The HSA Can Catapult Your Wealth

Several years ago, I was floored when my health insurance premiums topped $500. Oh, for the good old days. Last year, I paid over $700 per month. Recently, I gingerly opened next year’s health insurance estimate to discover that in 2019, I’ll pay more than $800 per month. And my health insurance plan has a deductible of thousands of dollars. Which means that before the health insurance company pays a reasonable percent of my health care expenses, I shell out thousands of dollars.

Here’s where the beauty of a Health Savings Account (HSA) comes in.

When my deductible hit the mid-four figures, I had to find a way to improve this expensive situation. And, I learned about the amazing Health Savings Account.

It’s an account with potentially huge tax benefits.

Here’s how an HSA works:

You open the account, just like you would open a savings account. At HSA Bank it takes about 10 minutes to open an account.

Next, you contribute money to the HSA, up to $3,500 for an individual and $7,000 for a family, in 2019 (with an extra $1,000 catch up contribution for those age 55 and older).

Then, you pay for any IRS-qualifying health expenses like:

- Acupuncture

- Doctor visits

- Prescription birth control pills

- Counseling

- Chiropractor

- Childbirth

- Crutches

- Dental treatment

- Dermatologist visits

- Special education tutoring

- Nursing home

- Hospital bills

- Hearing aids and batteries

- X-rays and more

So, you can use the HSA to pay for many medical-related expenses!

Unlike your Flexible Spending Account (FSA) at work, you don’t need to spend all the money each year. In fact, if you don’t exhaust the money in your HSA, the balance rolls over to the next year, and the next, indefinitely.

How do you Pay for IRS-Qualified Medical Expenses from Your HSA?

It is so easy. HSA Bank gives you a debit card that’s linked to your account. Just use it, like you would any other debit or credit card, to pay for your medical-related expenses.

Of course, you can go ‘old school’ with a paper check. And if you prefer, you can set up an electronic transfer to pay for reoccurring medical expenses.

Using your HSA is comparable to using your checking account.

How easy is that? But, wait, there’s more.

The HSA Contribution Silver Lining

In the year you make the contribution, you can deduct that same amount from your taxable income, if the contribution wasn’t already made tax-free through payroll deduction. That’s right, on page one of your 1040, line number 25, you list your HSA contribution. Then the amount of your HSA contribution is subtracted from your income and you don’t pay taxes on that amount!

That means, if you contribute $3,500 to your HSA and if you’re in the 24% tax bracket, your out-of-pocket expense is only $2,660, after factoring in the tax deduction!

But wait, there’s more, you can use your HSA as a powerful wealth-building tool.

Why I Love My HSA

I don’t have to pay for medical expenses out of my HSA, I can use it to grow my net worth! And, so can you.

I’ve taken to paying for my prescriptions and doctor’s visits out of my checking account, while my HSA money is invested and growing tax free!

You never need to spend the money in your HSA and it can be inherited by your beneficiaries.

In the beginning, I used my HSA in the typical way. I contributed the maximum to the account each year and deducted the contribution from my taxes. Then I’d pay for my co-pays at the doctors, my prescriptions and other medical expenses with my HSA debit card.

But, then I learned the secret that I’m going to share with you.

I want to legally shield as much money as possible from Uncle Sam and the HSA is the perfect way to do so.

I contribute the maximum into my account each year. Next, instead of keeping the money in the “cash” portion of the account, I invest it. (I leave some in cash for short-term medical expenses.)

Soon, you’re going to learn the magic of this investment strategy. But first, find out if you’re eligible to open an HSA.

Who’s Eligible for this Magical HSA?

By now, I’m sure you’re sold on the power of the HSA. After all, there’s no downside!

If you have a qualified High Deductible Health Plan (HDHP), you can open an HSA! You might have this type of health plan through your employer, your spouse, or like me, it could be one you’ve purchased on your own.

There are some caveats.

You can’t be covered by any other non-HSA-compatible health plan, including Medicare Parts A and B. You can’t be covered by a military insurance program, TriCare. Finally, you can’t be claimed as a dependent on another person’s tax return, unless it’s your spouse.

Now, let’s have some HSA fun!

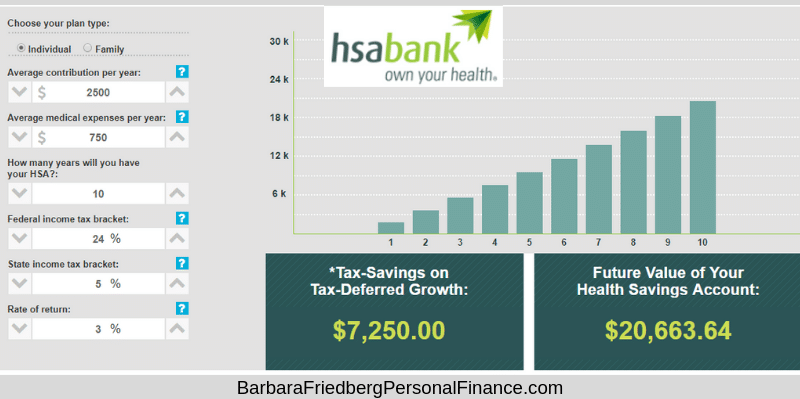

HSA Savings Calculator

Who doesn’t like to save money?

Play around with this HSA Savings Calculator to discover the magic of the account.

Let’s take a simple example and assume that you contribute $2,500 to your individual HSA for 10 years. And that your average medical expenses are $750. If you’re in the 24% federal and 5% state income tax brackets, find out how much you’ll amass within ten years.

With a 3% rate of return, the tax-deferred growth of your $7,250 contributions could grow to $20,663 after ten years.

If you transfer some of that money from the savings to the investment account, the return could grow your contributions even more.

If You Want to Invest Even More, Here’s How I’m Using My HSA

Remember, I contribute the greatest amount possible each year into my HSA. Next year, the maximum amount is $3,500 for individuals and $7,000 for families. Next, I choose a stock index fund and invest $3,000 per year in that fund. I project that over the next 20 years or so, as I continue to add the same amount annually, and earn approximately 7%, then my HSA could be worth approximately $131,600.

You’ll notice that I leave some cash available for medical expenses, too.

Now, at any time, I can sell the investments and use the money for health-related expenses. Or, I can let the funds stay invested and grow for retirement or to be inherited by my daughter! Distributions from your HSA that are used for qualified health care expenses are tax-free. Taxes, as well as an additional 20% tax may apply to non-qualified distributions.

(Just remember, don’t invest the money if you think you’ll use it within the next few years, as investing in the stock market is riskier than keeping the money in a cash account and the value of the account can go up and down.)

This article is sponsored by HSA Bank