Roth or 401k which should I max out first? asked Buck Inspire

This is an excellent question: which to max out first, a 401k or Roth IRA?

The easy answer, max out both the 401K and the Roth IRA! You can’t go wrong saving and investing as much as you possibly can now.

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

What if I Can’t Max out Both My Roth IRA and 401K?

In the real world we all need to make financial choices. Most investors can’t afford to max out their 401k and their IRA. So, how to allocate retirement funds is a common question.

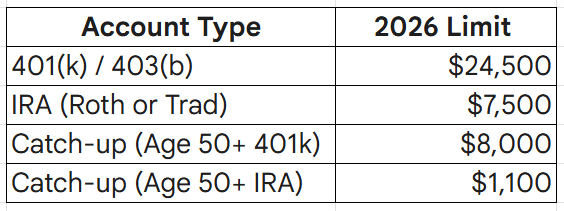

If you can afford to max out both, here are the contribution limits for 2026:

Higher income earners may not be able to participate in both a 401k and a Roth IRA.

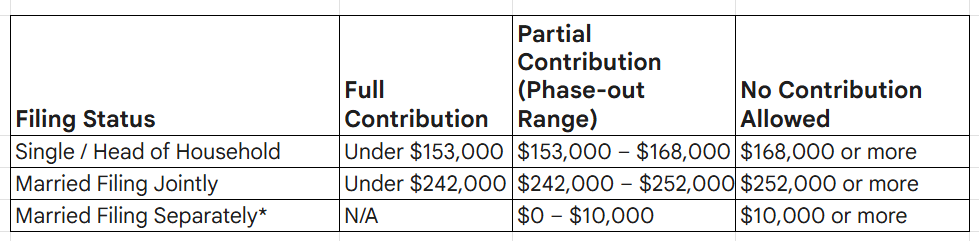

Following are the 2026 Roth IRA contribution and phase-out ranges, based upon taxable income:

Find more money to invest; 7 Unique Ways to Save Money

Which to Max out First – 401k or Roth IRA?

First, if your company matches your 401k investment, make sure to contribute enough to get the employer match.

After you receive the free employer money, then the decision whether to go with the Roth or 401k depends on several factors.

The Pros and Cons of a 401k vs. a Roth IRA Retirement Account

401k Pros

An advantage of the 401k over a Roth IRA is that your contributions are tax deferred which means your taxable income is reduced by every dollar that’s paid into the 401k. So, if you make $70,000 and contribute $10,000 to your 401k then you’re only taxed on $60,000 of income (for Federal taxes- state policies vary).

Assuming solid, low fee investment choices and the ability to defer taxes, it makes sense to max out your 401k contribution.

401k Cons

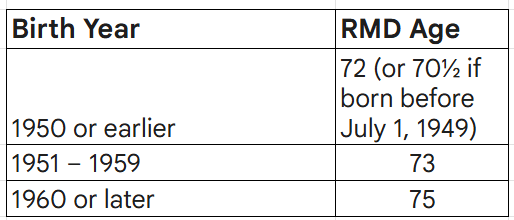

There are several disadvantages to investing in a 401k. You might not like the investment choices offered by your employer. Another disadvantage of investing in a 401k over a Roth is that you must start withdrawing your 401k funds between ages 72 and 75, depending upon your birth year. And you have limited investment options in your 401k. There are a much wider range of investment choices in a self-directed Roth IRA.

Required Minimum Distributions Ages

Read this article if you are experiencing retirement anxiety?

Ultimately, if you don’t like the available choices in your 401k, then invest only up to the employer match and invest the maximum in a Roth IRA for the rest of your retirement investing.

If you like the choices and appreciate the opportunity to reduce your current tax bill, then invest as much as possible in the 401k.

Bonus; Fidelity Retirement Savings Guidelines

Roth IRA Pros

The advantages of investing in a Roth IRA, or Roth 401k, are that you are not required to withdraw the money during your lifetime and the invested funds continue to grow and can even be passed on to your heirs. While most non-spouse heirs must now withdraw all inherited IRA funds within 10 years, certain ‘eligible’ beneficiaries—like spouses or those with disabilities—may still have more flexible options.

Among the greatest benefit of investing in a Roth IRA versus a 401k is that in most cases, withdrawals are tax free. In order for the Roth IRA funds to be withdrawn tax-free, they must meet these conditions:

- The 5-Year Rule: The account must have been open for at least five years (starting from Jan 1st of the year of your first contribution).

- The Event Rule: The withdrawal must occur after you reach age 59½, or due to death, disability, or a first-time home purchase (up to a $10,000 lifetime limit).

Roth IRA Cons

A disadvantage of investing in a Roth IRA is that you must pay income tax on the money before investing in your Roth IRA.

Another disadvantage of Roth IRA investing is that high income investors might not be able to participate. Check the chart above for specific limits. In that case, a Traditional IRA might be another option.

If you’re eligible, a Roth IRA is an outstanding wealth preservation and wealth transfer account.

401k or Roth IRA – Predicting the Future

Another factor in your investment choice is your future tax bracket.

I don’t know about you, but I’m not a fortune teller. Although, I expect that tax rates will be higher in the future, since they at historically low levels now.

But, I’m not sure if my personal tax rate will be higher or lower at retirement. In retirement, my salary income will be eliminated and I’ll be living on pension income , Social Security and our invested assets. So, I assume my retirement income will be lower than our family income is now. But, tax rates could rise. And I will need to withdraw funds (RMD) from my 401k account.

So, it’s possible that tax rates will be higher in the future, and income levels might be lower.

If you really need a tax break now because your income and tax brackets are high, and you think that they will be lower in the future, then the 401k may be the one to max out first. That is, as long as you are happy with the investment choices available in the 401k.

Read now; 5 Ways to Make Sure You Conquer Your Financial Goals

Finally, in the future, you’ll pay tax on the 401k withdrawals which must begin between ages 72 and 75. And, you never need to withdraw your Roth IRA savings, if you don’t want to.

Bonus Roth IRA Investing Idea

One benefit of a Roth IRA, is that you might encourage your kid to start a Roth IRA, with her summer earnings. A kid Roth IRA could actually make her a millionaire, by starting to invest early!

Ultimately, there’s no way to determine the perfect answer to this question now. The best answer is make sure to save and invest as much as you possibly can now. Look at the pros and cons of each option, then make your best decision.

Related

- The Truth About The 401k – Myths Exposed

- How Can I Tell If I’m On Track For Retirement?

- How To Save For Retirement At 30 And Become A Millionaire?

- How To Start Investing For Women

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.

1 thought on “Roth or 401k, Which to Max Out First?”

Hey,

I must commend you on your comprehensive approach to the topic. Your article not only provides valuable information but also instills confidence in those considering a freelance career. It’s evident that you’ve invested significant time and effort into researching and compiling this piece, and it truly shows.

Comments are closed.