Am I On Track for a Secure Retirement?

“Barbara,

Jake M.

I started investing late and although I have a military pension, a 401k, and brokerage accounts; I wonder if I am on track to a comfortable retirement. I use commission free ETFs in a taxable account.”

Am I On Track for a Secure Retirement?

You’re doing what you think is right, saving, investing and living modestly, but how do you know if you’re on track for retirement? After all, no one wants more life than money!

It’s helpful to view the process of retirement saving as a journey since you’ll likely have unexpected expenses and fluctuations in income over the years. Start planning today so that at retirement age you’ll have the resources to enjoy the chapters in your later life.

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

Here’s How to Find Out If I’m On Track for a Secure Retirement?

First, we’ll cover the quick and dirty way to figure out if your retirement savings are on track. Next, you’ll discover ways to get into the weeds with retirement income, expense and scenario analysis to uncover exactly how much you need to save and invest to meet your retirement goals. We’ll recommend our favorite retirement readiness calculator, too.

Easiest Ways to Calculate Whether You’re on Track for Retirement

Use this handy Fidelity Retirement Savings Guidelines chart to ballpark whether you have enough saved for retirement today and are on track for tomorrow. Simply, consider your household income or your own salary and your age. The chart suggests an estimate of the multiple of your current salary or annual income you need at each age.

| Fidelity Retirement Savings Guidelines | |

| Age 30 | 1x Your Salary |

| Age 35 | 2x Your Salary |

| Age 40 | 3x Your salary |

| Age 45 | 4x Your Salary |

| Age 50 | 6x Your Salary |

| Age 55 | 7x Your Salary |

| Age 60 | 8x Your Salary |

| Age 65 | 9x Your Salary |

| Age 67 | 10x Your Salary |

Source: https://www.fidelity.com/viewpoints/retirement/how-much-do-i-need-to-retire

Another “rule of thumb” to answer the question, “Is my retirement on track?” is to replace 80% of your current annual income in retirement. Use this rule cautiously as your pre-retirement income is only a guide, as you might want to travel or eat out more, causing an increase in your desired retirement spending.

If you’re willing to dig deeper into your finances for a clearer view of the likelihood of hitting your retirement goals, then using a retirement calculator is the way to go.

Check out our favorite FREE Customizable Retirement Calculator:

To get the best retirement readiness results, after creating a login, link your financial accounts to the FREE Empower Retirement Calculator.

Use a Retirement Calculator

For the best estimate of how much you’ll need to save and invest, gather this information first, then input the data into a retirement budget calculator:

Retirement Income Expectations

- Current savings and investment account balances

- Estimate Social Security benefits

- Additional retirement income such as pensions, expected inheritance or part time work during retirement

Retirement Spending Estimates

- Annual retirement spending

- Additional spending events like home renovations, charity or new car

A retirement calculator incorporate various saving, income and spending scenarios and help you to plan.

Empower Free Retirement Calculator

We’ll use the Free Empower Retirement Calculator to help determine if you’re on track for retirement.

The free Empower Retirement Planner is among the easiest tools to help you figure out if you’re on track for retirement. All you do is sign up here, link your accounts. This step will take five to ten minutes. Next, click on the “Planning” menu item > go to “Retirement Planner” and you’re read to go.

Using your linked accounts, along with the assumptions that you input, the Empower Retirement Calculator the likelihood percentage of reaching your retirement goals. Change your inputs and the retirement likelihood percentage adjusts.

Initial Settings

Estimate your expected tax rate, inflation rate and life expectancy. Obviously, these and other inputs, impact the ultimate determination of whether you’re on track for retirement, or not.

Savings Assumptions

Input Current savings, expected yearly savings and toggle the yearly savings slider to indicate an increase above inflation savings percent.

Income Events

Input Income assumptions like pensions, Social Security, partner income, inheritance, part-time work in retirement or other.

You can change these at will to determine how they will affect your retirement account value.

Spending Goals

You’ll start with the general Retirement spending goal and input at what age you expect to retire, how much money you’ll need each month, whether the spending amount should decrease or not. Last, you’ll plug in an expected annual spending minimum.

With all the future unknowns, we don’t recommend decreasing your spending amount expectation during retirement.

Next, you might add in additional spending goals such as a vacation, home remodel, charitable gift, or other expected spending aspirations.

Are You On Track to Retire Answer

Based upon your synced investment portfolio and inputs, the graph shows portfolio growth from today through your life expectancy estimate with best and worst case scenarios. You’ll get an approximate percent describing the likelihood of reaching your retirement expectations.

Change the inputs, to investigate alternate scenarios.

Investment Objectives

Incorporated into the retirement assumptions is the composition of your investment portfolio, and expected rates of return for various assets.

Stock and stock ETFs have delivered higher long term returns than bonds or cash investments. If you’re unsure of how to invest or where to invest for retirement, the simplest strategy might be to use a robo-advisor like M1 Finance or Wealthfront.

Automatically invest for retirement with a tax-advantaged brokerage account. Custom-build your portfolio or choose a pre-made Expert Pie based on your long-term goals.In addition to the Empower Retirement planner, the platform also offers a free Investment checkup. The benefit of this tool is to help you decide if you’re investments are best aligned for your age, risk level, and future financial goals.

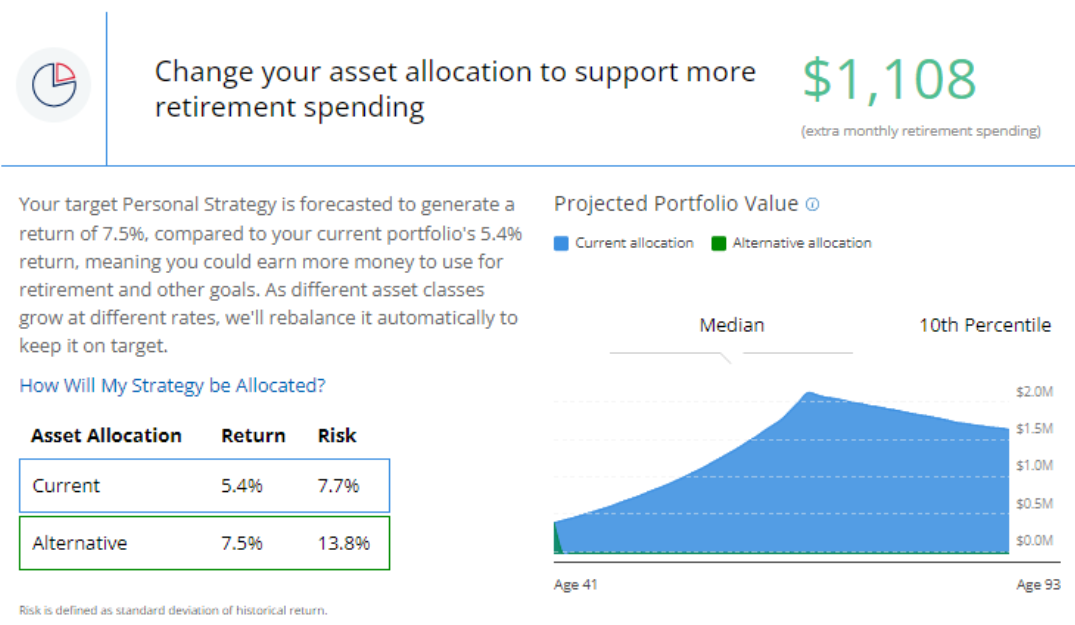

The above portfolio has a very high 40.5% invested in cash and another 21.7% in alternative REIT real estate funds. This is a very conservative portfolio for a 41 year old.

The recommended asset allocation recommends roughly 75% invested in U.S. and international stocks, 11% in bonds and 10% in the REIT alternatives asset class.

Implementing these asset allocation suggestions are projected to support $1,108 additional monthly retirement spending.

Where to Save for Retirement

The younger you are, the less you need to save to meet your retirement goals. The government has made it easy to save for retirement and receive tax breaks doing so.

Workplace Retirement Account – Most employers offer a 401k, 403b or other tax advantaged retirement plans. Many also offer a match up to a certain percent of amount invested, frequently 5% or so. Choose the amount you want deducted from your paycheck and select the investments. In most cases, the money will not be taxed until you withdraw the funds in retirement, thus saving you money on your tax bill today and in coming years.

Roth IRA – A retirement account where you contribute money, after taxes are paid. The money in the account grows tax free and can be withdrawn after age 59 1/2 without tax liabilities. You decide where to open the Roth IRA and how to invest the money. Or, you might choose to work with a financial advisor to help guide you.

Traditional IRA – Similar to your workplace retirement account, you contribute pre-tax dollars into an account, and the money compounds until withdrawn in retirement. You’ll pay tax on the withdrawals in

Taxable Investment Brokerage Account – You can invest in stocks, bonds, funds and other assets in most brokerage accounts. Typically, your stock and bond investments will compound and grow more quickly than the cash in your savings account. Depending upon your financial situation, you might want to save for retirement in individual retirement accounts and a taxable investment account. Many investment brokers also offer basic investment advice.

Click below to answer the questions, “How much should I have in my 403B account? Or 401K account:

Easiest Way to Save for Retirement

The easiest way to save for retirement is to have the money automatically withdrawn from your paycheck and transferred to your 401 k, Traditional IRA, Roth IRA and/or investment brokerage account.

You’ll learn to live on what is left and this simple action will ensure that your money will last throughout your life. When you receive a raise, use that opportunity to boost the automatic deposits into your other retirement accounts.

Meet Retirement Milestones With These Tips

- Invest enough in your 403B or 401K to receive the total employer match. Don’t leave “free money” on the table.

- Increase your savings rate as soon as possible. Aim to save 15% of your salary for retirement.

- If your company retirement plan offers automatic increases, sign up today.

- If you’re age 50 or older take advantage of the retirement contribution catch up provisions, which allow you to invest more in tax advantaged retirement plans.

- Curtail overspending and put a pause or waiting period, before making any unplanned purchases. A few days to a few weeks will curtail impulse buying.

How Much Money do you Need to Retire? Wrap up

These strategies will help you determine how much money you will need to retire. The best way to ensure your golden years are financially secure is to spread out todays earnings over your lifetime. Pay attention to your savings rate, early. Enroll in your workplace 401k plan. Automate additional saving and investing into an IRA and/or investment account. Use a retirement calculator LINK to fine tune your retirement readiness. Spend less than you earn, start saving and investing when you’re younger and your likely to fulfill your retirement plan.

Jake seems to be doing everything right. If he takes advantage of the retirement account catch up contributions for those over 50, he’ll accelerate his investment growth. The answer to Jake’s question, “Am I on track for a comfortable retirement?” ultimately depends upon the numbers, but he is taking the right steps to get his retirement on track.

FAQ

Fidelity Investments has come up with a rough estimate of suggested savings by age. These guidelines indicate that you might be on track for retirement if you have saved a particular multiple of your salary at certain ages. At age it’s recommended that you have twice your annual salary saved and/or invested for retirement. At age 50 you should have six time your annual salary and at age 60 you should have eight times your salary saved for retirement. These estimates will vary based upon when you expect to retire, how much you’ll spend in retirement and whether you’ll be working in your golden years.

There are many ways to determine if you are on track for retirement. Many suggest using the Fidelity Guidelines which suggest that you need a certain multiple of your salary saved at each important age. For example, at age 67, you should have 10 times your salary saved. Other handy tools for determining your retirement readiness include assuming that you’ll need enough money to allow you to withdraw three to four percent of your nest egg annually. So, if you have $500,000 saved for retirement, you should be able to get by on your Social Security benefits plus $20,000 from your investments or savings.

To figure that out, consider how much you estimate you’ll spend in retirement annually. Then estimate your Social Security or other Pension benefits. The difference between your benefits and your spending is the amount you’ll need to make up with withdrawals from your investments. You can use the 4% rule and save enough so that you can withdraw 4% from your investments to spend. If you need $30,000 per year from your investments, you’ll need $750,000. It’s more accurate to use a retirement calculator to help you estimate how much money you need to be on track for retirement.

A recent CNBC Your Money survey, conducted by SurveyMonkey found that the majority of Americans, or 56%, do not believe they are on track with their retirement savings. Using that data, 44% of Americans believe they are on track for retirement. One survey result might not provide enough data to adequately determine the true amount of Americans that are on track for retirement.

How much money you need to retire at 60 depends upon your spending and lifespan. Considering the Fidelity guidelines a 60 year old needs eight times their salary saved and/or invested to retire. One eighth of $5 million is $650,000. So unless your current salary is higher than $650,000, you should be fine to retire. Another way to check your retirement readiness at age 60 is the 4% rule. Can you live on a withdrawal of 4% annually or $200,000 from your portfolio. If these simple estimates seem to fit your situation, then you have a ballpark estimate of whether $5 million is enough to retire at age 60.

Generally, 15% of your income is a sound saving goal. If you can’t meet the goal right away, increase your savings amount in small increments. To check your retirement readiness progress, use a “Am I on track for retirement calculator,” like this one.

Sign up to use our favorite FREE retirement readiness calculator from Empower below:

Related

- Save For Retirement Now

- Empower vs Ziggma Portfolio Tracker Review

- Too Scared To Retire?

- We’re Talking Millions Review – Free Copy

- 5 Biggest Retirement Mistakes To Avoid

- Should I Invest A Cash Windfall In The Stock Market?

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.