Investing Strategies For 40 Year Olds

Are you middle aged with nothing to show for your two decades of hard work?

Are you afraid you won’t have enough money to retire-ever?

“Reader question:

For someone who got a late start “investing”, what should that person look for in investments? A mix of high and low risk assets, or something more aggressive to make up for lost time?” by Little House in the Valley

Have you spent the last few decades living without much regard for retirement? If so, you are definitely not alone.

These questions by Little House echo many mid 30-40-and 50 year olds concerns. The media is filled with stories of 40 year olds who’ve been busy getting married, raising kids, paying the bills and living. Either there wasn’t enough money left for retirement saving or these folks just weren’t thinking about retirement.

Finally, realize there is hope for those over 40. Here is actionable advice about how to invest for retirement at age 40.

Whatever the reasons for not saving earlier for retirement, it’s not too late to start now, even if you are 40 years old. And if you’re 50, well; better late than never.

Don’t Worry About Retirement-Do Something About It!

Now isn’t the time to beat yourself up or let regrets tear you apart. Neither of those avenues will put dollars in your 401(k) account.

If you haven’t started investing by 40 or older, there’s still hope. You are probably earning more now than you did in your 20’s and maybe your expenses are even dropping a bit. Is your mortgage payment a smaller percent of your total income? Are the childcare expenses and college costs coming to an end? If so, now you can get down to investing in earnest.

Here’s How to Invest for Retirement at Age 40

Little House in the Valley asked if the older investor should go more aggressive to make up for lost time, or combine high and low risk investments.

Combine high and low risk investments.

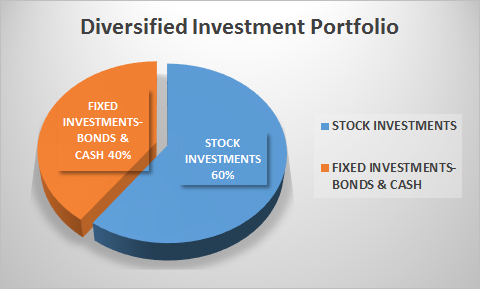

Most of us should combine high and low risk investments so that when the high risk (stocks and stock mutual funds) investments tank, we’ve got some bonds and lower risk investments to shore up our portfolio. If you’re 100 percent invested in stocks and the market falls 25 percent, which happens on occasion, then your $10,000 falls to $7,500. But if your portfolio holds 60 percent stock and 40 percent bond investments, then when the stocks fall 25 percent and the bonds hold steady at about 3 percent your overall portfolio decline will be moderated.

That 60 percent stock and 40 percent bond portfolio only drops 13.8 percent [(.60*-.25)+(.40 * .03)]. That’s much better than the 25 percent decline of the all stock portfolio!

By combining high and low risk assets in a 60 percent high risk and 40 percent low risk portfolio, during a market decline of 25 percent, your $10,000 portfolio only loses $1,380 and is worth $8,620. Compare that with a 100 percent risky stock portfolio. During a 25 percent stock market decline, the risky portfolio loses $2,500 and is worth $7,500.

By combining high and low risk assets, you reduce the overall volatility of your portfolio.

The downside of combining high and low risk investments is that when the market is going up, your high and low risk investment portfolio will increase less than an all risky portfolio.

Flip the situation around and during a 25 percent stock market increase, the all risky stock fund portfolio gains 25 percent. And the 60 – 40 percent stock and bond portfolio only rises 16.2 percent [(.60 * .25) + (.40 * .03)] . (Assumes a 3 percent return in bonds).

Should the Older Individual Invest More Aggressively (to make up for lost time)?

That depends.

How will you feel if you are 45 and your portfolio drops 25 or more percent? Will you be tempted to sell? An aggressively invested portfolio will decline more during market crashes.

Investors typically make bad decisions when they see their portfolio values decline.

Research shows that many investors panic and sell when the market falls (sell low) and then are afraid to get back in. Finally, when the market rebounds and returns to an upward trajectory these same investors buy back in (buy high).

It’s not a good idea to buy high and sell low. Yet the pain of watching your portfolio decline in value, especially when retirement is approaching causes this dysfunctional approach.

So, if you are certain that you can handle a large decline in the value of your portfolio without selling at the bottom, you might consider investing a bit more aggressively in your 40’s. Historical returns of the stock market hovers around 9 percent. But, be aware that the 9 percent average annual return comes with quite a bit of volatility. There’s also no guarantee that the stocks higher returns will continue in the future.

That said, the future is unknowable. Look at that crystal ball above, “Do you know if the stock market is going up or down?”

What is the Best Investing Approach for the Middle Aged Investor?

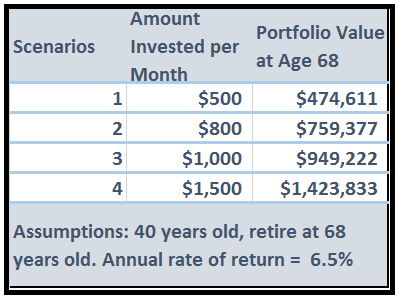

1. Save as much as you possibly can. A 25 year old can get away with saving and investing $300 per month. The older investor needs to find more money to put away and invest. Take a hard look at your income and expenses and figure out how much you can reasonably save every month. Below, you’ll see some figures demonstrating how much you need to invest in order to reach a specific amount by age 68.

With a projected 6.5 percent annualized return a 40 year old can have almost one million dollars by investing $1,000 per month for 28 years.

2. Invest in an asset allocation in line with your risk tolerance. Although we’ve used the example of 60 percent invested in stocks and 40 percent in bonds, it’s best to check out your own risk tolerance before setting up your asset allocation. To learn more about calculating your risk tolerance, complete the Sleep at Night Guide to Risk.

3. The research abounds that passive investing with index funds outperforms most active strategies. Propped up by the research of Nobel Prize winners such as Merton Miller, Daniel Kahneman, and William Sharpe, I recommend a very simple index fund approach to investing. Learn how to apply a passive index fund investing approach in the How to Invest and Outperform Most Active Mutual Fund Managers (a $10.99 value).

“…Any pension fund manager who doesn’t have the vast majority—and I mean 70% or 80% of his or her portfolio—in passive investments is guilty of malfeasance, nonfeasance or some other kind of bad feasance!”

— Merton Miller, “Investment Gurus,” Peter Tanous, February 1997

It is not too late to start investing for retirement, even if you’ve 40 or nearing 50. Start immediately and take advantage of Uncle Sam’s tax saving retirement vehicles such as the Roth IRA or the traditional IRA as well as your workplace 401(k).

Where are you on the retirement saving and investing path?

Click here for free Wealth Tips and 14 Rules of Investing free downloadable.