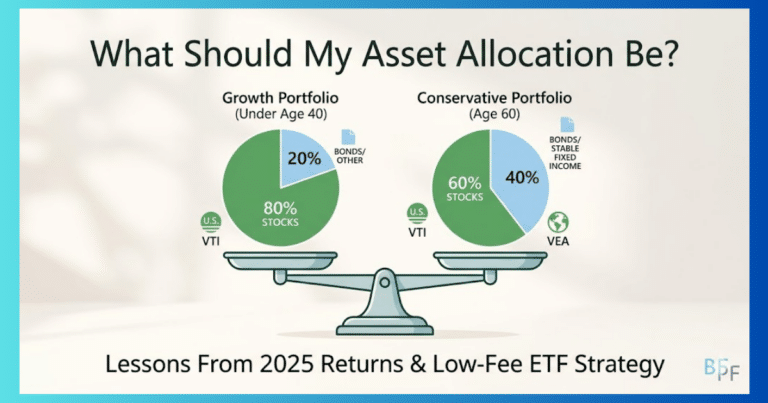

What Should My Asset Allocation Be? Lessons From 2025 Returns

Wondering, “What should my asset allocation be?” The 2025 market performance data can inform sensible asset allocation ETF portfolios. Key

Wondering, “What should my asset allocation be?” The 2025 market performance data can inform sensible asset allocation ETF portfolios. Key

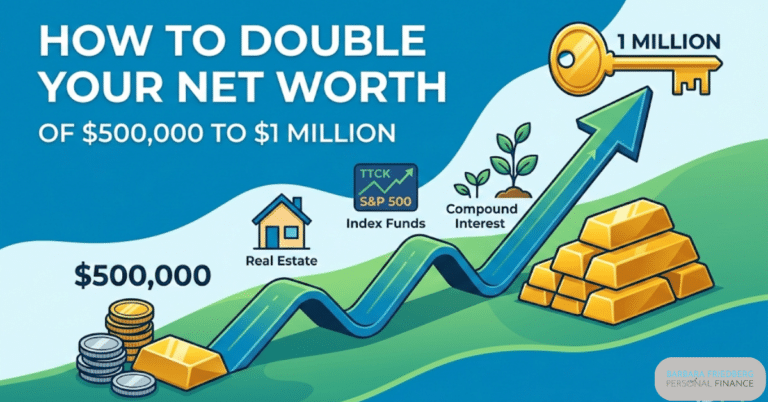

A reader wrote in asking how to double his net worth, from $500,000 to $1,000,000. Doubling a net worth of

Start Building Wealth Now With the Best investment Advice for Millennial Women By contributing columnist, Alexandra Deluise Millennial women, we have a lot going on right now. We’re fighting for equal pay while simultaneously facing difficult employment prospects, crippling student loan debt, and inflation that makes it tricky to afford having a family and homeownership simultaneously. None of that is a reason to let our investments fall by the wayside, however. If anything, millennial women …

When and how much to allocate to speculative investments? If passive investing is the right strategy, is there room for any active investing?

Invest Like a Woman and Become a Millionaire by Investing With my experience as a multi-decade investor, former professional portfolio manager and university investments instructor, I will reveal easy to implement strategies to build wealth for women (and men too). Research by Prudential found that women worry more about risk than men. I get it, despite investing for decades, I’m scared of risk too. Women report that they lack confidence in finances too. Even though in multiple studies, women…

Historical Stock and Bond Returns-Predict Future Returns I’m a bit obsessed with historical stock and bond returns. Since I’m a control freak, and the future is unknowable, knowing historical stock and bond returns gives me an illusion of control. And I’m not alone in my interest in historical stock and bond returns. If you’re wondering why you should care and how understanding historical stock and bond returns might help you, read on. Financial educators frequently use the historical return …

The best lazy portfolio is the one set up in line with your risk tolerance and rebalance regularly. In investing there’s no one right way to invest or manage your portfolio. In fact there are hundreds of different approaches, and probably more. Consider the active portfolio managers, they all have their own ideas about how to get the highest returns for their particular strategies. Then there are the hedge funds, clamoring for alpha from creative investment strategies. Finally, the market tim…

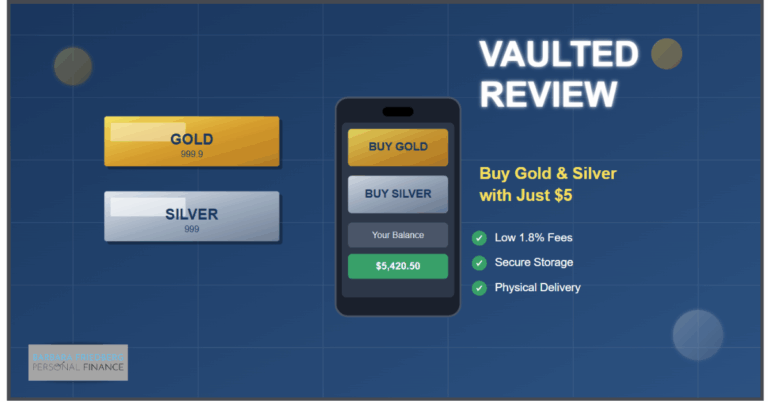

Find out whether investing in gold is for you. You’ll learn the pros and cons of investing in physical gold, how to invest in gold with an app, and get all of your gold questions answered.

This Vaulted Gold App Review explains the pros, cons and features of the unique silver and gold investment app. You can start with $5 and invest in pure gold bars. Store your gold and silver or have it sent to you.

Investing can feel overwhelming—especially when headlines scream about market crashes, recessions and global uncertainty. But here’s the truth: the best long-term investing strategy isn’t about timing the market or chasing trends. It’s about building a resilient, goal-driven plan that grows your wealth steadily over time. Whether you’re just starting out or refining your approach, this guide will walk you through the essentials of a long-term investing strategy that works—anchored by proven p…