A 401(k) retirement account is a powerful tool for your financial future to help you prepare for later years. Companies offer this program to eligible employees, and it’s an ideal path to create your retirement savings. However, many misconceptions surround this investment account, and lack of 401k knowledge can cost you.

Find out how 401(k) myths can hurt your long-term wealth. Yes, investing in your workplace 401(k) is essential, but there’s more to retirement investing than that!

Choose investments wisely and invest outside your 401(k) account as well. Learn the truth about the 401k and how to maximize retirement investing.

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

10 Retirement Myths-Believe at Your Own Peril

Check out our list of 401(k) myths exposed to achieve the best out of your retirement plan:

401k Myth #1 – The 401k Is the Best Place for All of My Retirement Savings

Not necessarily.

There are many types of 401k plans, some better than others. You hope your workplace 401k plan generally has low-fee mutual funds and low management expenses. It’s also desirable for your 401k to have a point person or offer access to professional advice for your questions.

If your 401k investment choices are filled with high fee, actively managed mutual funds, excess company stock, or other less desirable choices, you might need to consider other types of investment accounts for your retirement dollars. In this case, only invest enough in your employer’s 401k plan to receive the company match. Invest the remaining retirement savings in a Roth IRA or Traditional IRA outside the company plan.

Understand the fees that your 401k plan is charging. If they’re too high, get the employer match and open a Roth IRA!

401k Myth #2 – If I Invest the Minimum in My 401k, Then I’ll Have Enough Retirement Savings

False.

The myth is false. What if you’re age 35 and you invest $100 per month for 30 years in your retirement account? Let’s take a conservative approach and assume that the $100 is invested each month in a fixed bond fund with an average rate of return of 3% per year. At age 65, your account will be worth $58,419. You’ll have invested $36,000 over 30 years, which won’t double when invested.

The average monthly Social Security retirement benefit for a retiree in June, 2023 is $1,701.62. The amount changes monthly.

You need to invest enough money and receive high enough returns to give you more significant growth than 3% per year. Social Security won’t be enough to fund most people’s retirement, and thus, you must make up the difference.

In general, you’ll need to invest at least 10% to 15% of your income, depending upon your age, in both stock and bond funds to have a comfortable retirement. Develop an appropriate asset mix and invest enough per month to fund the difference between your expected Social Security benefits and your financial retirement needs.

401k Myth #3 – I Don’t Need to Worry about Adjusting My Retirement Target for Inflation since it’s Been so Low

False.

Many retirement calculations ignore inflation. During the decade preceding 2022, inflation was very low. Not anymore!

Consider this reality, you were born in 1988 and were given $10,000 at birth. When factoring in inflation’s impact, it would take $21,877 to purchase in 2020 what the $10,000 bought in 1988. That means you need to invest your money for retirement so that it will grow and compound more quickly than inflation.

Put it in another way: With an inflation adjustment, an investment in the S&P 500 stock index in January 1988 would yield an annualized 5.9% return after accounting for inflation, according to the DQYDJ calculator. That’s akin to an 8.56% return without considering inflation’s impact.

Don’t forget to factor in inflation when calculating your future investment returns!

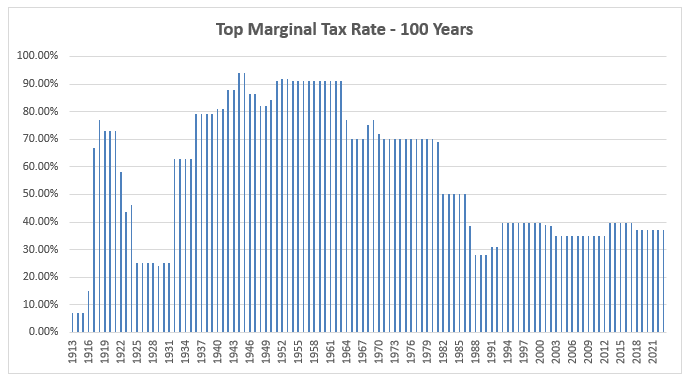

source-https://www.taxpolicycenter.org/statistics/historical-highest-marginal-income-tax-rates

401k Myth #4 – Your Tax Bracket Will Be Lower When You Retire

Maybe so, or maybe not.

Retirement investing requires making assumptions. When you invest in your 401k, you are saving on taxes today, with the expectation that when you withdraw your retirement money in the future, you’ll be in a lower tax bracket. Yet, this may not be the case.

Let’s stroll down memory lane with taxes as we did in the previous inflation myth section.

Notice that marginal tax rates haven’t been as low as they are now since the 1920s and 1930s. During most of the 1900s, the marginal tax rates were much higher than now. This fact raises the question, “Are you certain you’ll be in a lower tax bracket when you retire?”

You may assume your income will be significantly lower in retirement, yet, remember that at age 72, you must begin withdrawals from all of your retirement accounts except your Roth IRA. That required minimum distribution (RMD) will likely increase your taxable income. Don’t assume you’ll be in a rock-bottom tax bracket in retirement.

In the future, income tax rates may drift upward, and your taxable income may not be as low as expected. When doing your retirement planning, consider that your tax rate may not be lower when you stop working than it is today.

401k Myth #5 – My 401k is Free & I Don’t Need to Think about Fees

False.

There are various fees you may be assessed when investing in your 401k. The myth that 401k investing is free is rubbish. The U.S. Department of Labor encourages consumers to consider fees when investing in their employer’s plan. Following are sample fees you might encounter in your workplace retirement account:

- Plan administration fees: Cover the day-to-day operation of the program.

- Investment fees: Every mutual and exchange-traded fund (ETF) charges a fee, generally a percentage of assets under management. The lowest fee index funds might charge 0.03%, whereas an actively managed mutual fund could charge up to 0.90% or more.

- Sales charges: Some investments come with a special commission fee, charged when the particular investment is bought and/or sold. These fees may also be called ‘loads.’

- Service fees: These charges might be a flat monthly amount or a specific expense for participating in special plan features.

401k Myth #6 – It’s Best to Buy as Much Company Stock as Possible at a Discount

False!

Many employers offer employees the opportunity to buy company stock at a discount. Don’t assume that this’s a ‘can’t miss’ opportunity. Regardless of how fabulous your company is, consider diversifying your retirement monies. Imagine if your company hits a rough patch and its stock value tanks. Then, for added injury, you’re laid off.

There is a significant problem with over-investing in company stock. With the average 401k plan participant holding more than 7% of her investment portfolio in company stock (according to the Investment Company Institute), you may accidentally set your portfolio up for future losses.

Diversification is the bedrock of successful investment management. The benefit of maintaining a diversified investment portfolio is that when one stock, fund, or asset class tanks, you’ll have others that counteract the drop and increase in value. If you have too much invested in your company stock, even if bought at a discount, you’re opening up your financial future to the possibility of potential loss should your company hit a rough patch or suffer an investment market decline.

401k Myth #7 – Your Employer Takes Care of Your 401(k) on Your Behalf

False

Even if your employer is the 401k sponsor, they aren’t your investment manager! Their role is limited to contributing money toward your savings, a percentage of your contribution (employer match). It’s your responsibility to look out for your future by managing your 401k and picking the appropriate investments.

Otherwise, you fail to meet your retirement goal if you leave the management of your 401k to your employer or 401k administrator.

Fortunately, there are excellent online resources to aid in your educational education and your 401k management company may offer educational resources.

401k Myth #8 – You’re Automatically Registered for Your Employer’s 401(k) Plan

It may be the case or not.

Although many employers automatically enroll their employees in their 401k plan, don’t assume it’s the case with your employer. Take the initiative to contact the HR officer and verify your enrollment.

If you’re already enrolled, confirm that You agree with the contribution amount. If not, adjust it depending on your investment goals and capability.

Also, it’s essential to understand:

- If the employer will make changes throughout the year.

- Your investment options other than target date funds.

- How you can change your investment options.

- The costs of your 401k investment options.

401k Myth #9 –Target Date Funds Are the Best 401k Investing Strategy

Yes, to some extent.

The target date funds investment strategy is popular for a one and done investment strategy. The target date fund choice is based on your anticipated retirement date (2030, 2040…).

The investment funds within the target date fund are initially allocated to higher return, more volatile stock market funds. As you get closer to your retirement date, the asset allocation becomes more conservative, with greater allotments to more stable bond funds. This investing strategy keeps your 401k investment strategy hands-off.

Target date funds aren’t all alike, so it’s important to review the fees charged by the fund. You might want to meet with a plan advisor to ensure that you understand all of your 401k investment options.

401k Myth #10 – You Don’t Need to Review 401(k) Statements

False

Reviewing your 401(k) statement several times a year is a wise move.

It’s wise to make sure your contributions and your employer’s match are being invested according to your preferences.

Understand that investments in financial markets go up and down. So, don’t panic when you notice a decline in the portfolio’s value. This is a normal cost of investment. The long term trend of financial markets is up!

7 Tips for Managing Your 401k

- Carry the investment to term. If you invest part of your 401k in the stock market fund, stay the course even if market downturns occur. Don’t trade out of stocks, when the market hits a periodic hiccup. Continuing your investment plan during market drops leads to higher long term returns.

- Make good use of your employer’s match. Your employer will only put in their share after you have contributed yours. Therefore, be consistent in your contributions to avoid missing that portion of your compensation and benefits package.

- Understand your 401k investment options. You should understand the specific investment(s) you select for your 401k money. When choosing a mutual fund, know what investments it owns and how it aligns with your investment goals and risk tolerance. If you’re unclear, choose a target date retirement fund, aligned with your 65th birthday.

- Change your investment options over time. As you get closer to your retirement, it’s good to move your investment composition from higher risk to assets with potentially higher growth, like stock funds, to more conservative assets with lower risk like bond funds. Target date funds do this automatically.

- Consider your expenses before contributing the max. Ensure that you have a ready-access emergency fund before investing the maximum in your 401k. That prevents early withdrawals that can trigger taxes and penalties.

- Diversify your investments. Investing in various mutual funds across diverse asset classes, keeps you on the safe side. Investment diversification helps you lower the likelihood of large investment losses, when one asset class declines, you’ll have others to bolster your returns.

- Regularly rebalance your investments. Maintain the balance of your initial asset allocation. That prevents fast-growing investments from dominating your portfolio.

- If you switch jobs, don’t cash out your 401k. If you’re younger than 59 ½ you’ll owe taxes plus penalties. Consider rolling the 401k over into an IRA account.

401k Myth Wrap Up

The truth about 401ks – Although the 401k is a good retirement savings account with many financial retirement benefits, it isn’t perfect. Be aware of 401k myths to shield your future self from unpleasant financial surprises. Know what prices you’re paying. Understand what investments are in your account. If you want the easiest investment management choice, pick the target date fund.

Review these ten 401k myths to maximize your retirement plans. Also, it’s helpful to involve a financial advisor in your retirement investment decision-making, if you have any questions.

FAQ

No, your 401k isn’t safe if the market crashes. Since 401(k) is invested in stock and bond funds, your account’s value will fluctuate, depending on the market performance. This is nothing to fear, but the normal ups and downs of investing in the stock and bond markets. The volatility is the price you pay to receive higher investment returns. Since your 401k is invested for retirement, it’s very likely that your 401k account will be worth a lot more than you invested, upon retirement.

Diversification in stock and bond investments, will help temper the account’s price volatility.

There are all sorts of financial risks. If you keep all of your money in the bank, you risk losing the purchasing power of your money due to inflation. In the short term, investment markets are volatile and during any one year you might experience a gain or loss in value. But, over many years, the stock market has earned an average nine to ten percent annual investment return. While bond funds have earned four to five percent annual returns over the long term. These returns are higher than cash in a savings account and are likely to protect your money from the risks and loss of purchasing power due to inflation.

Over decades, investing regularly in your 401k account is one of the best ways to build wealth for retirement and turn thousands of dollars into hundreds of thousands of dollars or more.

Yes, your 401k is still safe, for long term saving and investing. Your money is protected with SIPC insurance against the investment companies failure or bankruptcy. The plan is generally considered a safe investment option to save for retirement. Just be aware the the value of your investments will go up and down in the short term. But over decades, the trend for financial investing is positive, and offers better returns than bank savings accounts.

Why Is 401k Going Down?

401k is going down due to one or several factors that affect the rate of return. They include high management and administrative fees, market downturns, economic recessions, and poor investment choices. It’s important to know what you are invested in. If you have set up a thoughtful investment plan, and the plan’s fees are reasonable, you don’t need to worry about temporary account value declines. Periodic investment declines occur when investing in stock and bond funds. Fortunately, over long periods of time, the investment gains have far outweighed the losses.

No. If you take money out of your 401k account before you reach age 59 ½, you’ll have to pay taxes on the money and also pay an early withdrawal penalty. You’ll also miss future growth in your investments. Don’t let fear drive your investing. The benefit of regular investing through a 401k account is that when markets decline in value, you’ll be buying more shares at lower prices. When markets rebound, as they have done in the past, you’ll be glad that you continued regular investing in your 401k account.

It is very unlikely that your 401k would go to zero. The only way the 401k would ultimately go to zero would be after retirement, when you have withdrawn all of your contributions. A diversified investment portfolio might experience on occasional loss, but it is unlikely that the account’s value would decline to zero.

Related

- Tax Benefits Of 401k Plans

- Is A 401k The Same As An IRA?

- The Difference Between 401k Loans And 401k Early Withdrawals

- Roth Or 401k, Which To Max Out First?

- 6 Dangerous Investing Myths

- Retirable Review – Monthly Income For Retirees

- How To Catch Up On Your Retirement Savings

- Recession-Proof Your Portfolio

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.

The statement is provided to you by Barbara Friedberg Personal Finance (“Promoter”) who has entered into a written referral agreement with Empower Advisory Group, LLC (“EAG”), through which Promoter will be paid for new leads through EAG. Promoter is not a client of EAG. Promoter is not affiliated with EAG or its affiliates and Promoter’s services consist solely of referrals of prospective clients.

No fees or other amounts will be charged to Personal Strategy clients, prospective clients, or any other clients of Promoter or EAG as a result of this arrangement. Investors should conduct their own research and seek advice before making investment decisions. For more information about EAG, refer to its Form ADV through the SEC’s website.

The statement is provided to you by Barbara Friedberg Personal Finance (“Promoter”) who has entered into a written referral agreement with Empower Advisory Group, LLC (“EAG”), through which Promoter will be paid for new leads through EAG. Promoter is not a client of EAG. Promoter is not affiliated with EAG or its affiliates and Promoter’s services consist solely of referrals of prospective clients.

No fees or other amounts will be charged to Personal Strategy clients, prospective clients, or any other clients of Promoter or EAG as a result of this arrangement. Investors should conduct their own research and seek advice before making investment decisions. For more information about EAG, refer to its Form ADV through the SEC’s website.