“Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.” ~Albert Einstein

This Albert Einstein compound interest quote sums up the power of compounded returns. The wealthiest individuals harness the power of compound interest and returns to turn earned income into growing wealth. Ever wonder how compound interest works with stocks, whether mutual funds compound, or the best compound interest investments? Learn how compound interest can work for you.

What are Compound Returns?

A compound return is simply your return on investment over a specific period of time. The “compound” part refers to the reinvestment of your gains. If you’ve had a savings account, you’ve seen compound interest in your statements, albeit to the degree of pennies on the dollar (if even that).

An easily understood example of significant compound returns is a dividend reinvestment program. In such a program, the dividends from your investment are reinvested into the stock or fund generating those dividends, essentially increasing your capital, thereby leading to even more gains. A simple compound interest example follows.

- You invest $4,000 in a dividend stock paying a 6% yield annually. You are enrolled in a dividend reinvestment program so that your gains are added back to your investment (not set aside as profit).

- After one year, you have $4,000 x 1.06 or $4,240.

- After two years, you have $4,240 x 1.06 or $4,494.40.

- After three years, you have $4,494.40 x 1.06 or $4,764.06.

When you reinvest dividends, all future returns are added to a growing base. In year one your investment grows to $4,240. In year two, you’ll receive your 6% or $240 added to the year one $4,240 for a new value of $4,494.40, after just two years of compounding. Over time, the same percent return is applied to a larger and larger principal amount.

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

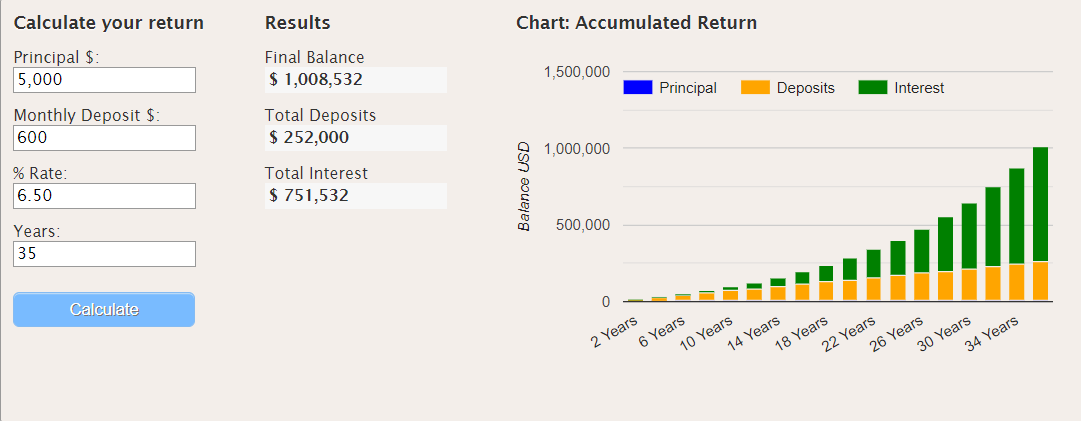

Compound Return Quadruples Your Money

source; helpfulcalculators.com

It’s hard to believe that over 35 years, with just $600 per month deposit you can become a millionaire. Start at age 30, invest $600 per month for a total contribution of $252,000 and compound returns gives you $751,532 in interest.

Dividend reinvestment is only one of a large number of investment strategies that aim for compounding returns. Let’s take a look at some of your other options.

How to Invest for Compounding Returns in 2023

Your compounding interest and returns are influenced by your individual preferences and risk tolerance. Consider these four popular methods of growing your wealth with compounded returns:

1. Exchange Traded Funds

Exchange Traded Funds, or “ETFs” for short, are great choices for investors with long-term time horizons, investors such as young people just beginning to amass capital or those who desire a low-cost method for owning a variety of stocks or bonds. An ETF is usually just a basket of stocks (or bonds) that share something in common, such as being in a certain sector or betting on the market moving in a certain direction. Some ETFs simply track major market indexes like the S&P 500 or the Nasdaq 1000. They often come with monthly or quarterly dividend payments that can be reinvested.

They also work well for investors who do not fear the occasional pullbacks in markets and can accept variance in their accounts, just as long as the long-term direction is upward (and it usually is). As most ETFs are stock-based, you should expect fluctuations in their value. But with that risk comes reward, as more volatile investment vehicles typically come with a risk premium, or greater gains than less volatile investments. A counterargument to this is that ETFs can seem less risky since your investments are spread over many assets – i.e., diversification. Ultimately, your risk tolerance will influence whether compound interest ETFs should be your vehicle for a buy-and-hold strategy that receives compounding returns.

Investment apps for ETFs:

- Sofi – Buy stocks, ETFS and crypto and chat with financial consultants.

- Robinhood – Buy stocks, ETFs and crypto.

- Acorns – Spare change investing with ETFS.

2. Dividend-Paying Stocks

Here’s how compound interest works with stocks. A dividend-paying stock is simply a stock that returns some of its cash flow to investors, via way of quarterly dividend payments. You can earn compounding returns by reinvesting these dividends back into the stock, as we saw in the example above. As a buy-and-hold strategy, dividend stocks can help investors receive compounding returns as a passive strategy. Dividend achiever stocks are those that have increased their dividends annually over a period of many years.

LIke ETFs, dividend-paying stocks work well for young investors aiming to grow capital over a long period of time. However, this is not at zero risk. In fact, investing in a single dividend stock is considered riskier than investing in an ETF due to the lack of diversification with this strategy. Of course, it all depends on the stock itself, but no stock is truly risk-free.

Investment apps for dividend paying stocks:

- M1 Finance – Stock and ETF investing with customized dividend portfolios.

- Sofi – Buy dividend paying stocks or dividend paying ETFs and chat with financial consultants.

3. Robo Advisors

In the past, investors turned to their local investment advisors for help with their own portfolios. But more recently, robo-advisors have surged in popularity due to their low fees and ease of access (financial advisors sometimes turn away clients with too little capital, while many robo-advisors have low-minimum investment requirements). Robo advisors come at a lower cost since they are predominantly automated. In essence, a robo-advisor frequently uses the same software that human financial advisors once employed for their clients, only now the process is automated and thus doesn’t need as much human oversight.

As robo advisors typically employ the same modern stock portfolio theories that financial advisors do, their focus is typically on passive investing, specifically that of earning compound interest on the initial investment without a lot of stock and bond trading. Most robo-advisors emphasize diversification and risk management. Yet as each robo-advisor is unique, your ideal course of action is to shop around before allocating your capital to the best robo-advisor for you.

Low-fee robo-advisors for compounding:

- Betterment – Low fee investment management and financial planning packages.

- Wealthfront – Digital investment manager with ETFs and crypto and $5,000 managed for free.

4. Compounding in Real Estate

Real estate compounding can take different forms. You might buy a real estate investment trust or REIT which pays dividends and trades on the U.S. stock market. You can reinvest those dividends back into the REIT, similar to reinvesting with an ETF or stock. Other ways to compound with real estate are to get in on the real estate crowdfunding trend. This is where you invest with companies who buy apartments, commercial, or various types of real estate. With real estate crowdfunding, you buy a share in individual properties or a company’s investment fund. Some crowdfunded real estate platforms also offer the opportunity to invest in real estate debt or mortgages. Just realize that your money might be tied up for several years with these crowdfunding platforms. Crowdfunded investments are typically less liquid than REITs, stocks or ETFs.

Real estate crowdfunding platforms:

- CrowdStreet – Invest in apartment buildings.

- Groundfloor – Invest in real estate debt.

- PeerStreet – Monthly income from real estate loan investing.

- AcreTrader – Invest in farmland.

Compound Return as a Passive Strategy: Choices, Choices

Choosing a method to generate interest payments on your initial capital can seem complex. Let’s discuss some of the most important issues at play.

First, your compounding interval helps determine the speed at which you grow your wealth. Monthly compounding (e.g., certain ETFs) generates wealth at a higher speed than quarterly compounding (e.g., dividend stocks), which in turn works more quickly than annual compounding (e.g., bonds).

Second, many sources of compounding returns require fees. Although mutual funds compound, they typically charge higher management fees than ETFs. The higher the fees, the less money going into compound compounded returns.

Third, whether you intend to touch the account can impact your income generation. Any withdrawal or deposit will affect the principal capital by which compound interest is generated. For example, if you have loan obligations, your withdrawals will work against you. However, if you can let the account sit alone, only adding via deposits, you will see your wealth grow much more quickly than otherwise. And compounding returns in a 401k or retirement account could provide additional tax benefits.

FAQ

Each interest-generating investment asset works differently. Usually, the compound interval is easily available through a little bit of research. Mutual funds, for example, usually offer fact sheets with this information. Stocks typically pay dividends quarterly. Funds are usually on a quarterly or monthly compound interval, with real estate investment trusts (REITs) more likely to offer monthly dividends.

The most obvious difference between mutual funds and ETFs is that shares of the former are purchased through a company while shares of the latter can be bought on the open market. ETF prices are more volatile, as they can be traded throughout the day, while mutual funds maintain a single price-per-share throughout the day, priced via its net investment asset value calculated after the stock market closes each day. There are roughly 8,000 mutual funds versus roughly 2,000 ETFs.

In finance, no investment comes with a 100% guaranteed return. A 401k or retirement account with a company-matching program is perhaps the closest thing to it. But other than that, even the assets that seem the safest still come with risk. Although a Certificate of Deposit provides a guaranteed return, Inflation could eat away at the ultimate value of your investment. In general, just remember that assets with higher compound interest rates are typically exposed to more risk.

In general, the dividend paid last quarter will be the dividend paid next quarter. Dividend payments are listed on popular stock websites like Yahoo!Finance. However, dividends are declared quarterly and can thus change every three months. Some companies consistently raise their dividends every year, while others keep the payments stable. Still others cut their dividends, to the dismay of many investors. Alas, dividend investing comes with several risks and requires either a high risk tolerance or a long enough time horizon to where the ebbs and flows of the stock price as well as dividends won’t hurt the investor.

Because investors who receive compounding returns can grow even small amounts of capital into large amounts of money due to the inner workings of compound returns themselves, investment methods utilizing compound interest are often recommended for young investors. However, compound interest investing also bestows benefits upon those planning for retirement. Simply put, as long as you have time to invest, you can employ compound interest investments.

In the end, the allocation of the funds in investment accounts is a personal choice. Low-risk compounding return sources, such as savings accounts, offer miniscule compound returns at extremely low risk; dividend stocks can pay out double-digit annual yields via compounding returns but come with a large number of risks, from market risk to dividend cuts. A determination of personal risk tolerance is a prerequisite for determining your investment vehicle. And no one said that you must choose a single source. You could certainly dedicate a portion of your investment account to high-risk compound return investments while placing the rest of your capital into safer avenues.

Related

Best Asset Allocation Based On Age And Risk Tolerance

How To Invest And Make Money Daily

Should A 30 Year Old Plan For Retirement?

Should I Invest In A Target Date Fund?

A Penny Doubled Every Day For 30 Days Or $1 Million – Which Would You Choose?

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.