Best Long-term Investing Strategy: Build Wealth With Confidence

A former MBA student wrote in asking, “What is the best long-term investing strategy? I’m so confused about investing, that I don’t know where to begin.”

Investing can feel overwhelming—especially when headlines scream about market crashes, recessions and global uncertainty. But here’s the truth: the best long-term investing strategy isn’t about timing the market or chasing trends. It’s about building a resilient, goal-driven plan that grows your wealth steadily over time.

Whether you’re just starting out or refining your approach, this guide will walk you through the essentials of a long-term investing strategy that works—anchored by proven principles and practical tools.

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

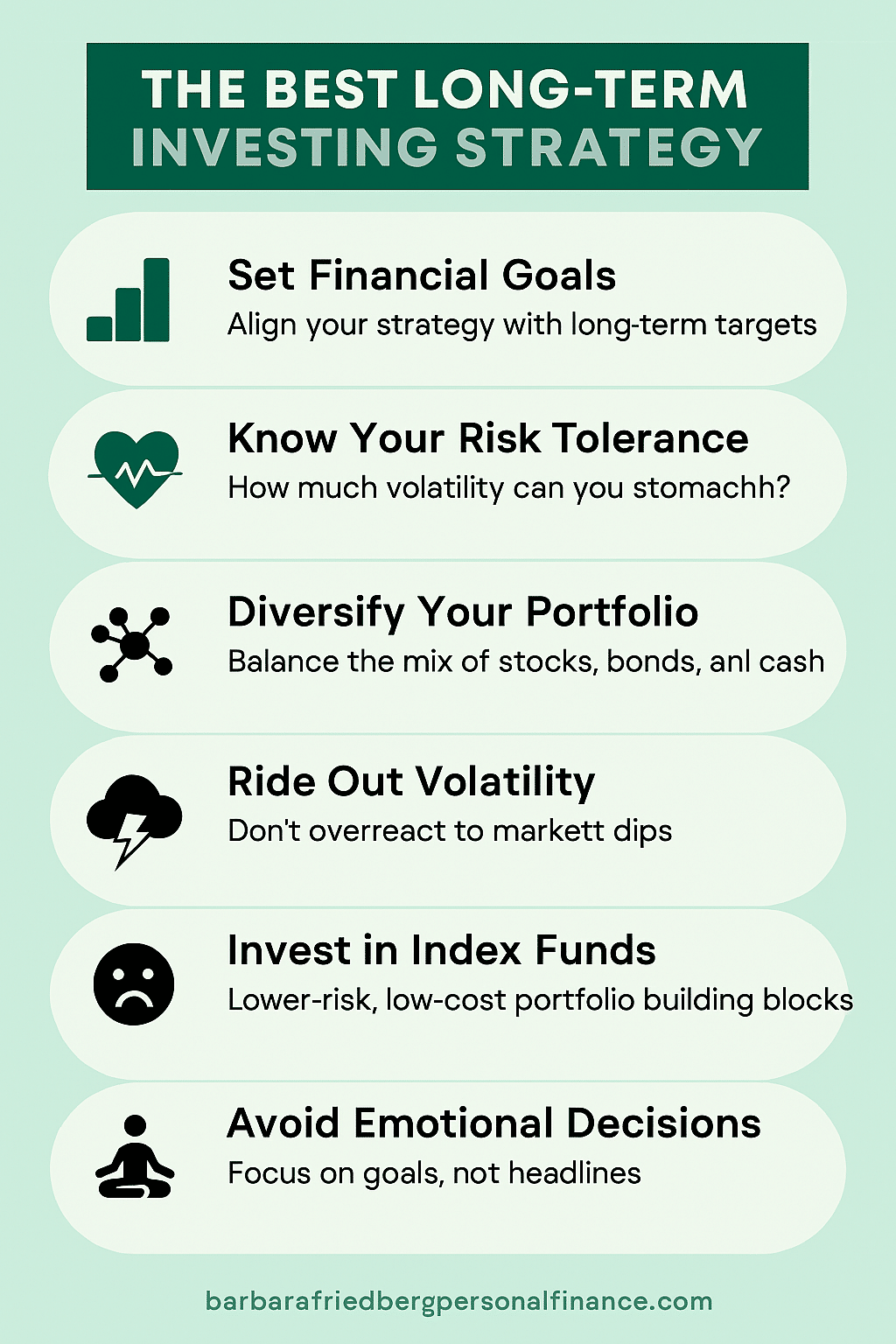

Start with Financial Planning Goals

Before diving into stocks or bonds, take a step back and define your financial planning goals. Are you saving for retirement, a home, or your child’s education? Your timeline and investment risk tolerance will shape your strategy.

- Short-term goals (1–3 years) may require safer assets like cash or short-term bonds.

- Long-term goals (5+ years) benefit from growth-oriented investments like stocks and ETFs.

Having clear goals helps you avoid emotional investment decisions and stay focused when markets get rocky.

Understand Investment Risk Tolerance

One of the most overlooked aspects of investing is knowing your investment risk tolerance. This refers to how much market fluctuation you can emotionally and financially handle.

Ask yourself:

- How did I feel during the last market downturn?

- Would I panic if my portfolio dropped 20%?

- Am I comfortable with short-term losses for long-term gains?

Your answers will guide your portfolio asset allocation—the mix of stocks, bonds, and other assets you hold. A balanced portfolio aligned with your risk tolerance helps you stay invested through ups and downs.

Many experts minimize investment risk tolerance and use age as a major factor when crafting a long-term investing strategy.

While younger investors have a longer time to recover from losses which occur during a market drop, that doesn’t mean you should own 80% to 90% stocks in your investment portfolio.

Understand that stock-heavy portfolios decline more when prices drop and rise more during bull markets. Risk tolerant investors, regardless of age, can own greater percentages of stocks, while conservative investors, should consider more balanced portfolios.

If you’re risk averse with a stock-heavy portfolio, you might be tempted to sell after a decline which can hurt your ultimate investment returns.

Build a Diversified Portfolio Asset Allocation

Diversification is your best defense against stock market volatility. By spreading your investments across different asset classes, sectors, and geographies, you reduce the impact of any single downturn.

Here’s a simple breakdown:

- Stocks: Offer high growth potential but come with volatility.

- Bonds: Provide stability and income, ideal for conservative investors.

- Cash: Safe but low-yield; useful for short-term needs.

A well-diversified portfolio asset allocation might include:

- 60% U.S. and international stocks

- 30% bonds or bond funds

- 10% cash or short-term instruments

Rebalance annually to maintain your target allocation and adjust as your goals evolve.

Don’t Fear Stock Market Volatility

Market dips are inevitable—but they’re not a reason to abandon your plan. In fact, downturns often present buying opportunities for long-term investors.

Historical data shows that despite recessions, elections, and global crises, markets trend upward over time. That’s why a long-term investing strategy is so powerful: it allows you to ride out the noise and benefit from historical market returns.

Remember:

- Time in the market beats timing the market.

- Reacting emotionally can sabotage your returns.

- Stay the course, even when headlines are scary.

Choose the Right Tools

You don’t need to be a stock-picking genius to succeed. Consider these tools to simplify your journey:

- Index funds and ETFs: Low-cost, diversified, and ideal for passive investors.

- Robo-advisors: Automated platforms that build and manage portfolios based on your goals and risk tolerance.

- Target-date funds: Adjust asset allocation automatically as you approach retirement.

These options align well with a recession investment strategy—helping you stay invested without constant monitoring.

Helpful Investment Tools:

- M1 Finance has expert portfolios in a variety of strategies and risk tolerance levels.

- Wealthfront is a low-cost robo-advisor with a wealth of investment portfolios and customization options.

- You can craft your own portfolio at both M1 Finance and Wealthfront and invest in low-fee index funds and ETFs.

Avoid Emotional Investment Decisions

Investing isn’t just numbers—it’s psychology. Fear and greed can lead to impulsive moves that hurt your long-term results.

To stay grounded:

- Set rules for when and how you’ll adjust your portfolio.

- Limit how often you check your account.

- Focus on your financial planning goals, not market noise.

If you’re feeling anxious, revisit your investment risk tolerance and remind yourself why you started.

Monitor Historical Market Returns

Looking at historical market returns can provide perspective. For example:

- The S&P 500 has averaged ~10% annual returns over the past century.

- Even after major crashes, markets have recovered and grown.

Use this data to reinforce your confidence in a long-term investing strategy. It’s not about avoiding losses—it’s about compounding gains over decades.

Stay Calm During Market Downturns

When the market drops, your instinct may be to sell. But that’s often the worst move. Instead, follow a market downturn response plan:

- Review your goals and timeline.

- Rebalance if needed, but avoid panic selling.

- Consider dollar-cost averaging to invest steadily over time.

This approach helps you capitalize on lower prices and maintain discipline.

Final Thoughts: Invest with Purpose

The best long-term investing strategy isn’t flashy—it’s consistent, goal-driven, and emotionally intelligent. By focusing on portfolio asset allocation, understanding your investment risk tolerance, and resisting emotional investment decisions, you set yourself up for lasting success.

So take a breath, revisit your financial planning goals, and commit to a strategy that builds wealth with confidence. The future is yours to shape—one smart investment at a time.

Related

- What Are The Differences Between Short-, Medium- and Long-Term Goals?

- 8 Steps To Creating A Diversified Index Fund Investment Portfolio

- Robo-advisor vs. Target Date Fund

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.