The primary purpose to hold cash in your savings account is to bolster against emergencies and unexpected expenses. In other words, having cash on hand, either in a checking or savings account acts as an emergency fund. However, holding too much of your portfolio in cash – as opposed to investing in the stock market, for example – means that you are both disproportionately exposed to the dangers of inflation and not optimally employing your capital for investment. and future growth

So, the logical question is just how much cash should you have in savings to create a balance between preparing for financial emergencies and engaging in optimal financial planning.

This article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link.

How Much Cash Should I Keep in Savings and Where to Keep It

The standard “financial professional” answer to the question, “How much savings should I have on-hand?” is “roughly six to nine months of living expenses.” However, this answer is often without much basis and ignores personal differences. When you think more deeply about this answer, you’ll find it’s a bit overkill to have $10k+ just sitting in your savings account.

Instead, think of the purpose of your emergency fund: It’s to account for unexpected expenses without having to take out loans, dip into your retirement savings, or sell investments. Thus, if you lose your job – for example – you’ll have a personal safety net with which to fund your living expenses while you get back on your feet – all without interfering with your debt status, retirement accounts, and investment goals. This is why the answer is so personal: Only you know how much cash you would need to fund your living expenses for that downtime.

As for where to store your emergency funds, you needn’t default to checking accounts, as you’ll be ravaged by inflation. At the very least, you should consider methods that offer at least a little resistance against inflation via somewhat decent interest rates. Consider the following places for your rainy day fund, where you can get a good yield on your cash:

- Certificate of deposit: This locks up your cash for a certain period of time but can be withdrawn early at a small penalty.

- Money market account: Essentially a savings account but with a better interest rate due to the way the money is invested on the back-end.

- High-yield savings account: As it sounds, it’s a savings account but with an institution that markets itself by offering higher interest rates.

M1 Finance, one of our affiliate partners, offers a high yield cash account to store cash for emergencies and unexpected expenses.

How Much Cash Should I Have in Savings?

Again, your emergency fund capital is a personal choice, but some rules-of-thumb can help you. The least amount of cash to have in savings is three months of living expenses. This is a minimal rule-of-thumb, as the Covid Pandemic has shown; many people had to fund living expenses with the stimulus checks the government distributed during the pandemic.

In a declining market environment, you don’t want to be in a position where you need to sell stocks and other investments as investment prices drop, to shore up cash for unexpected expenses.

Ultimately, the amount of emergency cash you need is an issue of practicality and psychology. Investment advice would push you toward, diverting more of your cash to investments. But the average investor is conservative and more comfortable with greater cash reserves. Still others prefer to deal with unanticipated expenses via borrowing and thus do not really require a cash cushion.

Many financial companies like M1 Finance offer low interest rate loans and low margin borrowing rates for their clients, and high yield cash accounts.

In the end, there is no magic number here. The three-month rule-of-thumb is good for less conservative investors and those with quick and easy ways to generate income like freelance workers. While six-to-nine months would be more suited for conservative investors or those who might have a more difficult time gaining new employment, after leaving a job. Just to get the process started, try setting aside at least one month’s expenses for a major emergency and grow your fund from there.

How Much Emergency Cash Should I Have?

Here is a quick-and-easy method for calculating how much liquid cash you should have.

Calculate your net worth. Before you can set your financial and savings goals, you need to know your current status. Add all your assets in your savings and checking accounts, money market accounts, high-yield savings accounts, stock market investments, and all other investment accounts, including your retirement accounts – 401k, IRA, and taxable brokerage account.

Calculate your monthly expenses. Your monthly expenses include your necessities (e.g., food and housing) and your discretionary costs (e.g., eating out and hobbies). You should also include the money you put into investing and saving into this calculation.

Determine intermediate expenses. These are expenses that are less frequent than monthly, including tax payments, house repairs, and personal events (e.g., vacations, weddings and baby showers).

You can use Empower Financial Management Tools or Quicken to keep track of your net worth, savings, spending, and investing.

Check out the free Empower (formerly Personal Capital) net worth calculator. Just link your accounts and the free software will do the rest.

As soon as you understand your current financial status, you can begin creating your financial plan. For virtually all individuals – regardless of your personal finance issues – keeping cash in an emergency fund should be a priority.

How to Create an Emergency Fund?

If you already allot physical cash to food and other necessities, then creating an emergency fund is as easy as adding one more allocation. Of course, that physical cash will go into savings accounts instead of your wallet, and you’ll need to do a little financial planning to free up that cash. But the process itself is simple, just divert some of your extra funds into a cash stash.

More specifically, consider the 50/30/20 budget rule:

- 50% to fixed costs. This includes daily living expenses: food, rent, and insurance – any cost that is not discretionary. You pay these fixed costs monthly.

- 30% to discretionary costs. This includes entertainment, clothing, hobbies, and eating out. These are costs that can be cut in the case of a financial shock.

- 20% to saving, investing, emergency fund, and intermediate goals. That is, any money that is not going to daily and regular spending goes toward either irregular spending (e.g., down payment on a house), longer-term financial goals (e.g., retirement), or your savings (e.g., your emergency fund).

The easiest way to implement this rule is to automate your spending, saving and investing.

Automating your finances helps you avoid deviating from your financial and savings goals. Consider setting up an automatic deposit into a savings and investing app or directly into your bank account. Consider automating your cash into a high yield cash account either at your investment broker or another financial firm.

Bonus: How To Save $10,000 In A Year Or Less

How Much Cash Should I Have in my Checking Account?

Because checking accounts do not typically earn interest, we recommend you keep the absolute minimum in this account, if possible. Each bank and credit union has a different minimum balance for a checking account, so check with your institution. Of course, if you rely on this checking account for expense-paying, keep whatever you need. Just know that the cash in your checking account is equivalent to physical money in terms of fighting inflation – i.e., it is a decaying asset and should be kept to a minimum, without risking overdrafts.

If you have overdraft protection for your checking account, then the question of “How much money should I keep in my checking account?” becomes less important. Minimally, make sure you have enough money in your checking account to cover one month’s expenses, plus an extra cash cushion for added short term bills.

How Much Cash Should I Have in my Savings Account?

The answer comes back to understanding your expenses. Once you have calculated your monthly expenses, as above, multiply it by your chosen rule-of-thumb: three months for aggressive investors and those with ready access to cash; nine months for conservative investors and those in rigid employment industries; and anywhere in between if you’re somewhere between those two extremes. The resultant number should be the ideal amount of money in your emergency fund.

For your savings account, maximize your interest by keeping your savings in a high yield money market fund, certificate of deposit, or high yield cash account.

How Much Cash Do the Wealthy Have on Hand?

After reviewing several millionaire surveys including a 2023 CNBC millionaire survey, those with $1 million or more are keeping roughly one third of their liquid wealth in cash. Now, this survey was taken during the highest cash interest rates time period in decades. Today, in late 2024, we’re finding interest rates are trending downwards, which means that last year’s cash-equivalent 5 percent cash yields are not available today.

The wealthy typically understand that when the stock market is highly valued, as it is today, capital preservation is very important. Should the stock market experience a large decline, the wealthy tend to a large percent of their investable assets in cash equivalents, to hedge against the stock market declines.

With falling interest rates, and high stock valuations, those seeking to bulk up their cash allocations, should look to higher yield certificates of deposit, short term and intermediate term bond funds. Despite the recent decline in the fed funds rate, money market mutual funds are still delivering decent returns.

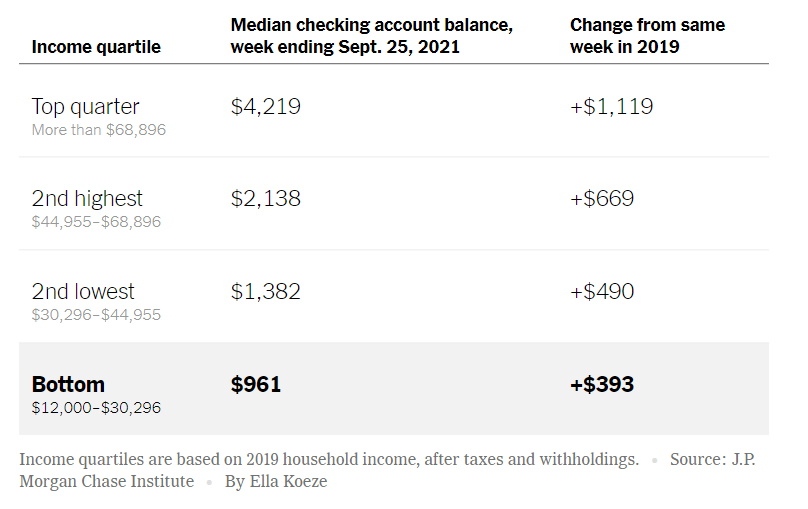

To illustrate the differences between how much cash the wealthy have on hand and those in lower income brackets, consider these checking account balances for American’s in various income groups:

“How much cash should I keep in my checking account?” varies among the wealthy and those lower income groups. In the long term, too much cash means you’ll lose purchasing power due to rising inflation. In the short term, greater amounts of cash can provide peace of mind and relief for emergency expenses.

How Much Cash Should I Keep at Home?

Keeping physical cash at home is risky due to possible loss or theft. However, having some cash around can be useful for emergencies. Still, cash in your home, whether in a safe or not, should not replace an emergency fund in a bank account, as the latter at least earns interest and is protected with FDIC insurance.

Still, it’s nice to have some cash at home for the rare emergency. For example, if you need urgent repairs at home (e.g., broken pump, AC not working, electrical issues), you can call anyone without needing to check whether they take card and without having to run to the ATM. You also might want some extra cash at home if you live in a tornado/hurricane/fire-prone area. Also, in the rare event in which there’s a run on the banks, you won’t need to join the fray.

The safest place to keep cash at home might be in an impenetrable locked safe that is difficult to open and remove from your home. Other safe places to keep cash at home might be hidden inside other household items, false floorboards, fish tanks, shell books, or pet food containers.

Ultimately, cash is nice to have, but don’t store all your emergency funds at home.

How Much Cash Should I Have in my Wallet?

In our neighborhood, the local farmers market only takes cash. So, on those days when we’re going to the farmers market, we bring $80 to $100 cash. Other reasons to have cash in your wallet include avoiding surcharges and paying workers. Some businesses enact a a surcharge for using a credit card. Handymen and home repair people might prefer cash as well. In those types of cases, you’ll need a hundred dollars cash or more in your wallet.

If you prefer to pay with a credit card and rack up reward points, then you might not need more than $40 cash in your wallet, for unexpected situations. Debit cards act like cash and can also reduce the need for cash in your wallet.

Like many personal finance decisions, the answer to “How much cash should I have in my wallet?” depends on your personal situation. Just remember that if you don’t keep much cash on hand, and pay with a credit card, pay off the balance in full each month. That way, you’ll avoid sky high interest payments.

How Much Cash Should I Have in My Investment Portfolio?

First thing’s first: cash is not an investment. Cash is important because of its liquidity and wide acceptance as payment. Cash should be held in your savings account, certificate of deposit or high yield money market fund as part of an emergency fund. When interest rates are higher than the inflation rate, then you might consider using cash as an investment and hedge against volatile stocks and stock funds.

If you are in, or nearing retirement, “How much cash should I have in my investment portfolio” takes on another meaning. IF you are drawing cash from your investment account during the next year or so, then you might hold one or more years of needed expenses in cash in either an investment account or high yield cash account. This removes the risk of having to sell stock investments after a decline.

The bottom line is that cash should used strategically, as a hedge against declining stock prices or possibly as a portion of the fixed-income asset allocation of your investment portfolio.

Wrap Up

Most investors dream of getting rich with their investments and forget the “boring” stuff, such as keeping money separate from your investment account in an emergency fund. Keeping cash reserves for an emergency doesn’t need to hurt your investments all that much, especially if you put them in liquid investment vehicles such as a money market account, certificate of deposit or short-term bond funds. During an extended down market, you’ll see your investments fall, not want to sell, and be happy that you have cash sitting on the sidelines.

Keeping some physical cash on hand is also often a good idea, considering withdrawing cash can be impossible if your account is locked or stolen. Personal finance reminds us to diversify, not just in investment vehicles but also where you place your wealth. As for cash, it’s all about security: A branch bank is nice to have for in person withdrawals and human contact; cash in your wallet is well-appreciated during a technology bubble crash or unexpected emergency.

Ultimately, financial experts will advise against having all of your money in cash. But being prepared for worst-case scenarios like a national emergency or job loss requires cash reserves. Start your emergency fund today, and your biggest possible regret can only be “I never needed to use that cash.”

Compare that with the alternative of not having an emergency fund when you need it, and… well… I’m sure you can imagine countless hardships in such an event.

Check out our recommended Empower Net Worth Calculator, just link your accounts, and Empower delivers your net worth along with a retirement planner and other useful financial tools.

Related

- Savings Tips For Renters – From Financial Pros

- 8 Savings Tips From Warren Buffett

- 51 Ways To Drastically Cut Expenses

- Basic Savings Strategies

- What Percent Of My Income Should I Save?

- M1 Finance – Pros and Cons

- Why Can’t I Save Money?

- Should I Invest A Cash Windfall In The Stock Market?

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t believe is valuable.

The statement is provided to you by Barbara Friedberg Personal Finance (“Promoter”) who has entered into a written referral agreement with Empower Advisory Group, LLC (“EAG”), through which Promoter will be paid for new leads through EAG. Promoter is not a client of EAG. Promoter is not affiliated with EAG or its affiliates and Promoter’s services consist solely of referrals of prospective clients.

No fees or other amounts will be charged to Personal Strategy clients, prospective clients, or any other clients of Promoter or EAG as a result of this arrangement. Investors should conduct their own research and seek advice before making investment decisions. For more information about EAG, refer to its Form ADV through the SEC’s website.

M1 Disclosure: This content is not a solicitation, is not endorsed by M1, and was not reviewed by M1; the opinions expressed are solely those of the authors and do not reflect M1’s views. Information presented is accurate as of the video posting date; for the most up-to-date information, please refer to m1.com. Before making any investment decisions, consult your personal investment, legal, and tax advisors, as this content is for informational purposes only and not intended as investment recommendations.