?

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.