You Can Beat Inflation with I Bonds

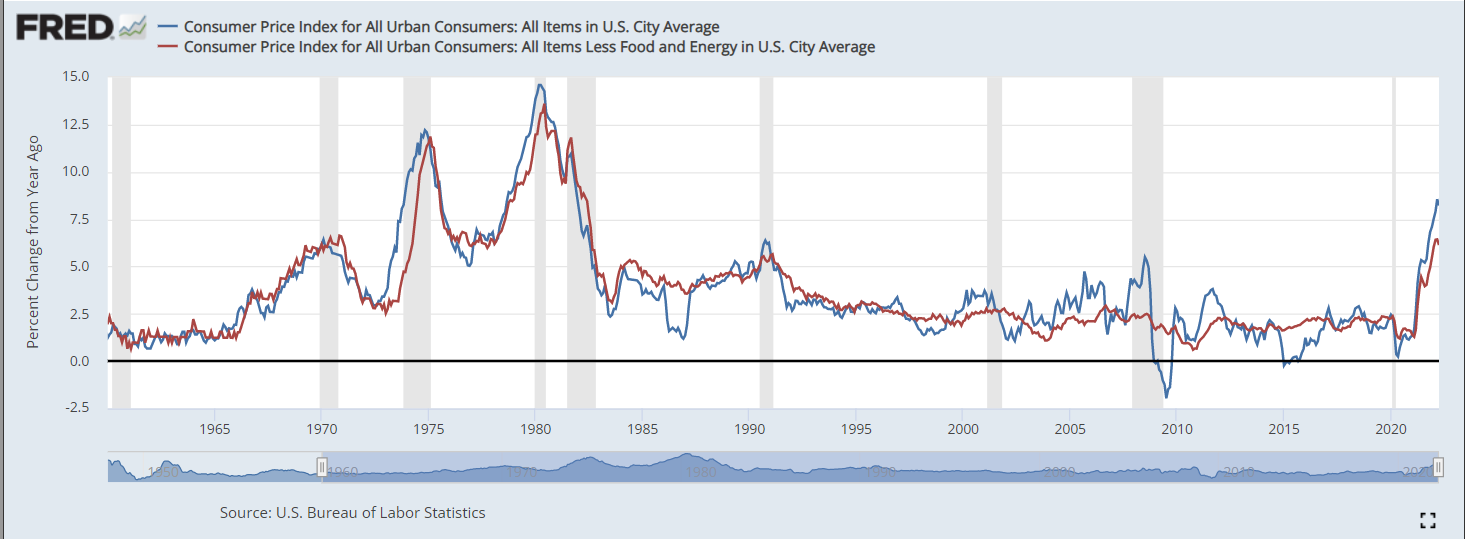

For the first time in decades, inflation is inching towards double digits. During April 2022, the 12 month inflation rate topped 8%. The inflation rate hasn’t been this high since 1982, as measured by the Consumer Price Index, or CPI. This means that you’ll need to earn 8% more this year to pay for the goods and services that you purchased last year.

U. S. government savings bonds can help protect your money from the ravages of inflation. The two best government bonds, with inflation protection are TIPS or Treasury Inflation Protected Bonds and Series I Savings Bonds.

This article will explain I bonds including where to buy, how interest payments are calculated, and the pros and cons.

CPI Inflation Rate: February 1960 – March 2022

Source: https://fred.stlouisfed.org/graph/?g=rocU

How do I Bonds Work?

If you’re wondering “What are I Bonds?” Here is a brief I bonds explainer.

I bonds are an investment, which is guaranteed by the U.S. government to protect your purchasing power from inflation. There is no commission fee to purchase this investment and the interest rate corresponds with the inflation rate. Although you’ll pay federal income taxes on the bond interest, the I bonds are free from state and local taxes.

For as little as $25 you get an investment which protects cash and purchasing power from inflation. At treasurydirect.gov, you can buy I bonds in any amount from $25 up to $10,000. Every six months, the I bonds interest rate is adjusted for inflation. If inflation is 3 percent, then the I bond interest payment will adjust, twice per year, to an annualized return equivalent to 3 percent.

Watch my interview on Cheddar Closing Bell about The Benefits of iBonds.

I Bonds interest is calculated with an initial fixed interest rate, that remains the same for the life of the bond and an inflation rate that is set twice a year on on the first business day in November and May.

In November, 2022 the I bond fixed interest rate through April 30, 2023 is 6.89%. If you buy a new I bond today the fixed interest rate is 6.89%

How Many I Bonds Can I Buy Annually?

You’re only allowed to purchase a total of $15,000 worth of I bonds annually. This is sufficient for small investors, but wealthier individuals, may find this a major constraint.

You can buy a maximum of $10,000 per person annually, online in denominations of $25 to $10,000. You’re also able to buy up to $5,000 paper I bonds, with your tax refund each year.

If you and your spouse each buy $10,000 worth of I bonds and $5,000 with your tax refund, that’s $25,000 per year. Do that every year for five years and you’ve got a $125,000 cache of inflation protected bonds.

If you’re seeking more inflation protected bonds, check out U.S. government TIPS bonds, available to buy at treasurydirect.gov or a TIPS bond fund.

How Long Must I own my I Bonds?

The bonds earn interest for up to 30 years. You must own them for at least one year before redeeming them. Although, if you cash your I bonds within one to five years, you’ll lose the previous three months of interest.

You can sell your electronic I bonds online at Treasurydirect.gov and have the proceeds electronically transferred to your bank account. Paper I bonds can be redeemed at most financial institutions or mailed in to the Treasury Retail Securities Services along with FS Form 1522.

How is Interest on I Bonds Calculated?

The interest rate on I bonds is a composite or combined rate of a:

- Fixed rate

- Inflation rate

The fixed rate never changes and remains the same for as long as you own the bond. The rate is announced twice each year, on the first business day in November and May, and applies to all I bonds issued during the next six months.

The inflation rate typically changes every six months and is set on the same day as the fixed rate. This interest rate for series I Savings bonds is based on changes in the non-seasonally adjusted Consumer Price Index for urban consumers or CPI-U, which includes food and energy.

The current inflation rate for your bond is applied every six months, from the bond’s issue date.

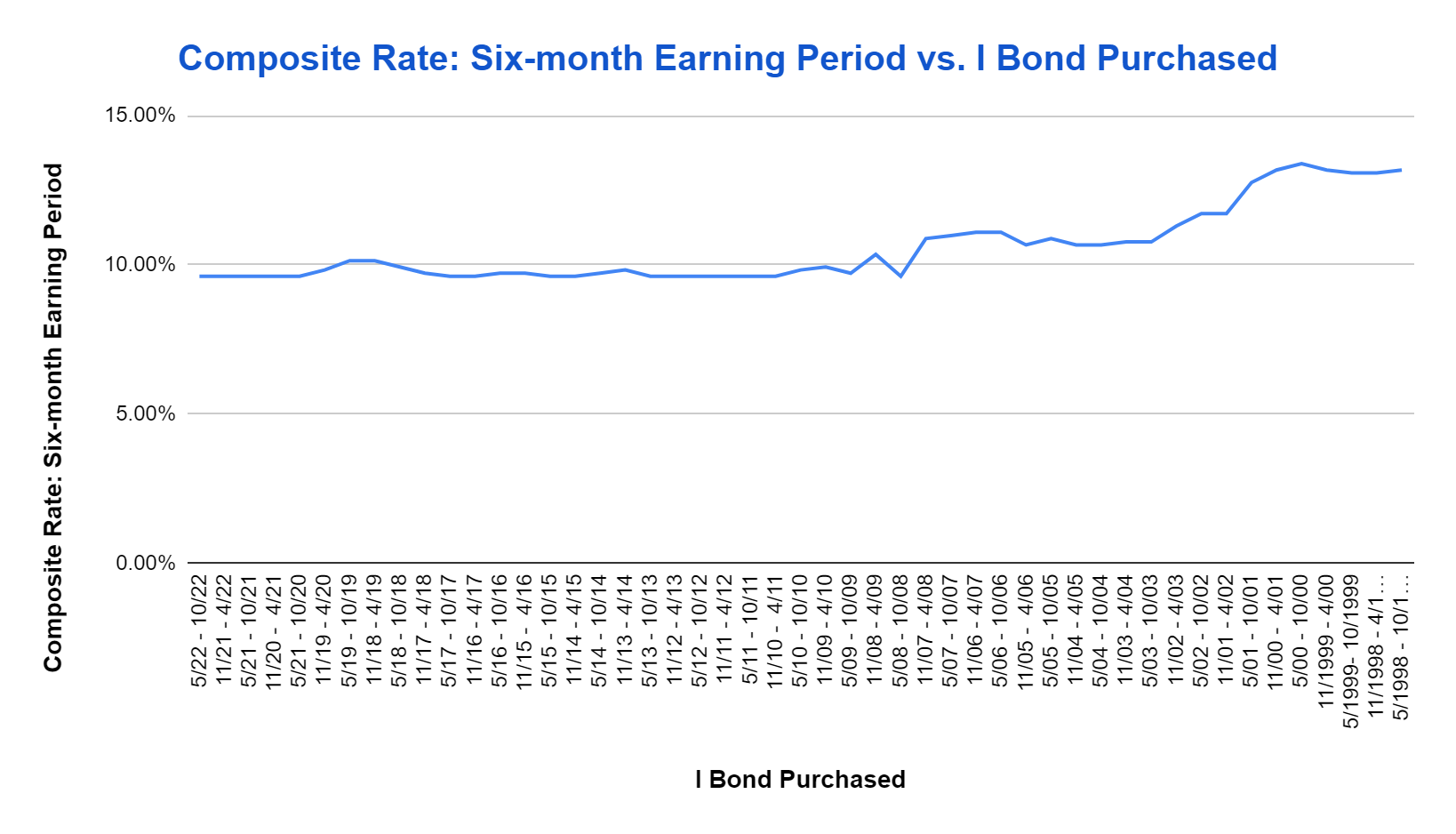

Current Composite Interest Rate for Every I Bond Issued (as of April 2022)

Composite Interest Rate for I Bonds Issued from 1998 – 2022 (April)

Composite Interest Rate

The fixed and composite interest rates are combined to determine the interest rate that your bonds earn. The combined rate is never less than zero, but the combined rate can be lower than the fixed rate. If the inflation rate is negative, or deflationary, some of the fixed rate will be reduced.

The composite rate is calculated using the following formula:

Composite rate = [fixed rate + (2 x semiannual inflation rate) + (fixed rate x semiannual inflation rate)]

Since May 2008, the fixed interest rate for I bonds has hovered around 0.00%, due to historically low inflation rates. But, with the recent ramp up in inflation, the composite rate of current returns for all I bonds soared to between 9.6% and 13.39% for I bonds purchased between May and October, 2000.

When is Interest Paid on I Bonds?

I bonds earn interest monthly from the first day of the month and accrues until you cash in the bond, or it is 30 years old, whichever comes first. The interest is compounded semiannually and added to the bond’s principal value. Future interest payments are calculated on the new principal value.

How are I Bonds Taxed?

I savings bonds interest is subject to Federal, but not state or local income tax. Although if you use the I bonds to pay for higher education, you might avoid paying taxes on the interest payments. You can read about the caveats for the higher education tax exemption on the treasury direct website.

You can report the interest annually, as it’s earned or you can wait until you cash the bond, or it stops earning interest to pay the tax due.

How to Invest in I Bonds?

The federal government website treasurydirect.gov is the headquarters for all government securities including TIPS, treasury bonds, bills and notes. It’s easy to set up an account and purchase I bonds. The website is user friendly and easy to navigate with headings for all types of government bonds easily accessible from the home page.

You can even invest in I bonds with a trust account!

With inflation becoming a bigger burden today, it is an ideal time to begin purchasing I bonds. Because there are no incentives for your financial advisor, or commissions, you’ll have to buy them on your own.

What are the Pros and Cons of I Bonds?

Pros

- Along with TIPs, I bonds are among the best investments to protect the purchasing power of your cash from rising inflation.

- I bonds are safe from credit risk and protected by the faith and credit of the U.S. government.

- I bond interest is free of state and local taxes.

- Interest received on I bonds used for higher education might avoid federal income taxes.

Cons

- You’re only eligible to buy a maximum of $15,000 per year per Social Security number – $10,000 electronic and $5,000 paper bonds with your tax refund.

- When inflation subsides, so will the interest earned on your I bonds.

- I bonds are illiquid for one year after purchase and will lose 3 months interest payments if redeemed within five years.

FAQ

I bonds are a different type of investment from stocks. They are cash-equivalent or fixed income investments and much safer than stock market investments. Stocks represent ownership in companies and their returns are typically more volatile. Over long periods of time, when inflation is tame, you’re likely to receive higher returns from stocks than from I bonds, albeit with greater price volatility or risk.

Yes and no. When inflation rates decline, your I bond interest payments can decrease. Yet, the principal value of your I bond will not fall below the purchase price.

You can’t cash in an I bond for one year after purchase. If you redeem the I bond between one and five years, you’ll forfeit three months of interest. You can’t purchase more than $15, 000 I bonds per year, $10,000 electronically and $5,000 with the proceeds of your federal income tax refund.

The I Bonds increase in value on the first day of each month as they earn interest and increase in value.

The interest is compounded twice per year

Are I Bonds a Good Investment? Wrap up

If you bought an item for a dollar in 2017, in 2022, that same item might cost $1.18, given the 17.9% inflation we’ve experienced in the past five years, according to usinflationcalculator.com. If you’re in or nearing retirement you might add I bonds to your investment portfolio to protect the purchasing power of your cash. If you’re saving for a home down payment or a goal a few years away, you might buy I bonds as well.

The drawback to these savings vehicles is that you’re limited to purchasing $10,000 I bonds annually per social security number and $5,000 of your tax refund in paper I bonds which brings your total annual investment up to $15,000. Although, for most investors, this limitation isn’t much of a problem.

I bonds are a sound investment for the cash portion of your investment portfolio. They are easy to buy, tax-advantaged and certain to keep up with the pace of inflation. For those who want to avoid investment volatility and want their cash to hold it’s value, I bonds are an ideal investment. The returns are tough to beat in this low interest rate environment.

Related

- Are Bonds A Good Investment Now?

- How To Get A Good Return On You Cash Without Too Much Risk

- 5 Low Risk Investments For A Rising Interest Rate Environment

- Would You Invest In A Muni Bond Portfolio?

- Best Cash and Related Investments For A High Interest Rate Environment

- M1 vs Wealthfront: Which Is Best?