“Investing should be dull,” according to Nobel Prize winning economist Paul Samuelson. “Investing should be more like watching paint dry or grass grow. If you want excitement, take $800 and go to Las Vegas”

Are you interested in a market beating approach with less volatility?

Do you want a set it and forget it investment plan?

Are you curious about a 3 fund portfolio that beat out “Yale U’s Unconventional” Lazy portfolio? (There’s more to this than meets the eye)

If you answered yes to any of those questions, then you must check out The Wall Street Journal, Marketwatch.com, Paul B. Farrell’s Lazy Portfolios.

5 Rules of a Lazy Investment Portfolio- Tips from “Build Your Own Lazy Portfolio”

These tips give you the “why” behind the Lazy Portfolio’s.

1. Be content as a singles hitter. Or, put another way, bet on every horse. Just buy the market through market matching index mutual funds.

In a study of 66,400 investors, behavioral finance professors Terry Odean (U.C. Berkley) and Brad Barber (U.C. Davis) found “The more you trade, the less you earn.” Stop looking for the “best trade” or the “big score”.

2. Avoid active trading and market timing. Compound returns will explode your wealth.

If you attempt to market time, you need to be right twice, once when you get into the markets and once when you get out. Are you really smart enough to know the perfect time to buy into the markets and the perfect time to sell? The most successful investors are not active traders.

Do you want to know how to be a singles hitting investment success? Click here

3. Save at least 10% of your income, so you smooth out your lifetime earnings. If you spend everything while you’re working, you’re relegating a quarter of your life (during retirement) to inadequate funding.

4. Trust compound returns. Time in the markets and compounding returns illustrate the miracle of wealth.

If you bought the first index fund in 1976 for $10,000 and didn’t sell it, then it would be worth $200,000 today, according to “Build Your Own Lazy Portfolio”. Not bad for doing nothing.

What Are Lazy Investment Portfolios?

Paul Farrell describes this “lazy portfolio” approach in his August 18, 2014 Marketwatch article, “Lazy Portfolio’s Grant Peace of Mind to 95 Million Investors”,

“Fifteen years ago we began tracking several successful portfolios that all had some common elements, as you can see on our MarketWatch Lazy Portfolio site. Although developed separately — by Nobel Prize winners and millionaires, portfolio managers and professors, grade-schoolers, professional economists and Main Street investors — they were all saying the same thing about how to invest.

Listen, here’s what we heard them say, follow these 10 guidelines, and your investment stress will drop, you’ll have more time to spend on stuff that’s really important, like family and friends, work you love, your returns will increase, and peace of mind increase. They’re a win-win set of easy-to-live-by secrets.”

Even if you’re a “go getter” and not at all “lazy”, this investment approach is worth a look. In fact, it’s a lot like the one I recommend in my FREE How to Invest and Outperform Most Active Mutual Fund Managers.

Each of the Eight lazy portfolios include various percentages allocated to unmanaged index mutual funds.

Bonus: How to Rebalance Your Asset Allocation Guide>>>

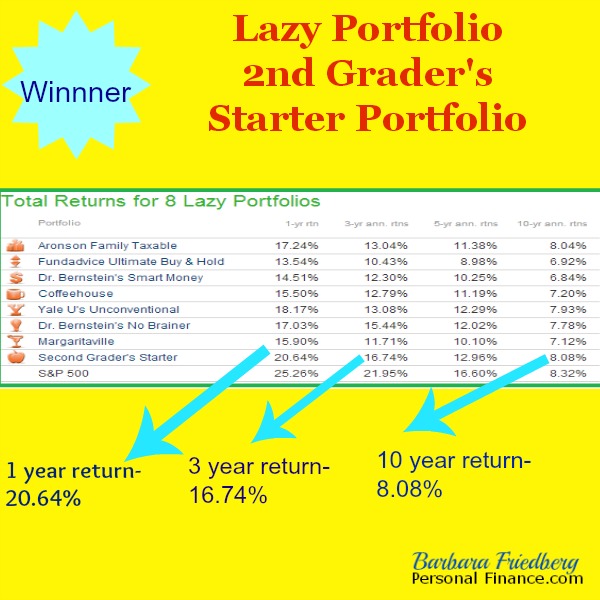

The Portfolio With the Greatest Number of Funds Is:

The portfolio with the greatest number of funds is The “Fundadvice Ultimate Buy and Hold” with 11 mutual funds in a wide variety of asset classes.

All of the funds in Paul Merriman’s Fundadvice portfolio are from the Vanguard family and include 6% allocations to Vanguards, Small-Cap Index, Small-Cap Value, Value, 500 Index, Emerging Markets, and REIT Index funds. He allocates 12% to Short-Term Treasury, International Value, Developed Markets Index funds. The largest allocation goes to Vanguards Intermediate-Term Treasury fund at 20%.

Notice that the Fundadvice Ultimate Buy and Hold portfolio has the lowest 1, 3, 5, and 10 year returns, in spite of holding the greatest number of funds.

But don’t jump to any conclusions yet.

The Portfolio With the Fewest Number of Funds Is:

The fund with the fewest number of funds was started by Kevin, an 8 year old second grader who began with a gift from grandma and advice from dad.

This overall winning 2nd Grader’s Starter portfolio holds 3 Vanguard funds in varying percentages. Sixty percent of the investment portfolio is in Vanguard’s Total Stock Market Index Fund. Thirty percent is allocated to the Vanguard Total International Stock Index Fund. Only 10% is invested in the Vanguard Total Bond Market Index Fund.

There’s a global difference between the Fundadvice and Second Grader’s portfolio, and it’s not the number of funds.

Can you figure out what it is?

How to Understand the Returns of the Lazy Portfolio’s

Before you conclude that a three fund portfolio is superior to a more diversified investment portfolio, there are a few important points to understand:

Asset allocation determines 90% of one’s investment returns. The 1986 article, “Determinants of Portfolio Performance,” by Brinson, Hood, and Beebower found that the percent of your assets devoted to various asset classes has more impact on your ultimate investment returns than the individual investments within each asset class.

Since the market trough and recession in 2008, stocks have enjoyed a tremendous bull run with returns averaging approximately 18% during the last few years. So it stands to reason that the portfolio with the greatest allocation to stocks during that period would outperform.

Asset Allocation Between Stocks and Bonds Explains (a lot) About Returns

The “Second Grader’s Portfolio”, held 90% of it’s total assets in stocks and only 10% in fixed bond investments. This is a very aggressive portfolio and best suited to a grade schooler with over 50 years until retirement.

This aggressive asset allocation, heavily weighted towards stock investments, is more likely to explain the portfolio’s out-performance than the portfolio construction of only 3 asset classes.

On the other hand, the 11 fund Merriman “Fundadvice Ultimate Buy and Hold Portfolio” was allocated more conservatively with 60% invested in stock funds and 40% in bond funds. This 60% stock and 40% fixed asset allocation is one of the most common asset allocations between stock and fixed assets.

It’s not surprising that during a period when stocks outperformed bonds significantly that a portfolio more heavily weighted towards stock investments would beat out one with a more balanced and conservative allocation.

The Lazy Portfolio Takeaways

In general, portfolios of unmanaged index funds will perform better than higher fee actively managed funds.

The allocation percentages between stock and bond (or fixed) asset classes is more likely to determine returns than the number of funds within an investment portfolio.

Returns will vary over time for each of the Lazy Portfolio’s (as well as your own investment portfolio) depending on market conditions.

Each of these portfolio’s offered excellent returns when compared with the unmanaged 100% stock S & P 500 index.

Click now to get a low cost plan to cut investment fees to the bone and manage your own investments.

In celebration of National Women’s Money Week #WMWeek17

What type of asset allocation do you prefer for your own investments?