Invest Like a Woman and Become a Millionaire by Investing

Investing Tips for Women

With my experience as a multi-decade investor, former professional portfolio manager and university investments instructor, I will answer the question, “Where should I invest money to get good returns?“ You’ll learn about how investing for women is straightforward and accessible.

You’ll learn easy to implement strategies to build wealth for women (and men too).

Research by Prudential found that women worry more about risk than men. I get it, despite investing for decades, I’m scared of risk too.

Women report that they lack confidence in finances too. Even though in multiple studies, women are more successful investors than men.

Women, investing is so simple, once you learn the basics, you’ll wonder why you haven’t started earlier, or invested more.

So, put aside your fear, learn a few investing basics, and get started building your financial future.

Women, it’s easy to find the best investments to make money – for the long term.

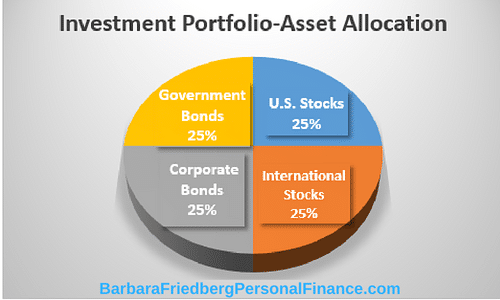

Traditional wisdom recommends looking at your total investable assets like a pie. Put the largest piece of pie – up to 80% in stock investments, depending upon your age an risk tolerance, and watch your portfolio grow.

Women and Investing Fidelity Survey Results – The Women Win!

A Fidelity Investments, 2021 Women and Investing study, compared 1,200 women investors with 1,200 men. Currently, 67% of women with a retirement account also invest outside of their retirement plan. This is up from 44% in 2018.

In a study of 5 million Fidelity customers over the last 10 years, women outperformed the men by 0.4%.

Investing 101 for Women – Investment Strategies for Beginners

Long term, investing in the financial markets is a brilliant way to build wealth. Although female investors may lack confidence in managing an investment portfolio, women’s past performance typically surpasses that of their male counterparts.

Women investors, striving for financial security will benefit from creating a financial plan and understanding investment history.

Long Term Investment Returns

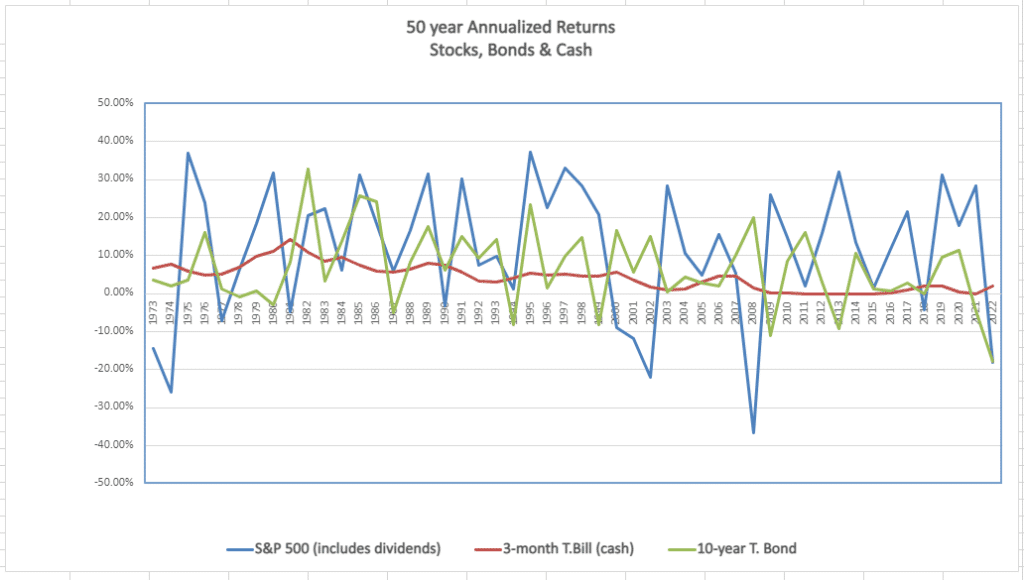

Data source; http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html

From 1973 through 2022, the S&P 500 broad stock market index returned more than 10.00% annually.. Yet, don’t let this long turn return fool you. Embedded in the glorious long-term stock market returns are some horrible losing years. While during this same period, bonds delivered north of 6.00% annualized and cash roughly 2.00%.

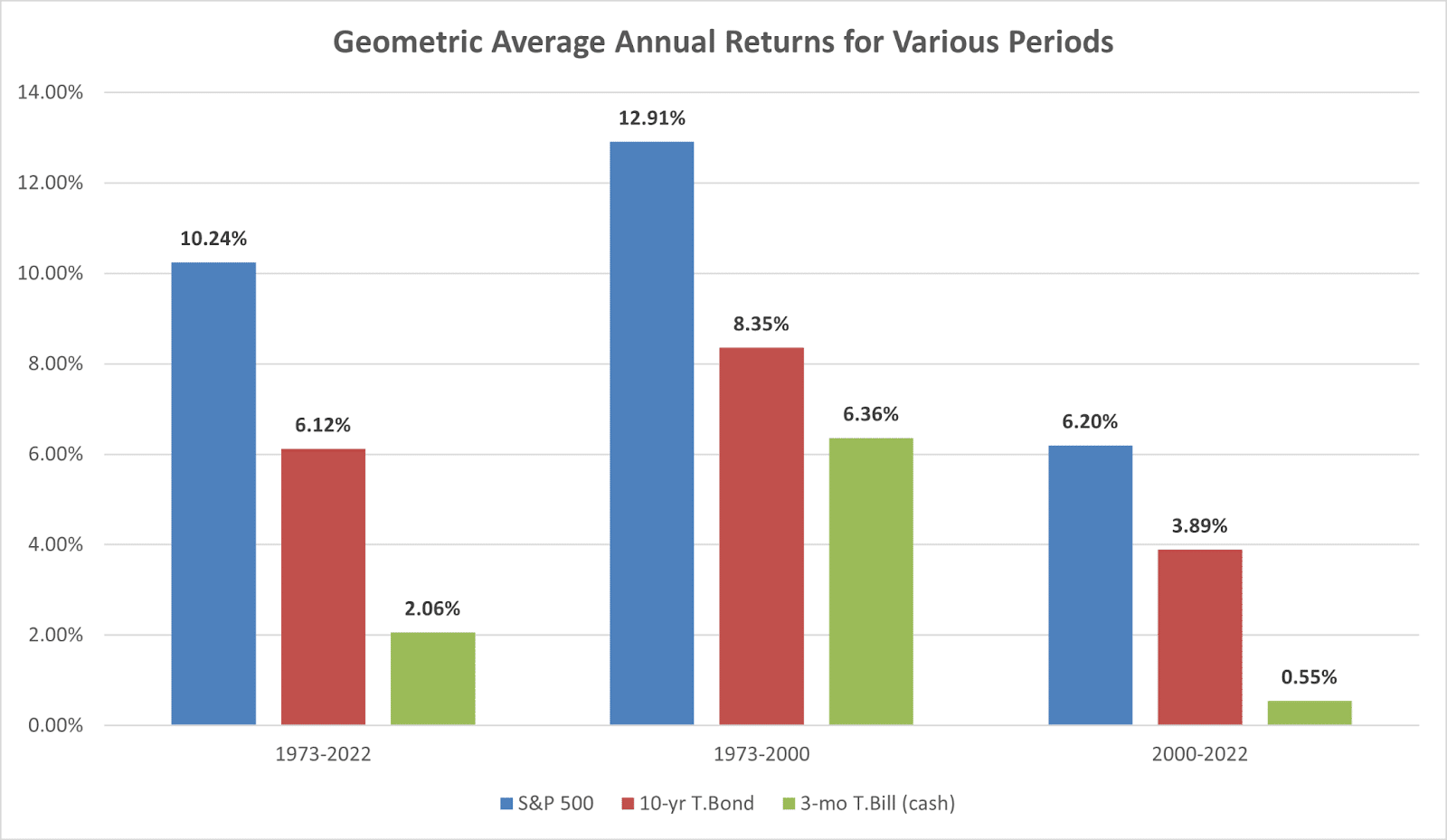

Data source; http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html

From 2000 to 2022, the stock market returned 6.20%, in contrast with the historical long-term average of 9 to 10%. Clearly, to meet your financial goals, women must understand that the stock market has delivered the highest long-term returns, albeit with the greatest amount of volatility.

In reality, most investors do not achieve an average annualized return over time on their long term stock investments, because many investors trade in and out of the markets.

The typical investor, due to fear, greed, or a belief that she can outperform the market will buy and sell various individual stocks and managed mutual funds. When stocks are on a normal cyclical downturn, investors get scared, and sell. Conversely, during cyclical stock return upswings, investors, afraid of missing the boat buy as the markets hit a peak. This type of behavior leads to buying high and selling low.

According to Barber, UC Davis and Odean, UC Berkley in the “Behavior of Individual Investors”, individual investors:

- Underperform standard benchmarks (e.g., a low cost index fund).

- Sell winning investments while holding losing investments (the “disposition effect”).

- Are heavily influenced by limited attention and past return performance in their purchase decisions.

- Engage in naïve reinforcement learning by repeating past behaviors that coincided with pleasure while avoiding past behaviors that generated pain.

- Tend to hold undiversified stock portfolios.

These behaviors damage your long term net worth.

So, although over long periods of time stock market investments averaged over 9% annually, most investors do not achieve those same returns.

But, these self defeating investing tactics can be turned around into the best investing strategies for the long term.

Investing Tips for Women – How to Combat Investment Underperformance

The research is abundantly clear that it is extremely difficult to beat the returns of the overall market. Even exceptional mutual fund managers who outperform the major stock market indexes before expenses, fail to surpass their benchmark indexes when expenses are factored in.

Sure there are exceptions, Warren Buffett, Peter Lynch, and George Soros are extraordinary investors. Chances are, you’re not one of them. Plus, there are excellent women investors as well!

In reality, the majority of highly compensated managed mutual fund managers fail to outperform their market benchmarks.

So, if most investors fail to outperform the simple stock market indexes, what should women investors do?

Here’s, what you should invest in.

The Best Personal Investment Strategy for Women (and Men too)

Women, here’s how to win at investing with long term investment strategies:

1. Invest for the long term. If you cannot leave your money in a stock index fund, for at least 8-10 years, do not invest. Markets are volatile and over the short term, your returns are random. Over the long term if you believe U.S. and global companies will grow and prosper, then their underlying stocks will advance as well.

2. Cut investment expenses to the bone. Realize that investment expenses are taken off the top. If you invest in a managed mutual fund charging 1% per year, then out of every $1,000 you invest, only $990 is going towards building wealth. And that’s not just in year one, that’s every year, that 1% is taken out. Thus, if the fund loses 3% one year, you lose 4%.

Go with the lowest expense mutual fund or Exchange Traded Fund (ETF) you can find. For example, VTI, Vanguard Total Market Index ETF charges, 0.03% per year while the category average is 0.33%. Less money toward annual management fees means more money in your pocket.

3. Don’t fight the market. Accept the fact that it is highly unlikely that you will beat the market, so choose highly diversified low fee investment funds for your portfolio.

4. Choose your asset allocation carefully. Divide your investment pie among stock index mutual funds or ETFs, and fixed income investments like bonds and cash. Plan your investment pie according to how much risk or volatility you can stomach. If you are risk averse and don’t like the ups and downs in value of stock investments then place a smaller percent in those types of financial assets and skew your asset allocation toward a greater percent in bonds and fixed income assets. Be aware that the opportunity for greater returns comes from taking on more risk. And more risk means a larger part of your pie invested in stock investments. If you want free investment management help in designing and managing your investment pie, check out one of my favorite investment platforms, M1 Finance.

Automatically invest for retirement with a tax-advantaged brokerage account. Custom-build your portfolio or choose a pre-made Expert Pie based on your long-term goals.5. Stick with your plan through market downturns. No one has a problem when their investment values surge. The problem comes when fear kicks in and you get scared during market downturns. I know more than a few folks who let fear get the best of them and sold during market downturns only to miss the subsequent rebound.

If you sell during a market downturn, you have to be right twice, once when you sell and another time when you buy back in.

6. Seek investment advice from a financial advisor or robo-advisor. Financial advisors can offer support with your investment decisions including crafting long term goals and saving strategies. Ellevest offers a low-fee robo-advisor with access to discounted financial advisory advice. While WiserAdvisor will match you with three fee-only, vetted financial advisors.

Women, Become a Millionaire in 25 Years of Investing

Women, start at age 40 and become a millionaire by age 65.

Even if you have not begun investing and have nothing saved at age 40, it is possible to reach $1,000,000 by age 65. You invest $1,236 per month in a portfolio equally divided between a U.S. stock index fund, an international stock index fund, and a Treasury Inflation Protected Securities (TIPS) fund. You can choose a mutual fund or an ETF.

Review; Quicken vs. Empower – Which is the Best Money Management Tool?

Assume historical returns prevail. If you earn 6.9% annually, then at the end of 25 years, your $370,800 investment will be worth $1,000,000.

Of course, if you start investing younger, you can achieve $1,000,000 with less money.

Start at age 25 and you only need to invest $385 per month to achieve $1,000,000 by retirement. And if your employer kicks into your 401k retirement account, you can invest less and still reach $1,000,000 or more by retirement.

Realize that fear is normal. But, don’t let your apprehension stop you from wealth building.

Start investing today to take care of your financial tomorrow.

Women Investing Resources

Here’s some help to get you started with your investing:

- Best Investment Advice for Millennial Women

- Free microbook; How to Invest and Grow Your Wealth

- Free budgeting, cash management, retirement planning, investing dashboard (I use this myself). Sign up required. Sponsored by Empower.

FAQ

The best investment for a woman is a well diversified stock and bond market portfolio. For example, depending upon your risk tolerance, and age, you might invest 70% in an all world stock market ETF like VT, and 30% in a broadly diversified bond fund like BND. Read more about asset allocation in this free microbook.

Open a Roth IRA and invest in a broad US or US and International stock ETF. You might choose either the Vanguard Total US Market ETF, VTI, or Vanguard’s all-world ETF VT. Since this investment is for long term growth, you can expect high single digit annualized returns over the upcoming decades. .

A 2018 MassMutual Womens Risk Survey found that women typically invest in diversified portfolios and take on less risk than men. Extrapolating from this research, you might expect women to invest in stock and bond fund portfolios, in line with their risk tolerance levels. This might include target date funds or passively managed stock and bond index funds. Women also gravitate towards investing with financial advisors, according to the MassMutual Survey.

If your workplace offers a 401k or a 403b account, that is an ideal vehicle for your investments. Within that retirement account, you might choose a target date fund or several low-fee passively managed stock and bond mutual funds. It’s also helpful for new investors to familiarize themselves with the investment basics. You can learn more about how to invest in this free microbook called Invest and Grow Your Wealth or other investment information websites such as Investopedia or Morningstar.

Related

Become A Millionaire In One Step

Quicken vs Empower – Which Is The Best Money Management App?

Historical Stock And Bond Returns

Actionable Investing Tips – Best Strategies For Long Term Investing

Sources:

https://www.massmutual.com/global/media/shared/doc/mm-womens-risk-study.pdf

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.

3 thoughts on “Investing for Women-Best Personal Investment Strategy”

Thank You for sharing this amazing article as I was looking to Invest.

Really great information, thanks for sharing this.

Hi Barbara,

This is Brij.

If you are at my life stage who has lots of ETFs in both the Rollover and Roth Accounts. How to cut down to Make like your portfolio?

Comments are closed.