TIPs Inflation Bonds – Protect Your Cash From Inflation

“Inflation is as violent as a mugger, as frightening as an armed robber and as deadly as a hit man.” Ronald Reagan

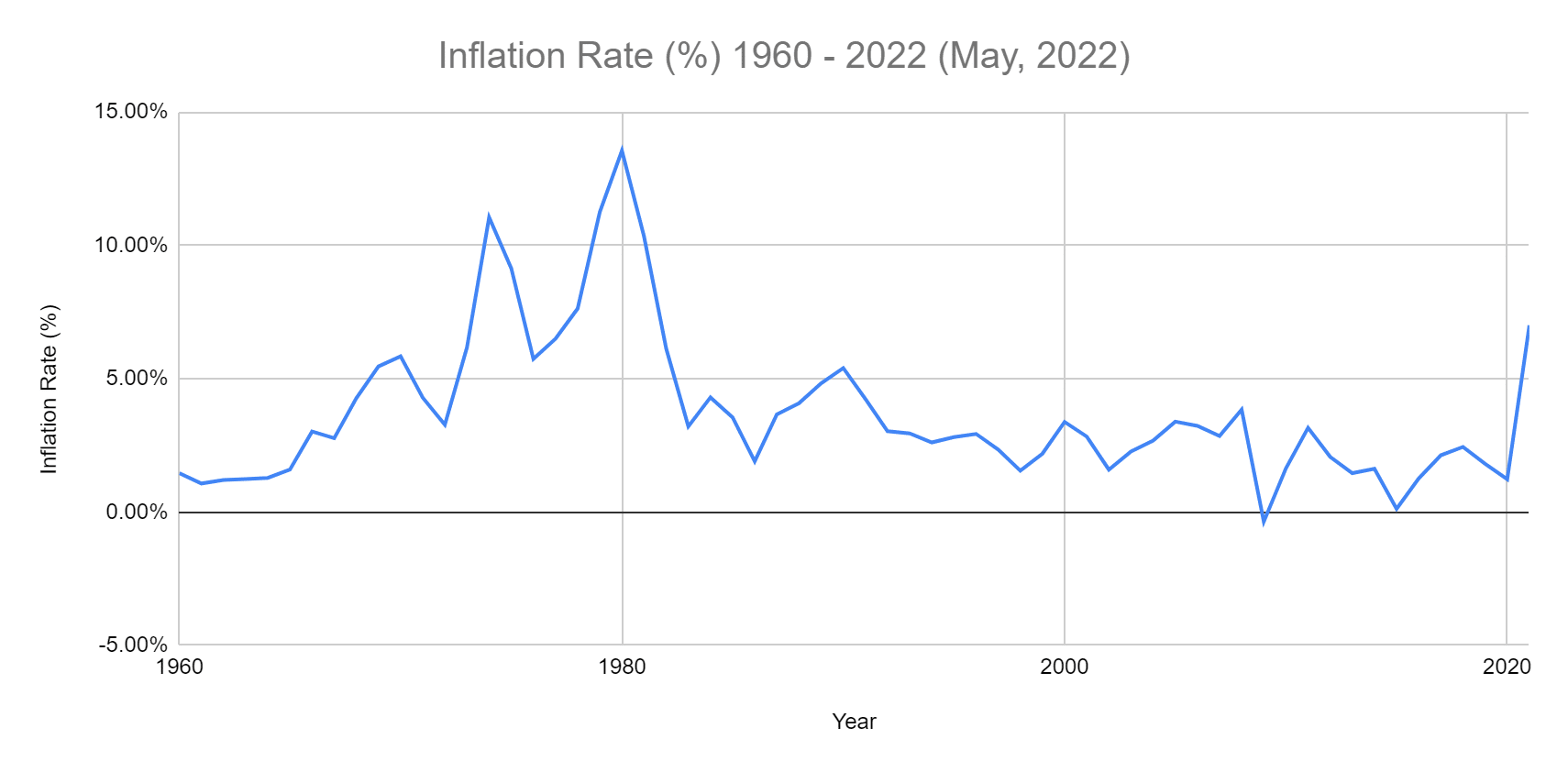

Inflation is rising as grocery, gas, and housing prices soar. That’s okay, as long as your salary matches the increase, which is unlikely. Compound rising inflation with volatile stock and bond prices, and inflation indexed bonds are gaining popularity. Treasury Securities, issued by the U.S. government, include I Bonds and TIPs or Treasury Inflation Protected Securities. These investments were created to provide inflation protection and preserve the purchasing power of your money, when inflation increases. In this article you’ll find out, What is an I Bond?, How to invest in inflation bonds, Pros and Cons of TIPS, and more.

What is Inflation Risk?

Inflation risk manifests insidiously when the same dollar purchases fewer goods and services. Another way to look at inflation is; the identical goods cost more and more. A CD (Certificate of deposit) is subject to inflation risk as the interest rate stays the same even though inflation may be rising. If you buy a CD playing 2% interest and inflation rises to 3%, then your money is losing 1% due to inflation.

One way to protect your cash from the ravages of inflation is to add inflation protected securities to your fixed income investments. Consider investing in TIPS, I bonds, or inflation-protected securities funds.

What are TIPs Bonds?

TIPS are bond-like investments issued by the US government. They have a fixed interest rate but they keep up with inflation because when inflation rises, the principal amount of the bond also increases. In contrast, when inflation drops, so does the principal amount of the bond.

TIPs inflation indexed bonds are issued in terms of 5, 10 and 30 years, in multiples of $100. TIPs bonds aren’t like a traditional bond, which is issued at face value with a fixed coupon, or interest payment. A TIPs bond is issued with a set interest rate. But, the principal value of the bond changes along with the rate of inflation, as measured by the Consumer Price Index or CPI. Throughout the life of the bond, you’ll receive the same interest rate, on a changing value.

TIPS pay interest twice a year, at a fixed rate. The rate is applied to the adjusted principal; so, like the bond’s princi value, interest payments rise with inflation and fall with deflation.

When a TIPS matures, bond you are paid the inflation-adjusted principal or original principal, whichever is greater.

TIPs Bond Example

If you own $1,000 in TIPS with a coupon rate of 1%, and there’s no inflation, then at the end of the year, you’ll receive $10 in interest payments. But, if inflation rises by 3%, the $1,000 will be increased by 3% to $1,030. The coupon interest rate remains the same, and is paid on $1,030 instead of $1,000. So after the 3% inflation increase, you’ll receive an interest payment of $10.30 for the year.

When the TIPS matures, you receive the greater of the adjusted principal, or the original principal. Even if there’s deflation, you never receive less than you originally invested.

In contrast, if you buy a typical ten-year bond for $1,000, with an annual coupon payment of 3%, paid semi-annually. You get 1.5% or $15 twice per year and in ten years, you receive the $1,000.

What Happens to TIPS Bonds When Interest Rates Rise?

All bonds are subject to interest rate risk, when interest rates rise. That means that when interest rates increase, the principal value of a bond will fall. The amount the principal declines depends upon the bond’s duration or implied maturity, among other factors. Longer duration bonds typically decline more than shorter duration bonds, when interest rates go up.

But, TIPS have an advantage in a rising interest rate environment, if inflation is present. Even if your TIPS bond falls in value, due to rising interest rates, the loss will be offset by the rise in the CPI or inflation rate.

Summary – What are Treasury Inflation Protected Securities (TIPS)?

- Buy a government bond and you are making a loan to the U.S. Government.

- In exchange for the loan, the government pays you interest.

- The TIPS bond interest rate is set at purchase and remains the same until maturity.

- The face value of the TIPS bond increases and decreases along with changes in the inflation rate, as measured by the CPI.

- The interest rate is applied to a higher or lower principal value. With inflation, when the bond’s principal amount increases, so will your interest payment.

- When the TIPS security matures, you receive the original or adjusted principal, whichever is greater.

A similar U.S. government issued inflation bond is the I bond.

How do I Bonds and TIPS Compare?

| TIPS | I Bonds | |

| Type of Investment | Marketable bonds-can be bought & sold though treasurydirect.gov or investment companies. Can buy TIPs funds. | Non-marketable. Bought through treasurydirect site, bank or some employers. |

| Face Amount (PAR) | Minimum $100 for individual TIPs bond. Fund price set by investment companies and supply and demand. | $25 or more. Can buy up to $10,000/year, plus an additional $5,000 with your federal income tax refund. |

| Interest Payments | Set semiannually-paid on adjusted principal | Interest is accrued over life of bond and paid upon redemption |

| Lifespan | TIPs funds can be held indefinitely. Individual TIPs can be held to maturity (5, 10, or 30 years) or sold prior in the secondary market. | Redeemable after 12 months (with 3 months interest penalty). No penalty after 5 years. Earn interest up to 30 years. |

| How they keep pace with inflation | The interest rate is set at the purchase date and stays the same.The value of the TIPs bond goes up and down with the inflation rate. | I Bonds receive a combined interest payment. The fixed interest rate is set when you buy the bond. Every 6 months the variable interest rate changes, based upon the inflation rate. |

How to Buy TIPS?

You can by TIPs bonds directly at the treasurydirect.gov website or through a bank or investment broker. To open an account, visit Treasurydirect.gov and choose the type of account. Input personal information including name, email, Social Security number, and banking details. Choose password and complete the security question.

You can also visit your investment brokerage account and select the fixed income section to find the appropriate links. To buy TIPS ETFs or mutual funds, proceed with the trade window at your brokerage account and key in the ticker symbol and additional information.

There are a range of inflation-protected securities funds available including:

- SPDR Bloomberg 1-10 Year TIPS ETF (TIPX)

- Schwab US TIPS ETF (SCHP)

- SPDR Portfolio TIPS ETF (SPIP)

- Vanguard Short-Term Infl-Prot Scs ETF (VTIP)

- PIMCO Broad US TIPS ETF (TIPZ)

TIPS Pros and Cons

Pros

- TIPS investments can diversify your portfolio, because they are less correlated with other types of investments and may reduce volatility.

- TIPS are safe from default. As long as the U.S. government is up and running, you’re safe from the loss of the principal value of your inflation bond.

- At maturity, even with the possibility of deflation, you will never receive less than the original face value of the bond. And, should inflation be higher at maturity, than at purchase, you’ll receive a higher principal value when the bond matures.

- TIPs bonds have tax benefits. The inflation bonds are only subject to federal tax, not state or local. You pay the tax in the year it is earned.

- You can hold TIPs until maturity or you can sell the securities in the open market through an investment brokerage company like Charles Schwab, E*TRADE, Fidelity, Vanguard, or TD Ameritrade. (The value might be higher or lower than at purchase.)

- TIPS are exempt from state and local taxes.

Cons

- When TIPS principal value increases, that amount is considered taxable income you are required to pay tax on the difference between the purchase price and the bond’s increased value, even though you won’t receive the additional principal until the bond matures, or is sold. This is called “phantom income.”

- A TIPS fund’s value, might differ from the worth of the bonds owned within the fund. When you sell shares in a TIPS fund, you might not receive the same amount as you paid for the initial investment. While individual TIPS held until maturity guarantee the return of your principal investment.

TIPS Bonds Wrap up

The best portfolio strategy is diversification. That means owning a mix of stock, bond, real estate and other investments. You never know which investments will perform best in the future, so owning a variety of assets will smooth out your portfolio’s volatility. During times of rising inflation, inflation protected bonds can be an important addition to your diversified investment portfolio. You can buy TIPS individually or in a fund for the fixed portion of your portfolio to preserve your capital. As inflation rises, so will the value of your TIPS bonds.

TIPS bonds and inflation protected bond funds are easy to buy. You can purchase TIPS and TIPS ETFS and mutual funds through your brokerage account. Or, buy individual TIPS bonds at Treasurydirect.gov here. Just realize that as inflation declines, so will the principal value of the TIPS bonds.

FAQ

TIPS bonds are a good investment during periods of high inflation and can help to preserve the value of your cash. TIPS inflation bonds can also help diversify your portfolio and cushion drawdowns.

Since TIPS are backed by the U.S. government, there is little chance of default risk. But, they do have the risk of declines in principal value, should deflation occur.

TIPS are different than typical bonds, as their principal value rises and falls along with changes in the CPI. Whereas, most corporate and fixed coupon rate bonds, will receive the par value at maturity. Bond funds don’t have a maturity date, and when you sell the value might be greater or lower than your purchase amount. TIPS are neither better nor worse than corporate or other treasury bonds. They each serve a different purpose in your investment portfolio.

Yes, when inflation declines, so will the principal value of the bond. Also, all bonds, including TIPS might lose value when interest rates increase.

Related

- I Bonds – Best Investment to Keep Pace With Inflation

- The Pros and Cons of Investing in Gold

- Best Low Risk Investments

- 10 Best Alternative Investments

- How To Benefit From Cyclical Investment Markets

- How To Get A Good Return On Your Cash

Disclosure: I own individual TIPS and the VTIP fund.

The statement is provided to you by Barbara Friedberg Personal Finance (“Promoter”) who has entered into a written referral agreement with Empower Advisory Group, LLC (“EAG”), through which Promoter will be paid for new leads through EAG. Promoter is not a client of EAG. Promoter is not affiliated with EAG or its affiliates and Promoter’s services consist solely of referrals of prospective clients.

No fees or other amounts will be charged to Personal Strategy clients, prospective clients, or any other clients of Promoter or EAG as a result of this arrangement. Investors should conduct their own research and seek advice before making investment decisions. For more information about EAG, refer to its Form ADV through the SEC’s website.