What is Your Net Worth? Get Rich Step-by-Step

“Money is only a tool. It will take you wherever you wish, but it will not replace you as the driver.”

~Ayn Rand

The first step in creating a fitness and diet plan is to step on the scale. Nobody likes to get weighed, but you have to accept where you are right now, before proceeding to change. It’s how you keep track! The same applies to financial health. It’s tough to track your financial progress or meet your future goals without calculating your net worth.

Since I began working, I have used my net worth as a measure to determine whether I’m headed in the right direction, or not.

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

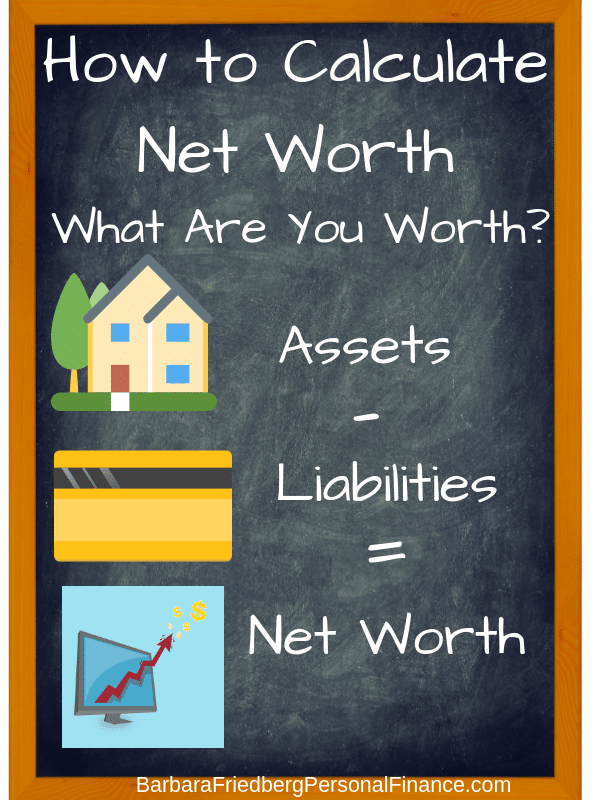

Your net worth or tangible net worth as it’s also called, is the total of your financial worth on a particular day. Net worth includes everything your own that could be converted into cash minus all the money you owe. Simply put, net worth is assets, or what you own, Minus liabilities, or what you owe. Just like your weight, your net worth goes up and down.

Why Calculate Your Net Worth?

Why do you need to figure out your net worth?

Why should you care about the value of what you own?

If you want control over your financial life – the opportunity to travel, send your kids to college, buy a new laptop, or retire – you must be aware of your financial footprint right now.

Would you begin a trip, check out the map app, and start driving if you didn’t know where you were?

Knowing your net worth is the same principle. Face up to your financial situation, and use it as a starting point to see if you are on track and able to meet your future goals. As you develop sensible money habits, your net worth will go up and you can use it to measure your financial progress. It is the yardstick to measure your money buildup.

An added bonus of knowing your net worth; after figuring out the value of all the stuff you own, most of which you never use, you may decide to sell some of it to get more cash! Then, you can use that cash for experiences or things that you really value!

It’s easy to figure out your net worth either with a spreadsheet or a net worth calculator. I use Quicken and Personal Capital to keep track of my net worth.

Although it takes some work at the outset to link your accounts to an online money management platform like Quicken or Personal Capital, in the long run it is a real time saver and gives you valuable insight into your financial picture, at a glance.

Inspiration; Go Beyond Keeping up With the Jones’ – Change Your Perception, Change Your Net Worth

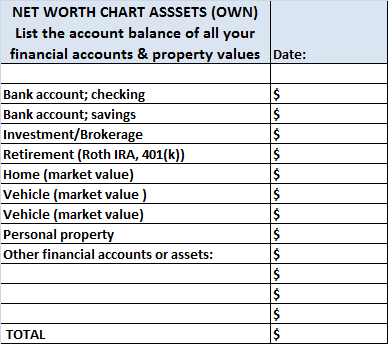

Step 1 to Calculate Your Net Worth – Your Assets

For the old school method, gather all of your financial statements: bank account(s), investment account(s), retirement account, old savings bonds stuffed in a drawer. These are called Financial Assets. When adding up the asset values of what you own, consider every account that includes cash or can be converted easily into cash. Ballpark the value of your home, vehicles, and possessions.

Assets include what you own that can be converted into cash.

List of assets includes:

- Checking and savings accounts

- Retirement account values

- Online and brick and mortar bank account values

- Investment accounts including mutual funds, stocks, bonds, and exchange traded funds

- Cryptocurrency value (remember to update this regularly)

- Government bonds

- Vehicle value

- Current market value of home equity

- Personal property

Print out the article and complete the charts, or download a net worth excel template .

Click below if you prefer to use an online net worth calculator.

Congratulations, Step 1 is done!

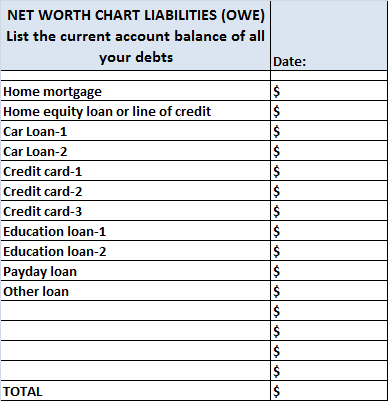

Step 2 to Calculate Your Net Worth – Your Liabilities

Wouldn’t it be great if your total Assets equaled your Net Worth?

Unfortunately, for most people, they don’t. Most Americans have some student loan debt, credit card balances, car loans and other liabilities. To continue with your financial weight, or net worth, you need to calculate assets minus liabilities.

Liabilities include everything that you owe.

List of liabilities includes:

- Credit card debt

- Student loans

- Personal loans

- Home mortgage

- Car loans

Calculating liabilities requires gathering all of your statements from various lenders and credit card companies and listing the current balance on a spreadsheet. Or you can link the debt accounts with an online financial management program like Personal Capital or Quicken.

For spreadsheet fans, follow these steps, and before you know it, you will have your current financial picture and an important part of your money education will be complete!

This step can be difficult, especially if all of your debts add up to four or five figures. So do it quick to get it over with. Next, fill in the Liabilities chart. Or, use an online financial management app.

Congratulations, you’ve done the heavy lifting. Get ready for the big finish. No matter how you net worth value comes out, you know the truth and are beginning the tough path towards money strength.

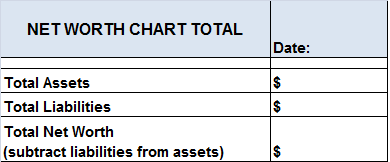

Step 3 – Calculate Your Net Worth – Assets Minus Liabilities

Next, subtract your liabilities from your assets. The result is your net worth-today. Remember that your net worth will change along with your debt levels and the value of your investments and your home.

Whew, you did it! Give yourself a pat on the back for calculating your net worth. Now what? You have your financial net worth as of today, but what do you do with it?

Free net worth calculator and financial software (compliments of Personal Capital)

Are you on track to meet your future financial goals? If so, congratulations. If not, you’ve taken responsibility for managing your financial assets.

Understanding Your Net Worth

Your net worth tracks your financial progress. Ultimately, to keep your net worth growing you want to increase your assets like savings, investing and retirement accounts, while you reduce debt. You can also grow your net worth by paying off your mortgage. Also, if your home appreciates (goes up) in value over time that will also boost your net worth.

Watch out for your vehicle, no matter how sweet, it usually falls in value and depreciates your net worth.

The beauty of a growing net worth is that the assets you amass, free you from financial stress and can be traded for time to pursue other activities. The greater your net worth, the more financial resources you have to fund retirement, pay for your child’s education, go on a vacation, work part-time or fulfill any other monetary dreams.

What if you Have a Negative Net Worth?

What if your net worth is negative? Remember, it is just a starting point. Just like your weight or your fitness level, your net worth can change. But you must make it happen!

A negative net worth occurs when you owe more than you own. A negative net worth is a reminder that you need to adjust your financial behavior. To move the net worth needle from negative to positive, begin a debt payoff plan.

Next you’ll want to increase your income with a side hustle or second job.

Many young people run up high credit card bills and later realize that paying off the debt is possible with a few lifestyle changes.

Ben Stein and Phil DeMuth in Yes, You Can Get a Financial Life! chastise the over spenders. Their no nonsense approach to money is right on target; you are only entitled to purchase what you can afford. They clobber the belief that you “need” the status items beyond your budget like the designer hand bag the stars’ carry and the exclusive resort vacation that you put on your credit card. You pay for those unnecessary extravagances with your future!

To keep your net worth growing, separate your needs from your wants. Fund your needs and prioritize your wants, based upon your extra cash. If you have debt, put the wants on hold until you’ve tackled your debt.

Check out your net worth every year or so and see if you are on financial track to meet your money goals.

How Your Net Worth Compares With Your Peers

The Federal Reserve created a median and average chart of Net Worth by Age Range. See how you compare. Remember that median means half of those surveyed were below the median and half were above. The average will be higher, as very wealthy individuals skew the results upwards. The 2019 data is the most current at the time this article was updated.

| Age | Average | Median |

| Younger than 35 | $76,340 | $14,00 |

| 35-44 | $437,770 | $91,110 |

| 45-54 | $833,790 | $168,800 |

| 55-64 | $1,176,520 | $213,150 |

| 65-74 | $1,215,920 | $266,070 |

| 75+ | $958.450 | $254,900 |

Source; FederalReserve.gov

Grow Your Net Worth Hacks

- Commit to eliminating one debt. (And then on to the next)

- Write down how much above the minimum you will pay each month to eradicate the debt.

- Find ways to save money.

- Increase your auto deposit into your 401(k) and your investment account.

- Start a side hustle to grow your income.

- For another online way to calculate your net worth, check out this Net Worth Calculator at Financial Mentor.

Related

- How Long Until I’m Wealthy?

- How Can I Tell if I’m on Track for Retirement?

- How to Cut Investing Fees and Increase Returns?

- 7 Secrets to Becoming a Millionaire

- 5 Personal Finance Habits to Help You Achieve Financial Freedom

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t personally believe is valuable.

Empower Advisors Corporation (“PCAC”) compensates Wealth Media, LLC. (“Company”) for new leads. Wealth Media is not an investment client of PCAC.

Empower Advisors Corporation (“PCAC”) compensates Wealth Media, LLC. (“Company”) for new leads. Wealth Media is not an investment client of PCAC.