MBA Series – What Makes Asset Allocation So Important?

“Don’t put all of your eggs in one basket.”

The beginning of the year is portfolio rebalancing time for investors. I write a lot about investing as it is an achievable path to long-term wealth. If you don’t know what asset allocation is or much about investing at all, then this article is for you.

Modern Portfolio Theory is the science that drives most of the writing about investing today. As I put the finishing touches on the university Investments class I’m teaching, I’m going to share some of the basics with you.

Asset Allocation means selecting specific asset classes and choosing the percentage amount invested in each asset class. Sample asset classes are:

- U.S. Stocks

- U.S. Bonds

- International Stocks

- International Bonds

- Real Estate or REITs

- Government Bonds

- Small Cap Stocks

- Large Cap Stocks

- Government Bonds

- and more

Diversification – Tried and True Investing

Diversification in investing means don’t put all of your money in one investment or one type of investment.

Why?

When that investment goes down, there goes the value of your invested assets-down. And vice versa.

Buy different types of investments, so that when one goes down in price, the others may go up, or at least remain stable.

Diversification smooths out the ups and downs of the value of your investments.

For example, it is rare for bonds and stocks both to go down at the same time. During certain years, bonds will outperform stocks and others stocks outperform bonds.

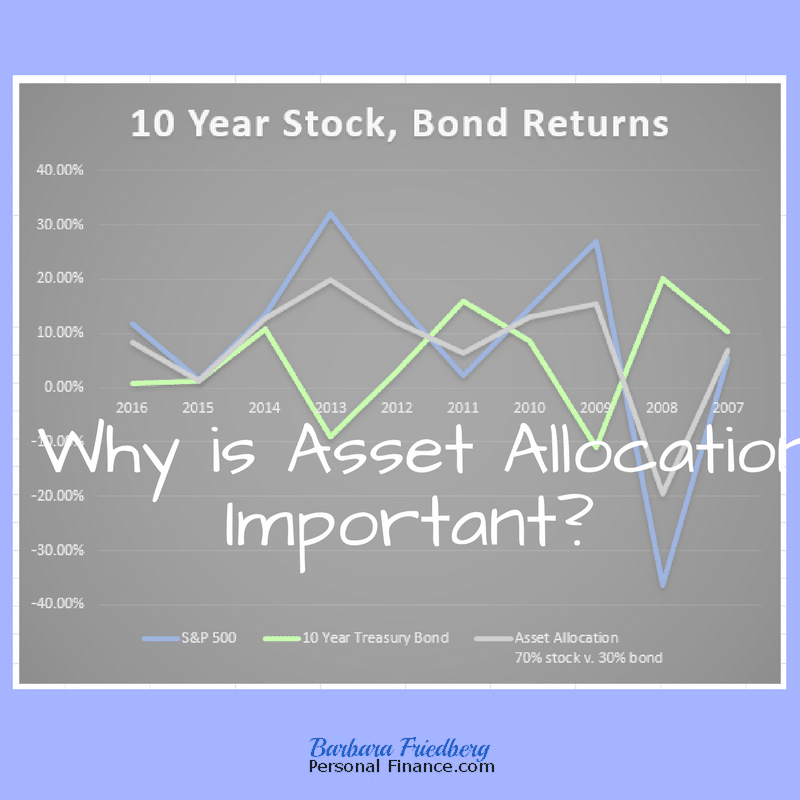

Take a look at returns of the S&P 500 stock market index in comparison with the returns of the 10 year Treasury bond during the previous 10 years.

Over long periods of time stocks have outperformed bonds, but a combination of both asset classes reduces your portfolio volatility (as measured by standard deviation). Notice that last year, the S&P 500, a proxy for the stock market averaged 11.74% return, while the 10 year Treasury bond returned a paltry 0.69%. Then, travel back in time to 2008 when the S&P 500 sunk a disastrous -36.55% and the 10 year Treasury bond enjoyed a 20.10% return.

With an all-stock portfolio, in 2016, you would have enjoyed an 11.74% return and a -36.55% decline in 2008. But, diversify a bit and the gain in 2016 wouldn’t have been as great, but neither would your losses have been as devastating in 2008.

Here’s Why Asset Allocation Is Important

Over the past 10 years, an all-stock portfolio would have earned an average 8.75% return, but with great volatility, as measured by the 18.74% standard deviation. Just think about how you might have felt in 2008 with a negative 36.55% return or in 2011 with a 2.10% stock market return while the 10 year Treasury bond advanced 16.04%.

Now, diversify with 70% of your money in stock market investments and 30% in bonds and over the past 10 years, you’d still have a respectable 7.63% return, but with a much tamer 10.87% standard deviation. You’re worst return year would still be painful, at -19.56% in 2008, but certainly better than the -36.55% drop.

Bonus: How to Build an Investment Asset Management Strategy >>>

Simple Portfolio Management for Successful Asset Allocation

The research abounds that a basic asset allocation of a certain percent in stock investments and a certain percent in bond investments has led to long term wealth creation.

As previously mentioned, there are all types of asset classes such as international stocks, country-specific stocks, small cap stocks, commodities, real estate, corporate bonds, government bonds, international bonds and more. All of these types of assets can be bought as individual holdings, or combined in mutual funds and exchange-traded funds (ETF). But, you don’t need to worry about the wide variety of asset classes unless you are passionate about investment management. You can obtain a satisfactory amount of diversification with just two ETFs or mutual funds.

For those DIY investors, seeking a simple two asset class investment portfolio, you’ll get sufficient diversification with part of your money in the Vanguard Total World Stock Index ETF (VT) and the remainder in the iShares Barclays Aggregate Bond Index ETF (AGG).

Index funds and ETFs are perfectly suited to a simple and effective portfolio management approach. The two asset portfolio shown in the chart above combines a world stock market index ETF with a total US bond fund. Depending on your age and risk tolerance, place more or less in each asset class.

With annual rebalancing to make sure the percentages in each asset class remain in alignment with your stated preference, you can grow your assets with little time spent in managing them. In other words, buy or sell from each holding to get back to the desired percentage amount invested in each fund. For a tutorial about How to Amass $787,355 with a Lazy Investment portfolio, click on the link.

For DIY investors, set a simple asset allocation to grow your wealth over time. There are even studies that suggest that a well-diversified asset allocation, rebalanced every year, will not only reduce volatility but increase your returns a small amount.

If you are not a DIY investor and want to pay a small fee for investment management, you might consider examining a robo-advisor comparison chart for help choosing a digital investment manager.

For those asset allocators out there, what is your asset allocation and why?

A version of this article was previously published.

1 thought on “Why is Asset Allocation Important? The Most Crucial Investment Concept”

nice article.thanks