I began planning for retirement at age 25, and my husband and I hit our retirement number several years ago. Even when we weren’t making a lot of money, the tactics I learned in my 20’s and 30’s began a lifelong path of saving and investing, which ultimately increased our family’s financial security.

Retirement Planning in Your 30’s

The earlier you start planning for retirement, the easier it is to save what you need.

If you’re in your 30s, retirement may seem a long way off. But did you know that’s actually a good thing? More than anything, having time on your side can make or break even the best-laid retirement plans. In fact, learning how to save for retirement in your 30’s will save you a lot of money.

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

The reason for this is that compound interest plus investing is an amazing way to turn small amounts of money into a six or seven figure retirement stash.

Should a 30 Year Old Think About Retirement? Yes. Here’s how to do it, and it’s easier than you think.

Why Save for Retirement in Your 30’s?

source: https://www.stlouisfed.org/open-vault/2018/september/how-compound-interest-works

Compound interest or returns makes saving for your ideal retirement easier. The way compound interest works is simple: it pays out interest not only on your original investment, but also on the interest and capital growth that has collected over the years.

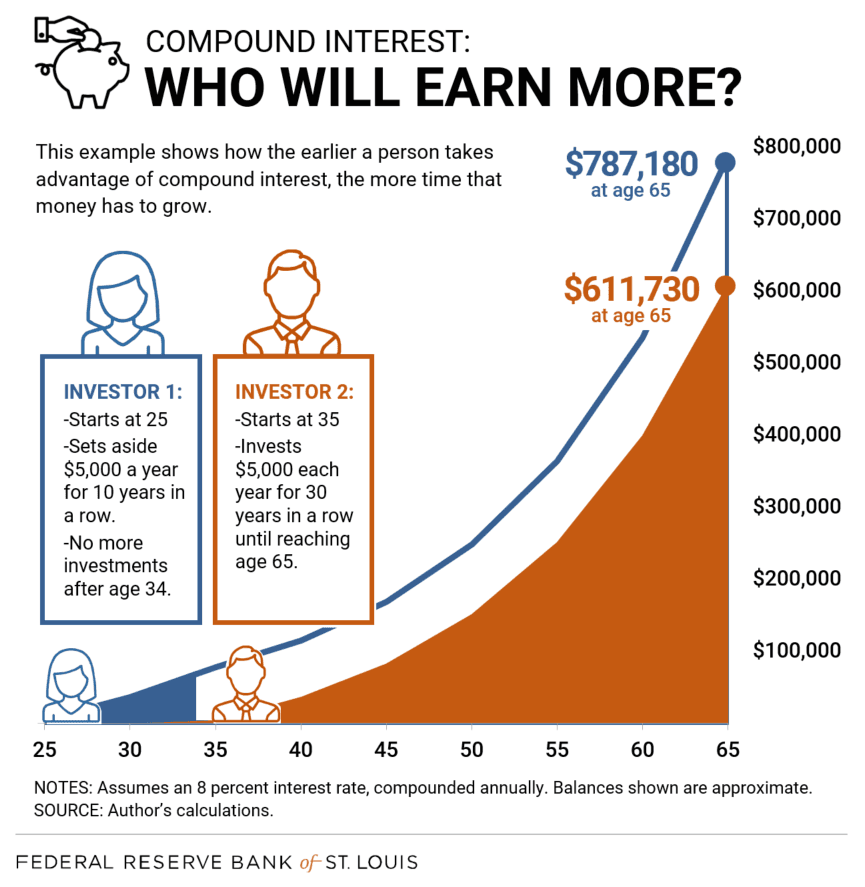

In the chart above, Investor #1 begins saving for retirement at age 25. She invests $5,000 per year for 10 years and earns an average 8% return. In sum, she’s invested a total of $5,000 x 10 years or $50,000. After 10 years, she stops her investing. At age 65. she has $787,180 in her account.

Investor #2 waits until age 35 to begin investing. He contributes $5,000 per year for the next 30 years and also earns an average 8% per year. He invested $150,000 by the time he reaches age 65. At age 65, Investor #2’s account is worth $611,730. He contributed $100,000 less than Investor #1 and yet has more than $150,000 less at age 65 than Investor #2.

And that is the power of time, investing and compound returns.

The longer your money can grow and make money, on top of your original investment, the more money you will have. So, should a 30 year old find out how to plan for retirement, absolutely!

Investors #1 and #2 kept their monthly investment contributions the same each month. Imagine, how much more money you’ll have in retirement if you increase the amount you invest, as your income rises.

Next, get an idea of how much money you’ll need in retirement.

But How Much Retirement Money Will a 30 Year Old Need in Retirement?

While some experts believe that you should plan to spend roughly 85% of your pre-retirement income during your retirement years, in reality you may need much less than that. Consider the difference between you-at-30 and you-at-65: 30 year old you may have lingering student loan debt, might have recently purchased, or considered purchasing, a home, and could even be considering starting a family. The expenses we face at 30 will likely not be present at 65.

To envision your ideal retirement savings, ask yourself what debts or expenses may be still lingering in your 60s, and which may be gone. Realistically, you may still have your 30-year mortgage. But will you still have $500 each month in student loan debt? You may also consider lifestyle changes. If you have a family now, will you still need or want that 4-bedroom home with the large yard, or would a smaller location do?

Add in some extra money for travel – if that’s your thing. Then factor in money for increased health care spending. Fortunately, for you, there are quite a few excellent retirement calculators to help you with this step. I use the Personal Capital retirement calculator and also appreciate the platform’s other money and investment management features.

Quick Method to Calculate Your Retirement Spending Goal

Here’s a quick way to guesstimate your retirement spending goal. Keeping these potential changes in mind, create your target yearly spending in retirement and then multiply by 25. This is your retirement savings goal. Don’t forget that you’ll be receiving money from Social Security, so you won’t need your retirement savings to fund all of your spending.

Is that goal a bit overwhelming? Don’t worry yet! Remember: time is on your side. Let’s consider a few scenarios and see how time, combined with compound interest, can make a difference in your retirement savings.

Still wondering…’Should a 30 Year Old Think About Retirement?’ Keep reading to find out how much easier it is to start saving for retirement sooner rather than later.

Click below for one of the best retirement planners. Quick set up and great reports and projections:

Benjamin: Planning for $80,000 Yearly in Retirement

Benjamin, who is 30, would like to spend $80,000 each year in retirement. Benjamin wants to be sure he continues to enjoy life after he stops working, and has plans to travel. However, in order to have $80,000 to spend each year after he turns 65, Benjamin will need $2,000,000 at age 65, without considering Social Security income. With Social Security benefits, he’ll need to save less.

But, just for fun, let’s take a look and see how 30 year old Benjamin could save up to $2,000,000 for retirement.

At age 30, Benjamin has not started saving for retirement. However, his expenses are low and he has a lot of disposable income. In order to reach his goal of two million dollars by age 65, Benjamin will need to save $1,000 each month in Mutual Funds or Exchange Traded funds that average out to 8% annual returns. This is possible with a well diversified investment portfolio.

Things move very quickly for Benjamin: in his first year, he receives $532.93 in returns on his first $12,000 in contributions. That $532 is comprised of dividends and capital gains received on his initial $12,000 investing

By year 5, Benjamin is making $5,241.12 in interest. Year 14 brings a stunning interest payment of $23,336.30, which is almost double Benjamin’s yearly contributions.

If Benjamin continues contributing $1,000 each month and maintains his 8% return, by age 65 he will have $2,309,175.03 saved for retirement. The best part? Benjamin contributed only $420,000 of that amount. The remaining $1,889,175.03 came to him in the form of compound returns on his investments.

We’ve covered the why, the how much you’ll need, now let’s delve into the how to save for retirement in your 30’s.

Retirement Planning in Your 30’s – 5 Steps

- Max out 401k contributions

- Contribute to a brokerage account

- Eliminate debt

- Create a side hustle

- Spend less than you earn-always

1. Max out 401k Contributions

Most companies offer a match, up to a certain point, of your contributions into your workplace retirement account. That means if you contribute 10% of your income into the plan, your company might add another 5% into the plan. So, if you make $70,000 per year, you’ll contribute $7,000 each year and your employer will add in $3,500 for a total of $10,500.

Invest the money wisely, in an aggressive asset allocation, and instead of having a six figure retirement account, the value will easily top seven figures!

The way to make sure that you maximize your returns on your retirement contributions are to choose low fee investments, like index funds or a target date fund. Pay attention to the funds expenses, because the more you save on expenses, the more of your money goes directly into the actual fund.

Investing more money in stock market index funds when you’re younger will likely lead to higher long term returns. And even though stock funds tend to decline in value on occasion, the decades in front of you before retirement will likely offest any short-term losses and provide higher long term returns

2. Contribute to a Brokerage Account

Thought you were done with saving for the future? Not yet. Even if you can’t add much additional cash for investing, it’s wise to avoid relying on your 401k for all of your retirement and future saving needs. That’s because if you need the money before you turn age 59 1/2 in most cases, you’ll face stiff withdrawal penalties.

You might want to save up for other goals, like a new home or college or a new car. Investing in the investment markets continues to be a superior strategy for building long term wealth. Just make sure not to deploy any cash into the investment markets that you’ll need in less than five years.

Stock market returns are volatile, so keep money for shorter term goals in cash or certificates of deposit.

There are scores of choices for investing, outside of your 401k. I personally have accounts at several of the large brokerage firms like Vanguard and Fidelity.

I also like robo-advisors for streamlining investing with small amounts of money. In fact, I have accounts at M1 Finance and Schwab Intelligent Advisors robo-advisors as well.

The benefit of investing with a robo-advisor is that you can have a specific amount transferred from your paycheck or bank account directly into the robo-advisor, and they will manage the money in accord with your preferences for zero or low fees.

3. Eliminate Debt

You might wonder why eliminating debt is included in saving for retirement in your 30’s. The reason is because if you have a lot of high inerest rate debt, no matter how much you save for retirement, you’ll be handcuffed by the debt payments. Look at it this way, You have $10,000 of credit card debt and your interest rate on that debt is 20% per year. In addition to the $10,000, you’ll pay an additional $2,000 in interest.

If you simultaneously contribute $10,000 to your retirement account and earn and 8% rate of return on that money, you’ll have gained $800. Compare the gain of $800 from your retirement account investment, with the loss of $2,000 from your credit card interest, and you’re in the hold for $1,200.

Unless the interest rate on your debt is extremely low, like below 3% to 4%, you’re usually best off getting eliminateing the high interest rate debt as quickly as possible.

Mortgage debt and low interest rate student loan debt are less troublesome than higher interest rate credit card debt. So focus on slashing any credit card debt as quickly as possible, to improve your retirement saving and investing.

4. Create a Side Hustle

Most of our lives, my husband and I have worked more than one job. From consulting, to creating a side business, the extra money served two benefits. First, obviously is the extra money. Second are the tax benefits. Having your own business offers many deductions which can ultmately reduce your tax bill. Combining a business and pleasure trip enables you to deduct part of your travel expenses. Home offices offer offsets to the mortgage payment. Just make sure to keep good records – just in case.

With the side hustle income, you can simply direct it to your brokerage account, emergency savings fund, or a Roth IRA, if you’re eligible. Although we’ve seen examples of the power of compounding with a fixed dollar amount, add additional money to your 401k, Roth IRA, or brokerage account and your long term returns will multiply.

If you’re not sure where to start, check out UpWork for ideas or start with some of the creative ideas to make more money.

5. Spend Less Than You Earn – No Exceptions

This is harder than it sounds. Advertisers, friends, and social media constantly bombard you with messages about buying more stuff. And if you don’t have the money, your credit card is in your pocket for spending. But, if you make the choices to spend a bit too much now, you’ll cost yourself financial discomfort tomorrow.

With compounding, spend just $1,000 less this year, invest that money instead and in 30 years that $1,000 will be worth more than $10,000.

Think of it this way, every dollar you spend today, actually costis you $10 of future wealth. So before you spend on something you don’t really want or need, consider whether you’d pay $100 for a $10 purchase.

(Assumes 8% average annual return with investments in diversified portfolio.)

Like any habit, spending less than you earn takes practice to develop. Use a a money app like Mint, Quicken, or Personal Capital to track your spending and investing, and it becomes easier to live wisely.

A trick you can use, when making the commitment to start saving for retirement in your 30’s is to ask yourself,, “Iis this purchase worth givng up the chance for financial independence tomorrow?”

FAQ

First, automate saving into your 401k, Roth IRA and/or investment brokerage account. Invest as much as you can, try for 10 to 15% of your income. Choose a moderately aggressive asset allocation with greater percentages allocated to stocks investments. When your salary increases, up your retirement savings. Consider using a robo-advisor.

No! The best time to save for retirement is NOW. Whether you are 30 or 50, saving for retirement should be your biggest investing and financial planning goal.

According to Fidelity’s Retirement Savings Guidelines, a 30 year old should have one years salary saved in a retirement account. So ir you make $50,000, then you should have that amount saved. If you make $150,000, then you should have that amount in your retirement account

Related

- How To Invest $500k

- What Is True Wealth? You Are Wealthier Than You Think

- Should I Buy A Bitcoin ETF?

- How To Earn Weekly Dividends With SOFI WKLY ETF

- Best M1 Finance Pies For Lazy Investors

Resource: Compound interest calculator.

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.

The statement is provided to you by Barbara Friedberg Personal Finance (“Promoter”) who has entered into a written referral agreement with Empower Advisory Group, LLC (“EAG”), through which Promoter will be paid for new leads through EAG. Promoter is not a client of EAG. Promoter is not affiliated with EAG or its affiliates and Promoter’s services consist solely of referrals of prospective clients.

No fees or other amounts will be charged to Personal Strategy clients, prospective clients, or any other clients of Promoter or EAG as a result of this arrangement. Investors should conduct their own research and seek advice before making investment decisions. For more information about EAG, refer to its Form ADV through the SEC’s website.