Why Contribute to a Health Savings Account?

A health savings account may be the best kept investing and health-related secret. Yes, you may use your HSA account for medical expenses. However, if used strategically, this account can also grow your wealth—tax free—and/or lower your taxes as you contribute. Plus, an HSA has magnificent investment potential.

How do HSA’s Work?

To take advantage of the power of an HSA, decide if you’re eligible to open an HSA. Next, learn the contribution limits and how to open an HSA. Then learn the tips to using your HSA to pay for medical expenses—or not.

What is an HSA-Eligible Plan?

First, determine if your health insurance is a HSA-eligible plan, such as a high deductible health plan (HDHP). This is a health insurance plan that meets the IRS guidelines (listed in publication 969) for deductibles, out-of-pocket expenses and acceptable coverage. The plan can’t provide benefits before meeting the deductible (except for preventative services), and co-payments must be included in the deductible and out-of-pocket limits.

If your plan is HSA-eligible then you can open an HSA account, as long as you meet the requirements for the last-month rule.

The HSA last-month rule allows individuals to contribute to the account as long as they are eligible on the first day of the last month of the tax year. So, if you sign up for a high deductible, HSA-eligible medical insurance plan on November 30th and are enrolled by December 1st, then you can contribute to an HSA account for that year.

How to Open a Health Savings Account?

If you’re eligible, open an HSA at any eligible provider either online or in person.

Make an HSA transfer from your savings or checking account into the new health savings account.

It’s fast and easy to complete the online application to open an HSA account!

What are the 2019 Contribution Limits for a Health Savings Account?

The annual 2019 HSA contribution limits are:

$3,500 for individual coverage

$7,000 for family coverage

After funding the HSA, you may invest in a cash account that earns interest or invest using a variety of options that might offer higher returns plus dividends.

The money in the account can be withdrawn at any time to pay for eligible medical expenses and for medical services such as acupuncture, chiropractic care and mental health to name a few.

Unlike a Flexible Spending Account, you don’t need to spend your HSA contributions annually. If you prefer, you can leave them in the account to grow and compound. You can also participate in an HSA rollover or HSA transfer if you have an existing account. This allows you to move into a new HSA without losing any of the tax advantages.

How to Use Your HSA

Once you set up the HSA you’ll need to understand how to pay for medical expenses with the money in your HSA account. There are several ways to handle your HSA reimbursement:

- Debit Card: Use the HSA debit card that comes with your account. This transfers money from the account directly to the medical provider. Remember to save receipts, to verify payments!

- Checks: Order checks from your HSA account and use them to pay for eligible medical expenses.

- Mobile payments: Link your debit card to your mobile wallet and at checkout, pay with your phone.

- Online Bill Pay: Like your standard bank account, you can set up your HSA Bank account for online bill pay and pay medical expenses directly from the account.

Can I Withdraw Money From my HSA for Non-medical Expenses?

Yes, you can withdraw money from your HSA for non-medical expenses and for any reason at all. But, there are costs to these withdrawals. If you’re under age 65, you’ll pay income taxes on the withdrawal, plus a 20% penalty. That’s a hefty price to pay if you’re under age 65, so exhaust other options before using your HSA account for non-medical expenses.

If you’re over age 65, you can withdraw HSA money for any reason. If used for non-medical expenses, you’ll pay income tax, but no penalty.

The best use of your HSA is to use it to pay for medical expenses and also to allow the funds to grow and compound tax-free for as long as possible.

Unlike IRA accounts, there is no required minimum distribution for an HSA account. This means that even if you don’t contribute to the account, the funds can remain in the account indefinitely. There’s no time limit for withdrawing HSA funds to be used for medical expenses.

What are the Advantages of a Health Savings Account?

As long as your funds remain in the account, they can grow and compound tax-free. Your money can then be invested in cash or potentially higher return stock and bond investment funds. In many cases, you can invest in the same assets that are available in an investment brokerage account, like TD Ameritrade or Schwab.

No taxes are due on any interest, capital gains or dividend payments for the funds within the account.

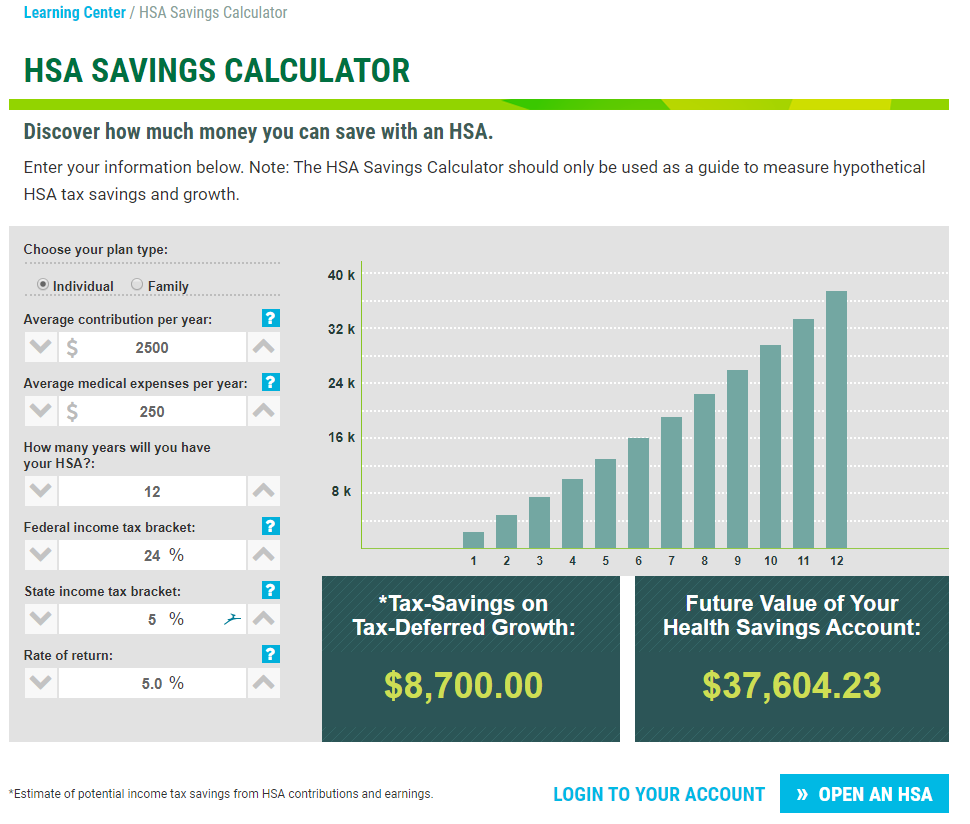

Source: HSA Bank Savings Calculator

The Wealth-Building Power of an HSA

An HSA Savings Calculator illustrates the wealth-building value of the account.

Consider this scenario:

- Contribute $2,500 annually to your HSA.

- Pay out $250 annually for medical expenses. Leave the remainder in the account, invested in cash, stock and bond funds.

- Assume that the money in the account earns a 5.0% return.

- Assume your federal and state tax brackets are 24% and 5% respectively.

- Own the HSA for 12 years and continue with the same pattern of contributions and withdrawals.

At the end of 12 year, your HSA is worth approximately $37,604 and your tax-savings is $8,700.*

Whether you use your HSA solely to pay for medical expenses or as an investment account as well, the benefits are excellent. If you’re eligible, there’s every reason to enroll in a HSA.

Take the Quiz and Learn Your Health and Wealth Score

The HSA account is almost magical in its health and wealth benefits. By cutting costs while taking charge of your health care spending you’ll benefit both financially and mentally.

Take a quick assessment to find out how you’re progressing on your Health and Wellness here: HSA Bank Health & Wellness Index Calculator.

Finally, taking a step to sign up for an HSA account to accompany your high deductible health insurance plan will propel your financial and mental well-being forward.

*This figure is an estimate.

This article is sponsored by HSA Bank.