What is a Checkbook IRA?

A Checkbook IRA includes the features of a traditional or Roth IRA, but has one distinct difference: the account holder, not a custodian, has control over the investments. This makes Checkbook IRAs a good option for hands-on, confident investors. It lowers the amount of fees paid to account custodians and makes access to your IRA quicker and easier.

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

Checkbook IRAs are also good choices for investors who want to own nontraditional investments within the account, like foreclosures, gold, raw land, and even LLCs.

However, there are many rules surrounding Checkbook IRAs, including limitations on some investments and hefty fees for breaking the rules. For this reason, checkbook IRAs are not good options for novice investors.

If you value flexibility and speed, and have some investing experience under your belt, you might be a good candidate for a Checkbook IRA.

Here’s an easy way to find a fiduciary financial planner who might offer a checkbook IRA:

if you’re in the market for a vetted “fee-only or fee-based” financial advisor, I’ve entered into a partnership with WiserAdvisor. This is a quality matching service for those who might be seeking a fee-only financial advisor.

“WiserAdvisor.com is an independent matching service that helps individuals find the best financial advisor for their unique needs. WiserAdvisor has successfully helped over 100,000+ individuals like you find their ideal financial advisor since 1998.

Click Here for 3 WiserAdvisor Vetted Financial Advisors in Your Area!

In order to join the WiserAdviser network, each and every advisor must pass a three-step qualification process. WiserAdvisor screens advisors based on their years of experience, their SEC/FINRA registration and records, and their compensation criterion. All advisors on our network are fee only or fee based.”

Answer a few quick questions and you’ll get three advisors in your area to interview.

What is the Difference Between a Self-Directed IRA and a Checkbook IRA?

Self-Directed Individual Retirement Accounts (SDIRA), which can be set up as Traditional, Roth, or SEP IRAs, are different than regular IRAs because of the types of investments they allow. SDIRAs are much more customizable than regular IRAs, as the investment options are substantial.

You can open a Self-Directed Roth IRA or Traditional IRA, with the same tax benefits as their regular IRA counterparts.

In all cases, the account holder manages the SDIRA investments. Account holders choose the investments from a wide variety of options, and, traditionally, the funds for those investments must be administered by custodians. Since the custodian is responsible for handling these transactions, SDIRA clients can occasionally experience delays in buying and selling their investments.

A Checkbook IRA is a variation of the SDIRA that can eliminate these delays. Checkbook IRAs are different from regular SDIRAs in that the custodian only handles account setup; after that, the account holder writes checks to make investments on behalf of the IRA.

Example: Rocket Dollar Self-Directed IRA

The differences between a Checkbook SDIRA and a SDIRA are most clear when looking at Rocket Dollar’s Core and Gold packages. Core and Gold both have the same basic features:

- $0 minimum deposit

- An LLC for investments

- Investment management tools

The Checkbook IRA has many more features than the regular Self-Directed IRA, however, including:

- A checkbook and debit card for account access

- Expedited transfers

- 4 free wire transfers per year

- Tax filing assistance (1099R and Form 5500)

How Does a Checkbook IRA Work?

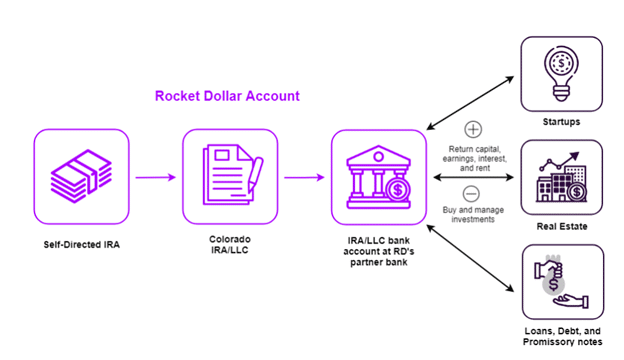

A Checkbook IRA is a bit different than a regular Self-Directed IRA (SDIRA). Checkbook IRAs own a Limited Liability Company which is opened specifically for the purpose of funding the IRA. This LLC is set up by the custodian, just like in a self-directed IRA, but that’s about where the custodian’s responsibilities end.

Once the LLC is created, transactions can then made by the LLC owner, who is typically the account holder. This translates to fewer fees since the custodian only handles account setup, not ongoing transactions.

As the name implies, a Checkbook IRA gives investors the ability to fund investments just by writing a check. Any investment allowed by the IRS is fair game. Investors no longer need to wait for custodian approval; they simply write out a check for the investment.

Not all financial companies offer SDIRAs, however; fewer still offer checkbook control.

Rocket Dollar is one of a few companies with Self-Directed and Self-Directed Checkbook IRA options. They stand out in the Checkbook IRA category because clients can write checks or use an account debit card to make investments for their IRA. These options speed up the investment process and eliminate the need to wait for account custodians to make purchases on behalf of the account holder.

What Type of Investments Can I Own in a Checkbook IRA?

Checkbook IRAs offer many investment options, from the more predictable options (stocks, bonds, and mutual funds) to more obscure offerings (private businesses, for instance).

Land and Property Investments

- Single or Multifamily Rental Properties

- Undeveloped Land

- Farmland

- Residential or Commercial Real Estate

- Foreclosed Property

Loans, Debt, and Deeds

- Mortgages/real estate loans

- Private loans

- Business loans

- Direct investments into community businesses

- Tax liens

- Deeds, such as timber deeds

Companies and Partnerships

- Limited Liability Companies (LLCs)

- Limited Liability Partnerships

- General partnerships

- Joint ventures

And more!

- Livestock or cattle certificates

- Racehorses or other competition animals

- Precious metals

- Gold

- Most currencies, including cryptocurrency

- Crops and harvests

- Certificates of Deposit

- Mineral rights for oil and gas

Excluded Investments

It may seem like anything goes when it comes to self-directed IRAs, but that isn’t quite true. The IRS does not allow IRA owners to invest in the following categories:

- Collectables, such as stamp collections

- Alcohol, such as fine wine

- Gems, Coins, or Metals (except those on the list of approved precious metals)

- S-Corp Stock

- Rugs

- Life Insurance

Some other banks specifically prohibit investments in cannabis and ATM-driven businesses as well.

How Should I Choose the Investments for My Self-Directed IRA?

SDIRAs allow for greater diversification than your standard stock, bond, and mutual fund IRA. That’s good news for investors, but there is one big downside: the potential for Paralysis by Analysis. How do you choose your SDIRA investments with so many options?

Financial experts agree that the best investment strategy is one that diversifies your investment streams. Diversification offers some protection from market downturns, as it’s unlikely – though not impossible! – that all your investments will lose value at the same time.

A diversified SDIRA might start with basic stock and bond investments, then add some foreclosed property, a Certificate of Deposit, and mineral rights to the mix. These additional investments might be chosen based on current market conditions or world events that are likely to affect these investments.

However, it’s important to do your due diligence.

Before jumping into any investment, make sure that it doesn’t violate any IRS rules for prohibited transactions; you also cannot live in any property investments.

If you have an SDIRA with custodian oversight this may be easier, as the custodian has final approval on investments. However, Checkbook SDIRAs lack custodian oversight. The responsibility for knowing and following the rules rests solely on the account holder.

How Do I Choose the Best Investments for My Self-Directed IRA?

In the investment world, the “best” investments are hard to pinpoint. Everything fluctuates; even investments that are performing well now might suddenly drop tomorrow.

To give your portfolio the best chance at growth, however, you’ll want to follow these three guidelines:

Invest in Diverse Industries

We all know the adage: never put all your eggs in one basket. While in regular IRAs that might mean choosing stocks from diverse industries, SDIRAs have the benefit of allowing more unique diversification.

For even greater diversification, consider branching out from your comfort zone. For example, even if your portfolio tends to be conservative you might consider adding some more aggressive or potentially volatile investments to the mix.

Just keep the percentage of speculative investments to an amount that you can afford to lose.

Follow Your Strengths

If you’re familiar with a specific industry or product, it’s possible you can invest in it. Using your familiarity with market conditions within this industry can help you to make smart investment decisions. For example, investing in racehorses sounds like a great investment, and it can be – if you know things about racehorses!

Consider Your Timeline

The best Checkbook IRA investments will be those that match your retirement timeline. When the time comes to take a distribution, you need to be ready; if you miss a required minimum distribution because an investment isn’t ready to pay out, you can get hit with hefty taxes or penalties.

Make certain to understand the liquidity of the investment and when it can be redeemed for cash. Keep your retirement timeline in mind as you choose long- or short-term investments.

Where Can I Open a Checkbook IRA?

Rocket Dollar offers Custodian Controlled IRAs for $15 per month, with a $360 set up fee. Clients who want checkbook control will pay a one-time $600 set up fee and $30 per month. There may be occasional transfer fees, but Checkbook IRA clients can expect 4 free wire transfers per year.

Innovative Wealth is a financial advisory firm that specializes in alternative assets and unique investment strategies. Unlike Rocket Dollar, investors at Innovative Wealth receive individual financial planning services as well as the opportunity to invest in alternative assets within an IRA.

Broad Financial partners with Madison Trust Company to provide Custodian Controlled and Checkbook Controlled IRAs. Their Custodian Controlled IRA has a $100 set up fee and charges $75 per quarter; there are also transaction fees attached to this account. Their SDIRA with Checkbook Control has a hefty set up fee of $1,295, which may vary depending on the LLC set up fees in your state; they also charge $75 per quarter, but do not have transaction fees.

There are many other firms that specialize in checkbook IRAs.

How to Open a Self-Directed IRA

Let’s look at how to open an SDIRA, using the Rocket Dollar Self-Directed IRA as an example.

The whole set-up process can be completed online. The first two steps are easy: first, create an account at Rocket Dollar, which will take approximately 5 minutes. Rocket Dollar team members create your IRA and will send documents for e-signatures within the next few business days.

Though Rocket Dollar has no minimum investment amount, you will need to fund your account through a transfer or contribution request. This can be completed once all e-sign documents are taken care of.

After the account is funded, Rocket Dollar opens an LLC checking account on behalf of the IRA. This is done through a bank partner. Once the LLC is created, any transfer or rollover money from the funding stage will be moved into the LLC bank account.

Finally, you’re ready to invest!

Rocket Dollar estimates this whole process will take 2-4 weeks to complete. This may seem long, but they note that this includes potential delays rolling over existing IRAs.

What Fees Can I Expect?

SDIRAs require a bit of initial set-up, and usually come with a one-time fee to the custodian who helps create the LLC required for an SDIRA. That fee can change, however, based on the type of account you’re opening. At Rocket Dollar, a custodian managed SDIRA has a one-time fee of $360; that fee increases to $600 for clients who want to set up a Self-Directed Checkbook IRA.

After this initial setup, however, Rocket Dollar charges only a monthly fee of $15 for their Core plan (Self-Directed, but no Checkbook) or $30 for Gold (Self-Directed Checkbook IRA). There are no additional management or investment fees. Transfer fees may apply in some cases.

How Many IRAs Can You Have?

There is no limit to the number of IRAs you can have, but there is a limit to the contributions you can make!

Regardless as to how many IRAs you have, the contribution limit is $6,000 for 2019 and 2020. Individuals 50 and over can make an additional $1,000 in catch-up contributions as well.

Although business Simple and SEP IRAs have higher contribution limits.

Is There a Benefit to Having Multiple IRAs?

In some cases, multiple IRAs can be beneficial.

There is constant debate on whether Roth or Traditional IRAs are best. If you predict your income growing substantially before retirement, you might consider having one of each.

Roth IRAs are funded with post-tax money. Because you pay taxes on your contributions before they’re invested, your money gets to grow tax-free. Your withdrawals are tax-free as well if you’re at least 59 ½.

Traditional IRAs are funded with pre-tax money. What you save in taxes now, however, is paid later: your withdrawals will be taxed.

If you’re just getting started in your career, making post-tax contributions to a Roth IRA might be beneficial. Once you move up into a higher tax bracket, switching your contributions to a Traditional IRA will lower your taxable income and potentially bring you into a lower tax bracket.

Regardless of the type of IRA that you have, the investments owned within the account grow tax free!

Pros and Cons for a Checkbook IRA

Checkbook IRA Benefits

There are four main benefits to a Checkbook IRA: cost, speed, flexibility, and return.

- Cost

Because the LLC owner handles all the transactions, monthly and transaction fees are reduced. This is similar to how robo-advisors work: lower fees are possible when there is less overhead or direct human oversight. After the initial set up fee, Checkbook IRA owners can pay less than SDIRA owners because they are essentially the account custodians.

- Speed

Checkbook access to IRA funds means that you can invest as soon as an opportunity appears – no more waiting for custodian approval or slow-moving funds. This is particularly beneficial for investors who are looking at real estate, which has been moving even more quickly than normal as of late.

- Flexibility

The IRS allows for extremely diverse investments – options that most regular IRAs do not have access to. Through this increased flexibility, investors can tailor their investments to best meet their goals and values.

- Return

Ultimately, since the investments grow tax deferred, your returns might be higher within the checkbook IRA than they would be if owned outright.

Downsides to a Checkbook IRA

With so many benefits, a Checkbook IRA might seem like a no-brainer. There are a few things to be wary of, however.

- Surprise costs

There may be additional costs associated with the Checkbook IRA LLC. As an LLC, you will need to have a Tax ID number and good recordkeeping for your IRA. You will also incur other expenses if you decide to hire out these responsibilities.

Some SDIRA providers, like Rocket Dollar, mitigate these concerns by having a transparent fee structure. Rocket Dollar’s Checkbook IRA can be set up for a one-time fee of $600, with fees of $30/month after that. They also allow up to 4 free wire transfers each year, so no surprise fees there!

- Fees for prohibited transactions

Checkbook IRAs are not for novice investors, and for good reason – if you make a mistake, you can get some hefty fees! Early withdrawal penalties and loss of tax-advantaged status are possible consequences for investing in a prohibited investment category or misusing an investment. For example, Checkbook IRA owners can purchase vacation property for the IRA but they cannot vacation in this property.

- Lack of oversight

SDIRAs do not usually come with investment advice. Since the custodian’s role ends once the Checkbook LLC is created, Checkbook IRAs don’t have custodial oversight in the way other IRAs might. This is not necessarily a problem, particularly for experienced investors. However, it can be a downside for novice investors who need more guidance or lack familiarity with IRS investment guidelines.

Checkbook IRA Wrap Up

It’s clear that Checkbook SDIRAs have a lot to offer. Is this the right fit for you, though?

Self-Directed IRAs with checkbook control are a good fit for clients who want the flexibility to manage their own investments, prefer to branch out into less traditional investments, and who like being able to make investments on their own time.

These accounts are not a good fit for investors who want a more passive investment strategy or who are new to investing. Checkbook IRAs may also include additional fees and often come with a larger set-up fee, which means clients will need cash on hand to get started.

In most cases, the benefits to an SDIRA will outweigh the potential downsides. This is particularly true when the myriad investment options are considered. With the ability to invest in anything from livestock to real estate, clients will be able to craft diversified portfolios that offer the possibility of beating the market.

Related

- You Don’t Need an IRA – There’s Always Social Security

- Is a 401k the Same as an IRA?

- Should I Contribute to Roth IRA or a 401k if I Can’t Fund Both?

- Vaulted Review-Physical Gold Investment App

- Retirees: What To Do When You Have Enough?

- Retirement Planning Tips For 50 Year Olds

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.