Groundfloor Investing – Invest in Real Estate Debt

Diversifying an investment portfolio is important in order to boost your investing returns. In addition to other forms of debt investing, real estate crowdfunding allows you to diversify and receive a passive income stream. This Groundfloor Investing Review provides all the information you’ll need to find out whether Groundfloor is right for you.

Groundfloor is qualified by the Securities and Exchange Commission (SEC) to offer real estate debt investments. Unlike most private real estate investments, Groundfloor serves accredited and non-accredited investors (i.e. everyone) via a mobile app and desktop browser.

The Groundfloor investing platform brings together borrowers seeking short-term real estate project financing and investors looking for cash flow through short-term real estate debt. This Groundfloor review explains how investors can be the bank, and loan money to real estate investors.

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

Currently, our Groundfloor investment review research reveals that the company has more than 260,000 registered users who have invested more than $1.6 billion since inception. Historical returns stand at 10% on average, with less than a 1% loss ratio since 2013. Over 5,800 loans successfully repaid to date. Although, it’s important to understand that your returns may vary from Groundfloor’s historical average.

Our comprehensive Groundfloor U.S. review provides the information you need to decide if Groundfloor investing is right for you.

What is Groundfloor?

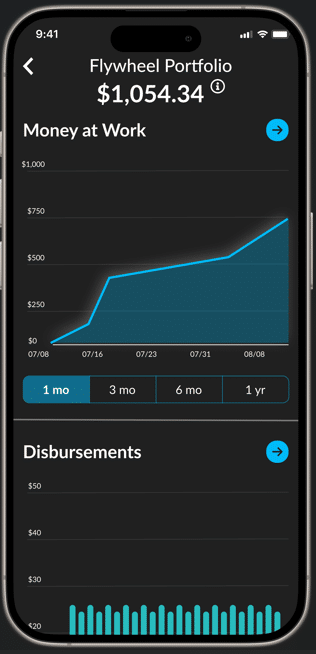

Groundfloor finance is an alternative investment platform and mobile app (available via Apple App and Google Play Store), making it easy for anyone to start fractionally investing into real estate loans. No prior real estate knowledge is required as Groundfloor allows everyone to transfer in funds and diversify automatically into hundreds of projects at once. Additionally, with the launch of the Flywheel Portfolio in October 2024, investors can enjoy weekly cash flow along with broad diversification, to minimize the risk of an unperforming loan.

What You are Investing in at Groundfloor?

The Groundfloor real estate platform lends to a variety of real estate investors. Most of these loans are issued to experienced developers who are flipping homes, building new construction homes or refinancing for long-term holds or rentals. Importantly for investors, Groundfloor usually holds a first-lien position on these loans and are backed by the underlying asset of the home itself. Should the borrower have difficulty repaying the loan, any payments go to those in a first-lien position, ahead of other creditors.

Groundfloor’s model opens private real estate lending to everyone, with a low, $100 minimum and a transparent real estate debt investment platform. Your investment is pooled with other investors money.

For borrowers, Groundfloor provides access to flexible, fast and cheap capital.

Pros and Cons of Groundfloor

Pros

- Weekly cash disbursements with the Flywheel Portfolio

- 10% average annualized returns since 2013

- Low $100+ initial investment for Flywheel Portfolio

- Open to accredited and non-accredited investors

- Highly diversified portfolio of real estate debt

- Low default rates (0.84% loss rate since 2013)

- Open to international investors, with a $5,000 minimum

Further, the platform ensures that its investors receive sufficient information about their investments’ health. That’s another unique feature of this lending and investing company.

Cons

- Less liquidity than public investment markets

- Loan defaults can cut into your returns

- The 0.5% to 1.0% management fee cuts into returns

- You lack protection or insurance against company (Groundfloor) default

- Groundfloor Notes require a $1,000 minimum investment

Groundfloor History

Groundfloor was the first company to achieve SEC qualification for real estate microlending and is able to provide investment offerings to all investors, both accredited and non-accredited (read: everyone) through Regulation A.

Groundfloor was founded by Nick Bhargava and Brian Dally in 2013 in Atlanta Georgia. Despite its U.S. headquarters, International investors are welcome at Groundfloor, with a $5,000 minimum. Providing invesors, from across the globe, an opportunity to fund and profit from U.S. real estate is a rare opportunity.

Who is Eligible for Groundfloor Investing?

All investors can invest in Groundfloor: accredited or non-accredited, US or non-US. Groundfloor is one investment platform available to all investors. As a result, the firm is among the most accessible alternative investment opportunities in the market worldwide.

The platform’s structure offers many benefits over other non-traditional investment sites. The most outstanding one is exposing small-scale investors to the real estate debt investment market. With a $100 minimum investment, you’re able to access Groundfloor’s Flywheel Portfolio of hundreds of short-term real estate loans with high-yield returns.

<<new image>>

How Does Groundfloor Work?

Groundfloor offers several types of high-yield investments, to suit various types of investors.

The transparent Groundfloor dashboard, available on desktop and mobile, shows investors the loan grade, expected return range, regular updates, and more for each investment.

Flywheel Portfolio

The Groundfloor set-it-and-forget-it Flywheel Portfolio, released in October 2024, is ideal for investors seeking weekly cash flow. Create an account, connect your bank account and transfer at least $100. Funds are invested across a collection of 200–400 short-term, high-yield loans for immediate diversification.

Groundfloor originates and pre-funds the Flywheel loans The loans are SEC qualified and available to both accredited and non-accredited investors.. The Flywheel Portfolio has delivered historical 10% average annualized returns and broad diversification within one fund.

Groundfloor Flywheel Portfolio Fees

Investors pay no fees upfront for the Flywheel, but there is a 0.50% to 1% management fee assessed when the funds are disbursed back to investors, along with their share of the interest. The 10% average returns are calculated after all fees have been paid.

Groundfloor Real Estate Notes

For those seeking greater liquidity and lower risk, Groundfloor Notes (or short-term loans) are available in Standard or Rollover options. Interest rates will vary, based upon market rates. If you need the cash immediately, you can cancel the note and receive your initial investment back, within the first 30-days. These Groundfloor Notes require a $1,000 minimum.

Two Types of Groundfloor Real Estate Notes

- Standard Notes come in 30-day, 90-day and 12-month terms with current yields ranging from 5.0% to 7.50%. Yields will vary, based upon current market interest rates. Your money is available for withdrawal upon notes maturity after 30 days, 60 days, or 12 months.

- The principal amount of the Rollover Notes are similar to the Auto Investor account and upon maturity, notes automatically roll over and invest in a new Rollover Note of the same term. The rollover notes are available for 30- and 90-day terms.

Groundfloor Notes release at the beginning of each month are a relatively liquid alternative for your short term cash needs.

Groundfloor Liquidity

Unlike money invested in liquid public markets, investors should only invest money in Groundfloor that they can leave invested for longer periods of time.

You can’t withdraw funds from the Flywheel Portfolio while it is lent to borrowers. After loans are repaid, the money will transfer to your “available balance,” where you can withdraw the funds or reinvest in additional loans. The Flywheel portfolio loan maturities range from 6 to 18 months, which means that every loan will mature within a specific time period. Despite the lock up period while the loans are in progress, you will receive steady weekly repayments because of the high diversification.

All Groundfloor notes can be redeemed within the first 30-days, but if redeemed, you will forfeit interest payments. After the first 30-days, Standard Notes will mature and the principal returned within the 30-day, 90-day and 12-month terms.

Groundfloor Mobile App and Auto Investor Feature

Groundfloor’s mobile app is available in the Apple App and the Google Play Stores. The auto investment feature in the Flywheel Portfolio instantly reinvests funds as soon as repayments come in for compounding returns. This gives Groundfloor investors a true, set-it-and-forget-it experience. As soon as funds hit the platform, your funds are automatically diversified into the Flywheel, offering greater diversification while mitigating risk. Better yet, investors can start seeing repayments in as little as seven days.

If desired, you can turn off the auto invest feature. This enables you to withdraw money from your “available balance” after the loan is repaid.

Groundfloor Fees

The company makes money from borrowers and charges 2.75% to 4.00% of the principal loan amount and $495 application fees for borrowers.

Flywheel investors are levied a 0.5% to 1.0% fee upon disbursement of their principal and interest payments. As previously stated, the historical 10% annual returns are after fees.

How to Make Money on Groundfloor?

If the project runs smoothly, an investor usually receives a proportionate interest payment and a lump sum payment of the principal at the end of the investment period. Because you are invested into 100’s of these projects in the Flywheel Portfolio, you start seeing reimbursements trickle in weekly.

Groundfloor Notes investment principal plus interest payments are returned when the notes mature after 30- or 90-days, or 12-months.

Groundfloor Risk – Loan Defaults

If a borrower defaults on the loan payment, the Groundfloor management team begins negotiations with the borrower. If negotiations are unsuccessful, the team manages the foreclosure process, which can be costly and time-consuming. Fortunately, Groundfloor has an average 6% return rate on defaulted loans, so you may still earn a profit on these loans. Groundfloor is in a first-lien position to mitigate risk for investors, only using foreclosure as a last resort solution. This means that Groundfloor investors get repaid ahead of other creditors.

After the foreclosure, Groundfloor management oversees the property’s rehabilitation and selling. If the rehab and sale are successful, you get back all or part of your principal plus interest. In some cases, you might receive a bonus from penalty fees.

On the other hand, if the proceeds from the defaulted borrower are insufficient, you might realize a loss on your investment. In the case of default, you won’t receive interest or principal payments during the negotiation and foreclosure periods.

Investors should realize that occasional losses are a characteristic of any type of financial investment.

FAQ

Yes, Groundfloor is legit. If you’re seeking to diversify your investments beyond stocks and bonds, into private real estate loans, then Groundfloor has proven itself as a sound and transparent company. As long as you understand that there are potential risks of the occasional loan default, and that your money will be tied up for the term of the loans, then you might be a good candidate to invest in Groundfloor. Higher returns come with a degree of risk, regardless of the investment firm.

Investing in Groundfloor is different from other investments in two ways: relatively short holding periods and continuous investor updates on the status of your investments. Groundfloor investing is also distinct from other platforms with offers for non-accredited and accredited investors.

Groundfloor has shorter investment terms than many other private crowdfunding investment platforms. Notes can be redeemed within 30 days and in 30-day, 90-day and one-year terms. The Flywheel Portfolio loans mature and can be redeemed from 6 to 18 months. Many comparable private real estate lending platforms have longer lock up periods.

To start investing in Groundfloor create an account, link the account to a bank and transfer funds. This should take 3 to 5 business days. With the Flywheel Portfolio, your funds are immediately invested in real estate loans.

How to Earn at Groundfloor?

There are two ways in which you receive your payment with Groundfloor investing. You receive weekly interest payments and the principal is returned at the end of the investment duration. Your Auto Investor Account automatically reinvests your funds based on your settings. If you prefer to withdraw the money, turn off auto invest and you can transfer funds, listed within your “available balance” out of the platform.

Returns are not guaranteed. You can expect 8.0% through 15.0% returns from your Groundfloor investing. Groundfloor has an average annualized return rate of 10%. The platform provides access to short-term, high-yield investments to borrowers with various creditworthiness. The riskier loans offer higher returns, but also have greater default risk.

The greatest risk of investing in Groundfloor is default by the borrowers. That occurs when the property improvement becomes more costly or complicated than expected, causing a delay or termination of the project.

When the borrower fails to repay the loan the company’s asset management team sells the underlying real estate to recover as much money as possible. You will receive your proportion of interest and principal payments, whenever they occur.

Groundfloor can be a good investment. Its debt-based structure and automatic loan diversification offers a reliable source of investment income. Also, the platform’s short-term emphasis means your funds won’t be locked up for long.

You can contact Groundfloor 9:00 am to 5:00 pm EST Monday through Friday through [email protected] or by setting up a time to chat with a Customer Support Specialist one-on-one, on the website.

Which Are the Best Groundfloor Alternatives?

Below are 3 top competitors of Groundfloor:

Groundfloor Vs. Fundrise

The main difference between Groundfloor and Fundrise is their specialization and minimums. Although Fundrise also has offers for both accredited investors and non-accredited investors, the Fundrise minimum investment amounts range from $10 up to $1,000 for an IRA.

Groundfloor offers investors a variety of types of real estate debt in which to invest.

Fundrise is akin to a private investment marketplace, with various types of offers, including private debt and venture capital offers.

Also, Groundfloor offers investors weekly income payments on their investment, while Fundrise inventors receive quarterly dividend payments. Fundrise investors might also receive capital appreciation.

Unlike Groundfloor, which has minimal investor fees, Fundrise charges its investors management fees per offer. Their fees range from 0.15% up to 1.85%% or more. All fees are listed on the platform and can be viewed before investing.

Groundfloor Vs. PeerStreet

PeerStreet filed for bankruptcy in June, 2023 and we don’t recommend investing with them.

Groundfloor Vs. CrowdStreet

There are many differences between Groundfloor and CrowdStreet including the minimum investment requirements, accreditation status, and types of investments. Groundfloor has a minimum of $100, while the Crowdstreet’s minimum is $25,000 for most deals. Both platforms served accredited investors, yet only Groundfloor provides non-accredited debt offers. CrowdStreet offers more investment options than Groundfloor including both debt and equity real estate.

Also, while Groundfloor specializes in short-term real estate loans, CrowdStreet focuses on commercial real estate deals and funds. CrowdStreet caters to wealthier investors with greater assets.

Is Groundfloor Investing for You? Wrap up

If you’re looking to diversify your investment assets beyond the public markets into private real estate debt, with higher returns, then Groundfloor real estate investing might be for you. The platform offers high yield loans to short term real estate borrowers. Investors can purchase a fractional portion of these loans through the Flywheel Portfolio. Those seekilng an outlet for their short term cash, might consider the Groundfloor Notes.

While historical returns have delivered roughly 10% annually, there are no guarantees for future returns. You’ll also need to accept that your Groundfloor investments are not as readily available or as liquid as those in the public investment markets.

Groundfloor might be a good investment for a portion of your assets if you can keep the money tied up for a few months to a few years. However, the high-yield nature of the investment returns comes with risk. Groundfloor investments are ideal if you don’t need immediate liquidity and if you’re willing to accept greater risk, to achieve higher returns. Study this Groundfloor Review and check out the website and mobile app to learn more.

Related

- Is Now A Good Time To Borrow Money?

- How Can Investors Receive Compounding Returns?

- Real Estate Crowdfunding – Diversify Your Portfolio

- PeerStreet vs Groundfloor

- 15 Accredited Investor Opportunities

- Fundrise vs Diversyfund vs Groundfloor

- A Penny Doubled Every Day For 30 Days Or $1 Million – Which Would You Choose?

- How Much Cash Should I Have On Hand?

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.