The goal of Fidelity’s retirement savings guidelines is to use a portion of your earnings today and make them last, so that you’ll achieve your desired retirement lifestyle. Your preretirement annual income must cover current expenses and future financial goals, such as vacations and college tuition along with income replacement in retirement. Fidelity’s retirement savings by age gives you a benchmark to strive for. We’ll also provide tips to meet your retirement savings goals.

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

U.S. Income Replacement Rate Estimate

Bankrate stated in August 2023 that the average Social Security benefit was $1705.79 per month or $20,469.48 per year. Fidelity reports retirees can expect to spend 55% to 80% of their preretirement income. So, with a 55% pre-retirement income amount, the average $20,469.48 per year Social Security benefit, funds the lifestyle of someone who earned $37,216 before retirement.

That’s great, if you were earning $37,216 before retiring, and your $20,469.48 retirement benefit covers all of your post retirement expenses.

The average per person annual income in the U.S. was $65,423, according to 2022 Statistica data. That’s a far cry from the $37,216 pre-retirement income that the average Social Security check might support.

Using Fidelity’s 55% pre retirement funding expectation, if you earned $65,423 before retiring then you’ll need at least $35,978 annually in retirement. That’s roughly $15,000 more than $20,469.48 Social Security Benefit.

The data suggests that you might need a retirement savings or investment account, to increase your income in retirement. That’s where the Fidelity Retirement Savings by Age guidelines can help.

Fidelity Retirement Saving Rate Guidelines Are Aggressive – So Start Saving Now

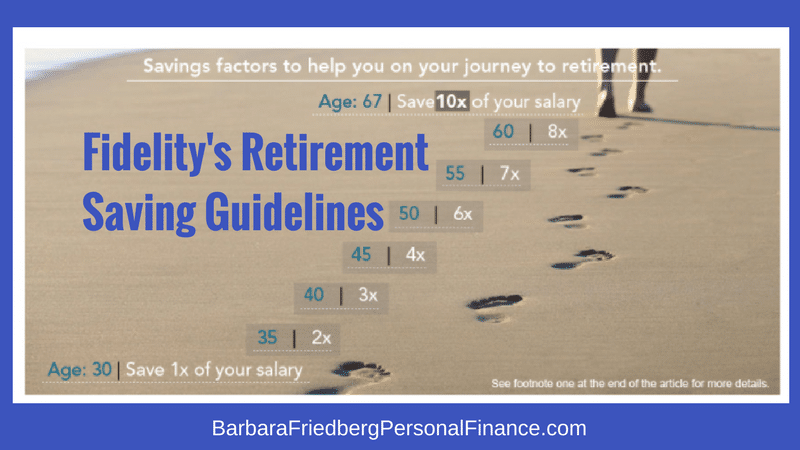

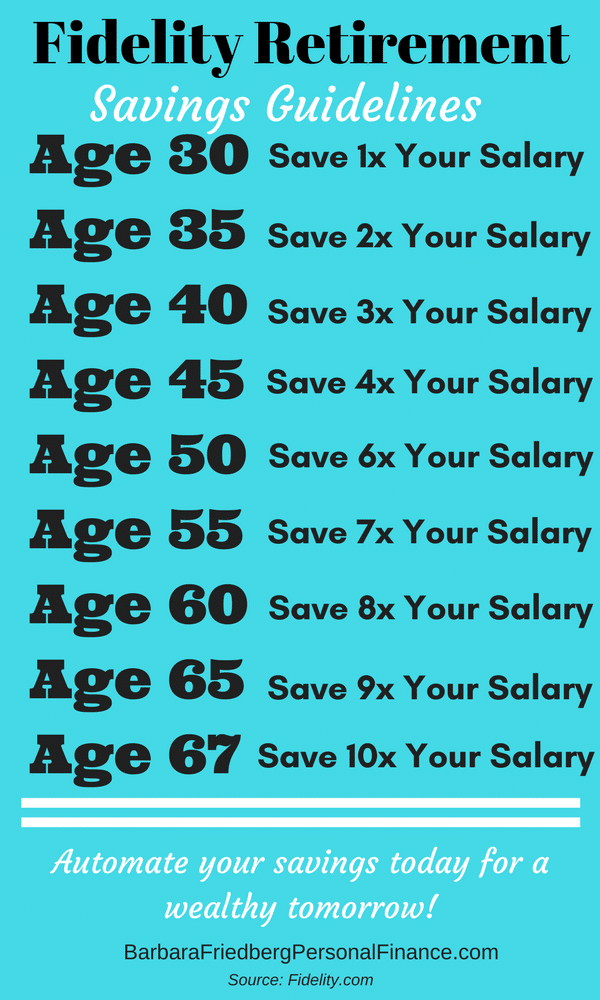

“Savings factor: Aim to save at least 1x your income at age 30, 3x at 40, 6x by 50, 8x by 60 and 10x at 67.” ~”How Much Do I Need to Retire” at Fidelity.com

Several years ago, Fidelity made a splash with cold hard retirement savings numbers. The discount brokerage powerhouse told savers and investors exactly how much they needed to save for retirement at each age milestone to fund a comfortable lifestyle in the future. Remember, this isn’t your emergency fund or the kid’s college fund!

- By age 30, you need the the equivalent of one year’s salary saved. So if you make $70,000 per year, you should have $70,000 saved for retirement at age 30.

- By age 40, you need three years salary saved for retirement. So, if your salary goes up to $100,000 by age 40, you need $300,000 saved for retirement.

- By age 50, you need six times your annual salary saved.

- By age 67, your retirement nest age should equal 10 times your annual income. So if you’re earning $185,000 per year at at 67, then you need $1,850,000 saved for retirement (according to Fidelity).

Obviously, these are guidelines, not mandates. Your lifestyle and financial goals are personal. But, it’s helpful to have a guide to work from. There are also many great retirement calculators, that can help with retirement readiness. One of our favorite Retirement calculators uses linked or manually input data from your financial accounts to create a probability estimate for meeting your future goals.

How to Meet Your Retirement Savings Goals – Start Now

Fidelity’s savings factors are created based on assumptions:

- Start saving 15% of your income annually (including employer match) starting at age 25.

- Invest 50% or more of your savings in stocks. If history is any guide, investing greater percentages in stock investments might yield a bigger retirement nest egg.

- Retire at age 67 with pre-retirement lifestyle.

If you’re behind in your retirement saving, start now to increase your income. In today’s economic climate, it’s the rule rather than an exception to have multiple streams of income. By saving more earlier, it’s easier to meet your retirement goals.

Bonus: How To Catch Up On Your Retirement Savings

What’s Wrong with the Fidelity Retirement Savings By Age Guidelines?

If this seems daunting, Fidelity states that these are “guidelines” and not hard and fast rules. We’re all different and there are multiple variables that impact planning for retirement savings. The Fidelity Retirement guidelines are conservative. If you follow the Fidelity retirement savings rate suggestions., you should have enough to be on your way to a solid retirement income plan.

Fidelity developed the retirement planning salary multipliers scientifically by examining many historical market situations. These conservative recommendations assume poor market and economic situations. Fidelity claims, with a 90% confidence level, that these retirement savings levels will support reasonable spending in retirement.

Realistically, your retirement situation could require either greater or fewer financial resources in your senior years.

Retirement Savings Guidelines; Factors to Consider

Retirement planning should begin in your 50’s or so, and requires some assumptions.

How much do you expect to receive from Social Security and other pensions or annuities? SSA.gov provides a print out of your expected retirement income.

Where are you going to live in retirement? If you’re planning on retiring in New York City or London England, you better have a boatload of cash saved up. Retire in Mississippi or Manila and you’ll need less cash for retirement.

What will you do in retirement? What you may do in your 60’s will be different from activities in your 80’s and 90’s. Financial advisors find that spending is higher for new retirees, tapers off and then rebounds in the final years.

Do you plan to participate in expensive travel in retirement? If you have plans to travel the world in your later years, you might need more money than a homebody.

What are your expectations for out of pocket healthcare? Healthcare is a big unknown. A CNBC.com article stated that a healthy 65 year old couple might pay approximately $250,000 on healthcare during the future decades. This quarter of a million dollar estimate excludes out-of-pocket expenses and long term care costs.

Will you work in retirement? My uncle, now age 98, worked part time until he was 80. My father-in-law, who passed at age 102, worked full-time until age 80. Many of my Uber drivers are retirees, seeking extra cash. I’m certain some of the helpful associates at Home Depot are working part time in retirement. This makes a difference in your cash flow.

All of these factors have a tremendous impact on the amount of money you’ll need in retirement.

Next,, try this comprehensive retirement calculator, to test out whether you’re on track for retirement. First,, input your financial information and make some assumptions about spending in retirement. The software then gives you a percent likelihood of meeting your retirement goals.

How Much Money Will You Need in Retirement?

According to Zvi Bodie in Risk Less and Prosper, your goals, values, career path and preferences impact how much money you need. You need to estimate the price tag of your retirement vision. Retire abroad (in some locations) and you can live on $20,000 per year. Live in a motor home in your home country and you can keep retirement costs affordable.

Financial independence means different things to different people. Like so many activities in life, personal finance choices are personal. It’s helpful that Fidelity is setting approximate benchmarks to quantify the retirement decision. But, review these numbers with caution and an eye for your personal goals and values.

One of the best retirement planners is FREE from Empower. I have used it and the set up is fast and secure. Click below to try the retirement calculator and tools.

Fidelity’s Retirement Savings Action Steps

Spend some time evaluating your retirement expectations. And don’t say, “I won’t retire.” Like it or not, everyone comes to a point in their life, either by choice or circumstance, when work is no longer possible.

These Fidelity retirement savings by age are based on the Consumer Expenditure Survey (BLS), Retirement Statistics and incorporate Income Tax estimates, IRS tax brackets and Social Security benefit calculators. Fidelity developed the salary multipliers through multiple market simulations based on historical market data, assuming poor market conditions to support a 90% confidence level of success.

Create a plan for your retirement:

- Use a retirement calculator and test out various scenarios. Add in spending goals or part-time work. Find out how your goals interact with your current and future expected retirement savings balance.

- Do a values exercise and rank the value you receive from your spending. Redirect less important discretionary spending to a retirement investment account.

- Calculate your net worth, spending and saving expenses. This will help you make appropriate spending, saving and investing choices. We like this free net worth calculator.

FAQ

The Federal Reserve Survey of Consumer finances, 1989 – 2022 surveyed Americans and found that in 2022, the average retirement savings for those aged 45 to 54 was $313,220 in 2022. In contrast, In1989, that group had an average retirement balance by age 45 to 54 of $120,460.

Fidelity’s 45% rule states that you should plan to save and invest enough to replace at least 45% of your preretirement income. This rule assumes that you retire at age 67 and have no pension income, other than Social Security. This amount was determined based upon the Bureau of Labor Statistics Consumer Expenditure Survey and considers income, taxes and Social Security benefits.

USA Today, using Vanguard data reports on the average 401(k) balance by age:

Under 25: $5,236

25 – 34: $30,017

35 – 44: $76,354

45 – 54: $142,069

55 – 64: $207,874

65 and older: $232,710

This data is substantially lower than Fidelity’s savings rate. With the possibility of an employer match, when available, contributing to a 401(k) is one of the best ways to meet your retirement goals.

T.RowePrice offers a different perspective than Fidelity, on the best retirement savings by age. In an article entitled, “How Much Should You Have Saved For Retirement By Now?” author Roger Young, reminds of the nuance of retirement planning. If you earn less preretirement, your Social Security benefit will cover more of your post retirement needs. While higher earners will need to rely more on funds outside of Social Security to fund retirement spending.

The ultimate goal in answering the question of the best retirement savings by age, is to determine how much you’ll need at age 67, 65 or the year that you retire. Young reports that striving to save one and a half of your salary by age 35 is reasonable. This is less than the two times your salary saved, recommended in the Fidelity guidelines. By age 65, the T.RowePrice savings guidelines suggest you should have 7 to 13.5 times of your salary saved.

These questions aren’t answered in a vacuum. Check out a retirement calculator for guidance on how much you should save for retirement, given your personal situation.

Related

How Can I Tell If I’m On Track For Retirement?

What Are Index Funds And Asset Classes Investing?

The Truth About The 401k – Myths Exposed

Retirable Review – Monthly Income For Retirees

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.

The statement is provided to you by Barbara Friedberg Personal Finance (“Promoter”) who has entered into a written referral agreement with Empower Advisory Group, LLC (“EAG”), through which Promoter will be paid for new leads through EAG. Promoter is not a client of EAG. Promoter is not affiliated with EAG or its affiliates and Promoter’s services consist solely of referrals of prospective clients.

No fees or other amounts will be charged to Personal Strategy clients, prospective clients, or any other clients of Promoter or EAG as a result of this arrangement. Investors should conduct their own research and seek advice before making investment decisions. For more information about EAG, refer to its Form ADV through the SEC’s website.

Sources:

- https://www.statista.com/statistics/205199/per-capita-personal-income-in-the-us/

- https://www.fidelity.com/viewpoints/retirement/spending-in-retirement

- https://www.fidelity.com/viewpoints/retirement/how-much-do-i-need-to-retire

- https://www.bankrate.com/retirement/average-monthly-social-security-check/

- https://www.federalreserve.gov/econres/scf/dataviz/scf/table/#series:Retirement_Accounts;demographic:agecl;population:all;units:mean

- https://www.fidelity.com/viewpoints/retirement/retirement-guidelines

- http://money.cnn.com/2015/12/30/retirement/retirement-health-care-costs/index.html

- https://www.usatoday.com/money/blueprint/retirement/average-401-k-balance-by-age/

- https://www.troweprice.com/personal-investing/resources/insights/youre-age-35-50-or-60-how-much-should-you-have-by-now.html