Save $10K in Year – Tips and Strategies

Before you research how to save $10,000 in less than a year, you need to be clear on your reason for saving money. Are you trying to create an emergency fund or bulk up your retirement account? Or perhaps you just want to stop living from hand to mouth.

In any case, as you embark on your challenge to save money, you’ll probably learn a lot about yourself. When you examine your spending, you’ll find out how it matches up with your income. As you look for ways to cut back, you’ll discover what you care about. For example, you might find that you’re spending a lot of money eating out or buying expensive food. Perhaps instead of eating cheaper products, you simply find ways to buy in bulk. Perhaps you can take up cooking, creating dishes better than your usual restaurant fare.

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

Overall, once you examine your income and expenses, you’ve taken the first step toward your $10,000 in a year goal. You’ll be on your way to changing aspects of your lifestyle, creating new habits and ultimately controlling your personal finances.

Invest and Earn Compound Interest

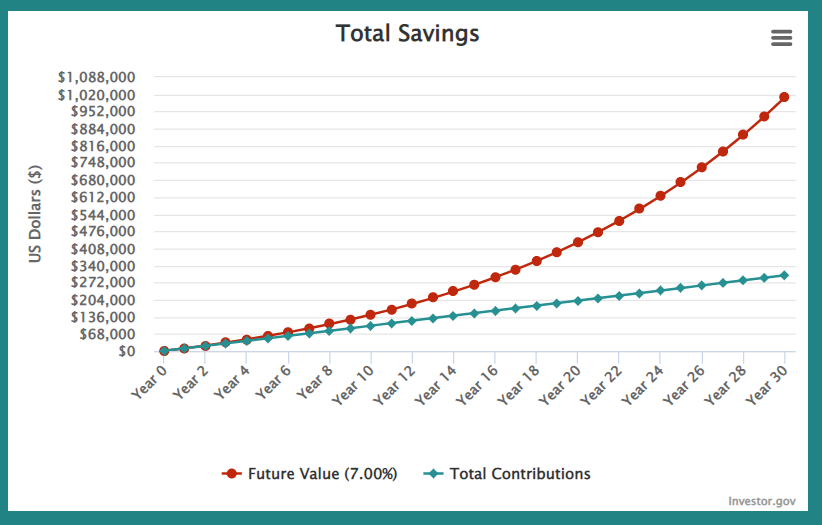

Even if you don’t need $10,000 for a specific something, just having that extra cash by the end of the year can really change your future. Consider this: the Social Security Administration’s Office of the Actuary uses a figure of 7% as the real return of the stock market per year. So, $10,000 invested at 7% per year is an extra $700 per year in passive income.

Seven-hundred dollars might not sound like a lot, but when you apply compound interest to the equation, things start to look really good. With compound interest, you are assuming that you are re-investing your gains. So, that $700 you make after one year of investing forms the new principle along with your original $10k, giving you $10.7k to invest: $10.7k invested at 7% is $11,449 at year end.

To earn this 7% return, choose to invest in a mixture to stock and bond exchange traded funds (ETFs). These lazy portfolios will give you some ideas.

Continuing with this example, you’ll hit approximately $12,250 in year 3; $13,108 in year 4; you’ll have doubled your money by year 10; you’ll hit seven figures or $1,009,419 after 30 years.

Value of $833.33 Monthly Investment – 7% Average Annual Return (compounded quarterly) After 30 Years

That’s the power of compound interest. And – even better – the Social Security Administration’s Office of the Actuary’s 7% figure might be a conservative one. Over the past century, the stock market has returned an average of 9% – all the more reason to find reason to engage on this financial journey.

Keep Your “Why” in Mind

This is what it boils down to: Today’s consumption is inversely correlated to tomorrow’s financial security. In other words, every time you avoid spending today, you are bolstering your future financial security.

10X Rule

Your $100 savings today is worth $1,000 for retirement (assume 7% average annual return invested for 30 years). So, think about the cost of the dollars you choose to spend today and consider whether a $100 dinner out with your partner is worth giving up $1,000 to spend in your later years.

My background is in psychology. I remember in graduate school reading several studies on how people save money. I applied the most useful techniques to myself, and that was actually when I started investing.

Here are a couple of science-backed tips to increase your willpower to save money:

- People are more likely to save money when they have a tangible future need for money, like a big vacation or home down payment. Make a list of future expenses and review them occasionally. Keep those future financial goals in mind when making payments for non-related things today.

- If you your plans change and you choose not to make the purchase in the future, you’ve still saved the money.

- Know your future self. Studies have shown that “connectedness to your future self” is a determining factor to whether you save money. Do some journaling to imagine your life in the future. How will you be the same? How will you be different? Try out aging software to visualize what you’ll look like in the future, science has shown this to be an effective method of saving money.

In the end, the key mental factor to saving money effectively lies in respecting your future self. Ask yourself if you want to be worrying about money in 20 or 30 years, or if you’d prefer to cut back a bit today to improve your financial security later.

How Much is $10k per Month? A Realistic Approach to Saving $10k in One Year

Saving $10,000 sounds like a lot of money. That’s why we break it down into terms that are easier to imagine. We can start by thinking in smaller terms. If you want to save $10,000 by the end of the year, save monthly, weekly, or daily:

- $834 per month

- $90 per week

- $27 per day

So, if you can save about $30 per day – or if you can make an extra $30 per day – you’ll have your $10,000 in a year.

How to Save $10,000 Fast

Okay, so you are ready to tackle your savings goal of $10,000. Here is a quick place to start implementing the top strategies to make $10k in one year:

- Automate all saving and investing. Set up regular payments from your paycheck and checking account into savings and investing accounts. If your monthly income goes directly to your bank account or brokerage account, you won’t have that cash burning a hole in your pocket.

- Reduce your monthly bills. Here are ideas:

- Cut your TV cord. Most people can get their entertainment just as easily for free online.

- Change your phone plan. If you’re using WiFi a lot, you probably don’t need an unlimited data plan.

- Shop around for a better car/home insurance plan. Insurance companies are extremely aggressive about sniping competitors’ clients and will help you find a cheaper rate. Billshark is a good service to help you slash your bills!

- Create a budget. If you’re not measuring your monthly expenses, you are probably engaging in wasteful spending, even if you don’t think you are. To save $10,000, you really need a plan.

- Ditch your non-cashback reward cards for cashback reward cards. Some credit cards have nice perks, but if your goal is making money, you ought to be using cashback reward cards.

- Pick up a side hustle. Even an extra $15 per day is halfway to your goal.

Flipping Websites is one strategy to bulk up your side-hustle income and get you closer to $10k in a year!

10 Ways to Save $10k in One Year

Here are ten ideas to make $10,000 dollars in one year or less and reach your savings goal.

1. Contribute at Least 10-15% of your income to your 401k account.

It’ll hurt for the first month or two, but after that, you won’t miss it.

Within reason, you should be contributing at least enough to your 401k account to receive the employer match. This effectively doubles the amount you are saving. Of course, if you have high-interest debt, you will want to pay off the debt, before engaging in this step.

2. Contribute to an IRA Account

An IRA is an important vehicle for financial independence. It provides favorable tax benefits and enables your contributions to grow tax-free or tax-deferred. You should try to max this out investment account every year so that you can avoid some of the damage the tax man inflicts. See the source below, for this year’s IRA contribution limits.

3. Contribute to an Investment Brokerage Account

Of course, you could store your cash in a checking account or savings account, but to maximize your annual growth you’ll want to contribute to an investment account. With small amounts of extra income, you probably want to limit yourself to either a robo-advisor or low-fee index funds. Both are easy to set up via your brokerage account and can definitely grow your money faster than within a high-yield savings account.

M1 Finance is a good option for those who want pre-made investment portfolios and the opportunity to invest in stocks and ETFs tool. It’s a good investing app for both experienced and beginner investors.

4. Slash Unnecessary Expenses

Every time you pay a bill or purchase a product, ask yourself if you really need it. We want many things but need little; don’t trick yourself into believing you need something that is actually just a “want.” An easy trick to cut expenses is to delay purchases: Hold off on a purchase for a couple weeks. After a couple of weeks, you might decide you don’t want it after all – or you might be able to find a cheaper alternative.

Billshark is an easy way to eliminate uneccesary subscriptions and negotiate for better prices on insurance and other expenses.

5. Prioritize Experiences Over Things

Buying experiences is better than buying things – psychological studies have proved this. Here is an excerpt from one study on the subject:

“Compared to possessions, experiences lead to greater satisfaction, less regret, especially when the outcome of the experience is positive. experiential purchases, such as a meal out or theater tickets, result in increased well-being because they satisfy higher order needs, specifically the need for social connectedness and vitality — a feeling of being alive.

“These findings support an extension of basic need theory, where purchases that increase psychological need satisfaction will produce the greatest well-being,” said Ryan Howell, assistant professor of psychology at San Francisco State University.

Source: https://www.sciencedaily.com/releases/2009/02/090207150518.htm

Spending money on things is so easy compared to experiences, which typically requires planning before you spend money, by prioritizing experiences over things you’ll naturally find you’ve curtailed your day-to-day spending, and likely increased your life satisfaction.

6. Use a Round-up App

If you are struggling to meet your money-saving goals or if you believe that you just don’t have enough extra money to save, try using a round-up app. For example, Acorns is a round-up app that works by rounding up your purchases to the nearest dollar. The difference between the amount spent and the nearest dollar is transferred into your investment account to grow for the future. In this way, you can seamlessly invest your money as you spend on everyday items.

This is another small strategy to contribute to your $10k in a year goal. Add this to saving in retirement and investment accounts, cutting spending and creating a side-gig, and you’re on your way to reach your $10k per year savings goal.

7. Ask for a Raise

Today, as inflation spirals out of control, companies are willing to raise employee compensation to meet with the increasing expenses of the average household. Consider renegotiating your salary for bonus money or an annual increase to make your $10,000 in a year goal more achievable. Ensure you present evidence documenting your value to the company and explain how giving you a raise will help the company meet it’s objectives.

Be strategic when you ask for a raise. Have an ideal amount in-mind (e.g., 20% higher) as well as a deal-breaker amount (e.g., no raise means you walk). Having another job lined up beforehand is also a good bargaining chip.

8. Work a Side Hustle

The path to your financial goal can either be lined with money-saving steps, money-earning steps, or a combination of both. Consider working a side hustle, either trading time for extra money or by running a passive income side-hustle. Check out our make money resources. Here are some quick, side gig ideas:

- Become an app/software/game tester.

- Grow some pumpkins in your yard to sell for Halloween.

- Teach a cooking/music/art class online.

- Sell stuff online via Etsy or eBay.

- Do some freelance programming/consulting/repairing.

- Become a tutor.

- Walk dogs.

- Babysit.

- Become an Uber/Lyft driver.

- Upload pictures to stock photography sites.

- Use Mechanical Turk.

9. Pay off Debt

Pay off your debt before you start saving money. Debt might not seem so bad when your financial situation is good, but during downturns, debt can really impede your savings journey. Ensure your credit card debt is handled in your monthly budget, and you’ll find that over time you’ll have more financial freedom.

If you’ve got high yield credit card debt and you’re paying 18% interest per year, then paying off $1,000 debt will save you $180, that could be transferre into an investment account. Investing the $180 will be yield $1,800 for your future self. (assume 7% average investment return over 30 years).

10. Move

Many people don’t have a great reason for living where they do. Most people in history simply live where they were born. If you are serious about your goal to save money, consider whether the housing costs, food prices, and other expenses in your current area are reasonable for you. Moving to Las Vegas or Portland from New Jersey or New York, for example, could lead to you successfully saving $10,000 in a single action.

Especially with the recent “work from home” trend, many employers are comfortable with remote employees. You could save $10,000 in living expenses by simply moving from California to Nevada.

How to Save $10,000 in a Year – Wrap Up

With a savings goal of $10,000, first remove obstacles that impede your goal including high yield debt, high living expenses, monthly maintenance fees, excess family member responsibilities, high cost cell phone bill and unnecessary online purchases. That’s a lot to deal with, but once those cash drags are out of the way, you can focus on building up $10,000.

If you have free time, the easiest path to financial success is likely a side hustle. If you’re strapped for time, you can often succeed in saving $10,000 just by cutting out your biggest expenses and unnecessary monthly payments. A tax refund or a debit card cashback program can really help in saving $10,00, too.

Ensure you are aiming for retirement savings so that you can start investing with tax benefits early. Breaking $10,000 in a year down to a weekly savings goal can make the process seem easier. And on the subject of ease, online banks that allow automated transfer and roundup apps that allow for direct deposit can reduce the barrier to investing. From there, to save $10,000 is just about having enough money to invest and earn compound returns.

Related

- Make Money With A Blog – Is Blogging Dead?

- 51 Ways To Drastically Cut Expenses

- What Percent Of My Income Should I Save?

- Where To Start Investing For Retirement?

- How Can Investors Receive Compounding Returns?

Sources:

- What stock market returns to expect for the future? https://economics.mit.edu/files/637

- Connecting to Your Future Self https://academic.oup.com/gerontologist/article/55/Suppl_2/311/2491734?

- IRS.gov IRA contribution limits https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-ira-contribution-limits

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.