A reader wrote in and asked, “Why should I invest in bonds? After all, the yields are low and don’t bond values drop as interest rates rise?”

I started investing in bonds in my mid 20’s and have enjoyed their dividends for years. When interest rates were high, I even received double digit bond interest (coupon) payments – can you believe that today?

Understand the importance of bond investing. Learn why bonds remain a good investment today.

Investing in Bonds for Beginners

“Are bonds a good investment now?” is a great question. After all, bonds, typically offer lower returns than stock investments. And, when interest rates are rising – like they are now – bond values tend to decline.

Yet, bond investing is a good idea.

Let’s start with a quick bond investing 101. And, if you already know about investing in bonds for beginners, then skip down to the “Why are Bonds a Good Investment’” section.

A bond is similar to a loan, where you are the lender. When you buy a corporate bond, you lend money to a corporation. The company might use the money to grow or acquire another business. With government bonds, you lend money to the government. A municipal government might use your bond investment to build a stadium or repair roads.

How Much Does a Bond Cost?

Bonds are issued in set amounts, typically $1,000. This is called par or face value. Bonds also have established maturities, anywhere from a few months to 30 years. If you buy a bond at issue, you’ll pay the par value, but if you buy it later, it might cost more (a premium) or less (a discount) than the face value.

Bond Coupon Payments

When you purchase the bond, in exchange for your payment, the issuer pays you interest and ultimately repays the loan (principal payment). In bond-talk, the interest payments are called coupons. That’s because many years ago, a paper bond had small “coupons” attached to the bond, which you cut off every six months and presented to the bank in exchange for your interest payment.

Bonus; Should I Sell Stocks Now That Markets are Peaking?

When interest rates rise, like they are doing presently, new bonds offer higher interest or coupon payments. But, old bonds, become worth less – their principal value drops. That’s because an investor can go out and get a new bond paying the higher interest rate, so why would she pay same amount for a lower interest payment?

With rising interest rates, longer maturity bonds will fall more in price than shorter maturity bonds.

In the 1980’s, I bought a bond with a 10% coupon payment. Twice per year, I’d cut the coupon and go to the bank for the interest payment. I miss the high interest rates of the 1980’s, just not the high inflation rates!

How do Bonds Differ from Stocks?

When you buy a share of stock, you’re purchasing an ownership stake in the company. The stock may or may not pay a dividend. And, if the company defaults, then bond holders get their money back before stock holders.

Historically, stocks have returned approximately 9% per year, while bonds earned roughly 5%. That’s because stock investing is riskier than investing in bonds. So, to entice people into riskier investments, stocks must offer higher returns than other, safer investments such as bonds and CDs.

Types of Bonds and Bond Funds

Unless you have at least $50,000 to invest in several bonds, you’re better off buying a bond mutual fund or bond exchange traded fund (ETF). With funds, you own a basket of diversified bonds for a small amount of money.

Individual bonds and bond funds come in many varieties.

Similar to stock funds, types of bond funds include all-in-one diversified bond funds such as Vanguard’s Total Bond Market Index Fund (VBMFX), corporate bond funds, government bond funds or riskier high-yield bond funds. You can also buy funds that include bonds of varying maturities (we’ll talk more about this below).

Where to Buy Bonds?

Bonds are easy to buy. Visit the fixed-income section of your online brokerage account to sort through individual bonds. You can screen by quality, maturity and type of bond.

Bond funds can also be bought through any online broker.

If you want an easier way to buy bonds, you might consider a robo-advisor that creates a balanced stock and bond portfolio such as Betterment or M1 Finance.

With M1 Finance, you can choose from pre-made investment portfolios or create your own. After you’ve selected your investments, M1 Finance and Betterment will rebalance your assets periodically.

Why Are Bonds a Good Investment?

After a ten year bull market for stocks and low interest rates for bonds, you might wonder, “Why buy bonds?”

Buy bonds because investment markets are volatile and most people don’t like to lose money!

The average annual stock and bond returns of 9% and 5% respectively, mask the volatility in the investment markets.

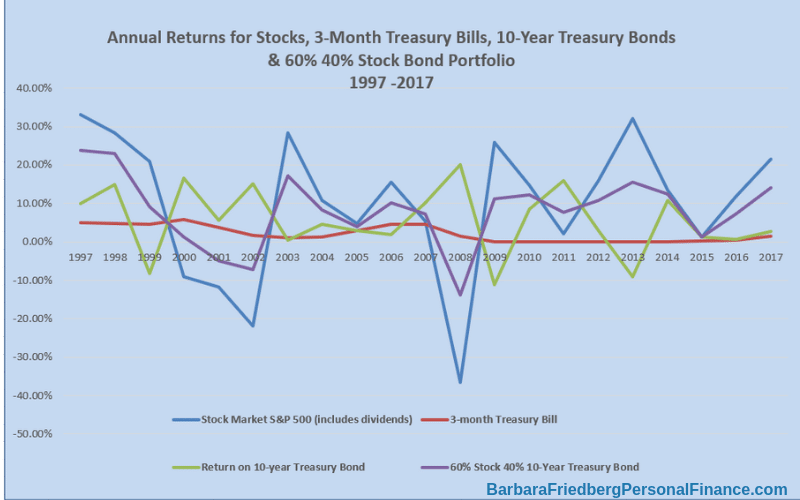

Notice the blue stock market line. During 1997, the stock market returned 33.10%. The next year it rose 28.34% and bonds had amazing returns as well at 23.84% and 22.97% respectively.

Jump ahead three years to 2000 through 2002 and the stock market lost 9.03%, 11.85% and 21.97% respectively for a cumulative loss of more than 40%. Even the hardiest investor would cringe at a 40% loss.

From 2000 through 2002, the 10-year Treasury Bond returned 16.66%, 5.57% and 15.12%. Clearly, during down stock market years, it’s helpful to own bonds, which will likely go up or at least, won’t fall as drastically as stocks.

If you owned a diversified investment portfolio with 60% stocks and 40% bonds during the risky 2000 through 2002 period, then your returns would have been 1.24%, -4.88% and -7.13% for a cumulative 3 year return of -10.77%. Although a 10% loss over three years isn’t great, it’s certainly better than a 40% loss during that same period.

And that’s why you need bonds in your investment portfolio! Bonds smooth out the volatility of an all stock portfolio. Also, depending on the percentages invested in stocks versus bonds, you might improve your returns with a more diversified portfolio.

Are Bonds a Safe Investment?

If you define safety as loss of principal, then bond investing is safer than investing in stocks. Since 1997, stocks had four losing years while bonds had three. On the “Annual Returns” chart above, you’ll notice that the price swings on bonds are smaller than those for stocks.

Also, if a company defaults, the bond holder will be paid before the stock holder.

Typically, higher rated bonds have lower risk of default.

So, bonds are somewhat safer than stocks.

But, if you’re wondering, “Can you lose money investing in bonds?” The answer is “yes”.

Unlike cash in your savings account, bonds might have a losing year now and then. So if you mean “Are bonds a safe investment like cash?” The answer is no. But for investors, who want higher returns than a savings account, bonds are an important component of a well-diversified investment portfolio.

Are Bonds a Good Investment Now?

Individual bonds and bond funds are important to have in your portfolio, to diversify and temper the risk of more volatile stock funds. If you’re thinking about when to buy bonds, I believe that bonds are a good investment now.

Presently, interest rates and new issue bond yields are going up.

The Vanguard Total Bond Market Index Fund Investor Shares (VBMFX) yields 2.59% today. And if you’re more of a risk taker, the Fidelity High Income Bond Fund (SPHIX) yields 5.53% now.

So, bonds are a good investment now, but…….

There’s a catch. With rising interest rates, if you buy a longer term bond fund, the principal value of your original investment will fall. When interest rates rise, shorter term bonds and fund values decline less than longer term issues.

Read; Quicken vs. Personal Capital – Which is the Best Money Management Tool?

Here’s how to get around the peril of declining bond values as interest rates increase.

First, you can buy individual bonds and hold them until maturity. That way, you’ll get the coupon payments and par value when the bond matures. Or, you can buy a short term bond fund and reinvest your dividends. That way, the fund will lose less in value and as new bonds are added to the fund, with higher coupon payments, your reinvested dividends will lift the returns of the fund.September 25, 2018

Best Bonds to Buy Now

Best Bond Funds for Rising Interest Rates

Here are a variety of short-term bond funds for investors right now. The selection includes inflation protected government bond funds and corporate bond funds

Short term bond funds are a good choice for investors now, as interest rates continue to rise. Here are a few winners from US News and World Report:

- iShares iBonds Mar 2020 Term Corp ETF (IBDC)

- iShares 0-5 Year Invmt Grade Corp ETF (SLQD)

- Invesco BulletShares 2020 Corp Bond ETF (BSCK)

- Vanguard Short-Term Bond ETF (BSV)

Best Individual Bonds for Rising Interest Rates

Step up bonds have scheduled increases in the coupon payment. Buying step up bonds is a good way to bolster returns as interest rates rise.

Floating-rate corporate bond coupon payments are linked to a predetermined benchmark, such as the six-month treasury yield plus a percent. When the treasury yield rises, so does your floating-rate coupon payment.

Inflation protected I Bonds from the US government offer an interest rate that changes every six months, along with inflation. These protect your cash from the perils of inflation.

Treasury Inflation Protected Securities (TIPs) are another government bond that is issued with a set interest rate. Yet, as inflation changes, the principal value of the bond adjusts. So, with rising inflation, the bond value increases and your interest is paid on a larger principal value.

Individual corporate bonds with shorter maturities allow you to benefit from rising rates. When one short term bond matures, you can replace it with another, higher-yielding issue. To find these bonds, visit your online investment broker.

Are Bonds a Good Investment Now – Wrap Up

Finally, let’s assume that future investment returns will follow a similar path to the historical gains. If that trend persists, then you have a few choices. You can invest in an all stock portfolio and potentially achieve the highest annualized returns, over the long-term. Yet, that means there will be years where your investments might drop up to 40% or 50% in one year!

If you’re somewhat risk-averse, like most investors, you’ll add in some bonds and bond funds to temper your investment portfolio’s ups and downs.

So, the answer is, bonds are always a good place to invest. Yet, when interest rates are rising, keep maturities short. And when interest rates peak, or begin to fall, go for longer maturity bond investments.

Related

- TIPS Bonds – Invest to Preserve Your Capital

- Should I Invest In A Bond Fund Now?

- 5 Low Risk Investments For a Rising Interest Rate Environment