Can You Predict Future Stock Market Returns?

Guest article by Rob Bennett

Have you ever tried your hand at predicting stock returns?

See what Rob Bennett has learned with his research about predicting stock returns.

I have been studying how to predict stock returns effectively for nine years. The purpose of this article is to put forward a brief summary of what I have learned.

1) Short-Term Predictions Never Work.

I do not believe that it is possible to predict where stock returns are going to be in six months or in a year or in two years. I have run into some smart people who disagree. What I can say with certainty is that, even if those people are right, it takes a lot of work to predict stock returns in the short-term; more work than most middle-class investors are willing to put to the task.

2) Long-Term Predictions Always Work.

We have 140 years of stock-return data available to us and a mountain of academic research reporting on that data. That research and that data shows that long-term predictions (predictions of where stock prices will be in 10 years or 20 years) always work if performed in a reasonable manner. This is the best-kept secret of stock investing. (Barb’s comment- No prediction, no matter it’s basis is 100% accurate.)

3) Investor Emotion Cannot Be Predicted.

There’s much more demand for predicting stock returns in the short-term than there is for long-term predictions. So, if there were some means of making effective short-term predictions, I would very much like to learn about them. However, I have come to the conclusion that short-term predictions will never work because the primary influence on stock prices in the short term is investor emotion. Emotion is by definition an irrational phenomena. So it cannot be predicted.

4) The Greater the Influence of the Economic Realities on Stock Prices, the More Predictable Returns Become.

The obvious question is — Given how hard it is to make good short-term predictions, how can it be that long-term predictions always work? I believe it is because investor emotion is not the primary influence on stock prices in the long term. After the passage of about 10 years, the economic realities become the dominant influence. The economic realities are known. And the economic realities are rational phenomena. So long-term predictions lend themselves to prediction by those willing to take the time to look up a few numbers.

5) It Is Far Easier to Make Effective Predictions Than Most People Imagine.

My guess is that most people don’t bother trying to make long-term predictions because they assume it would take a lot of work to pull them off. Nothing could be farther from the truth. Every factor that affects the price of a broad stock index is reflected in the price of that index. So you don’t need to worry about inflation or productivity or consumer confidence or anything else.

There’s only one exception to that general rule. Overvaluation and undervaluation are never reflected in the nominal (not adjusted for inflation) market price because these two factors are by definition indicative of mispricings. Look at the nominal price of an index, make an adjustment for the overvaluation or undervaluation that will be disappearing over the course of the next 10 years (it is an “Iron Law” of stock investing that prices are always in the process of reverting to the mean, according to Vanguard Founder John Bogle) and you have a ballpark number for where stock prices will stand in 10 years.

Barbara’s comment; As the average stock market returns during the past few years have been close to 20%, it’s not unreasonable to expect future stock market returns in the low single digits. Since the long term mean, or overage stock market return is approximately 9 percent and recent returns have been double the average, going forward it’s likely we’ll experience a few below average return years.

6) Long-Term Predictions Can Never Be Precise.

We know that from any valuation level stock prices will be headed in the direction of fair value over the course of the next 10 years. But that 10-year number will also be influenced to some extent by the investor emotion that is dominant at that time. Remember, investor emotion is never predictable. So we can never make precise return predictions, even in the long term.

7) Our Prediction Abilities Are Real But Limited.

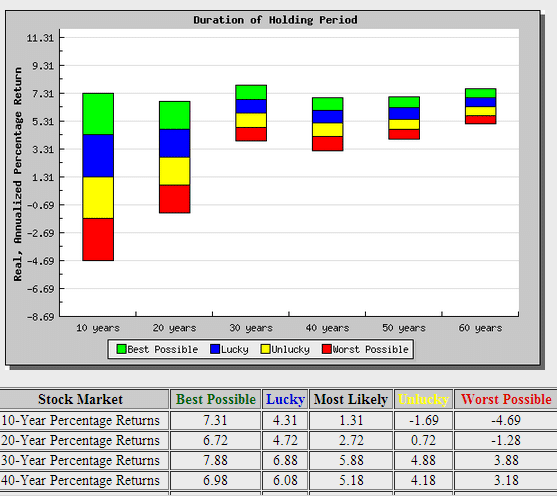

So what can we do? We can identify a range of possible returns that will apply in 10 years and assign rough probabilities to particular points along the range. For example, the P/E 10 value (the price of the S&P 500 over the average of its last 10 years of earnings) is today “26″ (SeptemberAugust, 2014). A regression analysis of the historical data from the stock-return predictor calculator, indicates the following future return probabilities:

Barbara’s update: According to Bennett’s Stock Return Predictor tool, during the next 20 years, the most likely “real’ (before inflation) stock market returs would be 2.72 percent with a best case scenario of 6.72 percent and a worst possible picture of -1.28 percent.

Since a real return doesn’t take into account inflation, you can tack on the average inflation rate of about 3.00 percent and see what the nominal return would be. Using an approximate nominal return, even the worst case 20 year return scenario, would be a positive return of 1.72 percent[3.00 + (-1.28)]. And the best case return for the upcoming 20 years would be 10.88 percent (including 3 percent inflation).

8) Knowing This Much Provides a Huge Edge.

The long-term benefit obtained by knowing this much is counter-intuitively large. Investors who change their stock allocations in response to big valuation shifts sooner or later nearly always go ahead of those who do not do so. The edge is often small. But that edge grows and grows over the years as a result of the magic of compounding returns. Over the course of an investing lifetime, investors who employ long-term predictions to inform their stock allocation choices can realistically expect to be able to retire five to ten years sooner than those investors who elect not to do so.

Rob Bennett often writes about stock market investment research and the tricky tricks used to trick you.

Chime in, do you think stock market returns are predictable or not?

A version of this article was previously published.