Advice from a Newbie on Choosing a Financial Advisor

Guest contributor, Alexandra from Real Simple Finances

When it comes to investing, I feel pretty clueless. With all the options – even within a single category like mutual funds – out there, I’m completely lost! Barbara has some excellent advice for those of you looking to invest on your own – and I would recommend you read her investing articles – but I am here to talk to you about choosing someone else to do your investing for you.

This advice may not be comfortable to some people. I encourage you to do what is best for you and your situation; if you’re a do-it-yourself kind of person, by all means research investing and make your own decisions. Alexandra writes, for those of you like me, who are indecisive and have a hard time understanding some investing terms, read on.

Note: Before deciding on a financial advisor, you should first decide if you’re ready to invest.

Choosing an Advisor Basics

There are a few things to consider when choosing a financial advisor. Fees, qualifications, and length of time on the job are all very important factors. It should go without saying that you want to hire someone with a lot of experience and who won’t cost you too much in fees and expenses.

Advisors who are only paid only through commissions have a conflict of interest. If the only way the advisor gets paid is through commissions, they may feel compelled to buy and sell more than is necessary.

The Investment Answer by Dan Goldie and Gordon Murray (one of Barbara’s favorite investment books) has one of the best overviews of investment advisor’s designations.

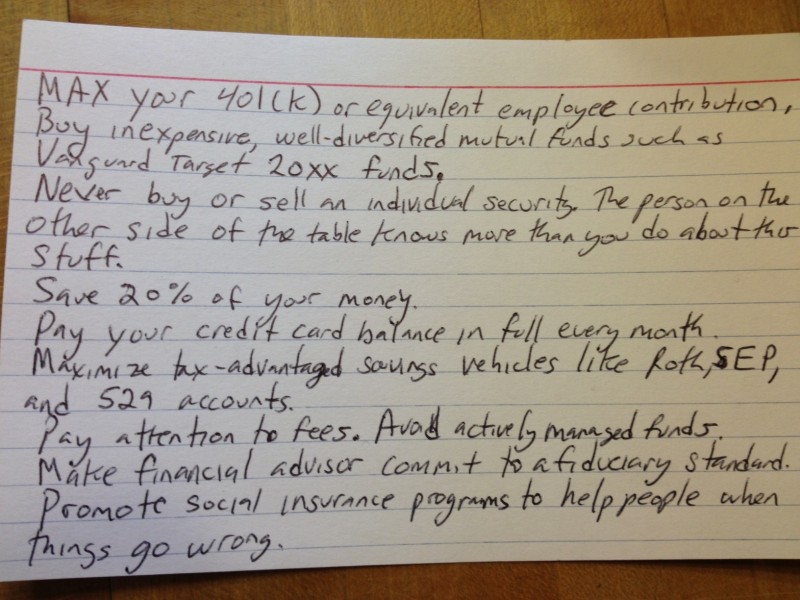

Find out if the advisor recommends index mutual funds and exchange traded funds. These popular investments have low fees and generally outperform most actively managed mutual funds.

Don’t rely on glossy charts of advisors “past performance”. As the disclaimer says, and research has proven, “past performance is not proof of future success”.

The Wall Street Journal writes about How to Choose an Advisor if you’d like to learn about advisor’s designations and how to run an advisor “background check”.

If you need help with your investments, we’ve partnered with WiserAdvisor to provide you with access to three vetted Financial Advisors – in your area. Click the image below to sign up. (no obligation when signing up)

When Choosing an Advisor, Look at the Personal Side too

Dig Under the Personality Hood of Advisors

1. Personality

Don’t judge me on this one, because I think it’s extremely important. I cannot work with someone who is rude and stuffy. You should build a relationship with your financial advisor. I want my relationship to be one that doesn’t make me anxious or irritated every time I interact with the advisor.

I also couldn’t work with someone who is too pushy. If I feel as though I’m dealing with a sales person – and believe me, I know they have to make money too – I’m going to feel a bit uneasy. I want to know that my advisor cares about me, and that he won’t push me into making decisions that will stuff his wallet, but not necessarily mine.

Make sure you understand the advisors training and background. Some advisors are glorified sales people with little or no background in financial concepts.

Bonus: What Net Worth Should I Have Before Hiring A Financial Advisor?

2. Ability to explain things

I already have a hard time with some investing concepts. I do not want to work with someone who cannot explain things to me when I’m confused. That being said, I also don’t want to feel like an idiot! If the financial advisor can’t speak to me in a simple way without treating me like I’m stupid, I’m out of there.

If you need help with your investments, we’ve partnered with WiserAdvisor to provide you with access to three vetted Financial Advisors – in your area. Click the image below to sign up. (no obligation when signing up)

3. Accessibility

How frequently can you get in touch with your advisor? Is he available only during typical business hours? I understand that not everyone is accessible 24-7, but having alternative ways to contact your advisor can be very helpful when you’re investing in a volatile stock!

4. Number of advisors in firm

When you are searching for an advisor, you should find out exactly who will be working with your money. Are you doing business with a one-man show? Are there multiple people involved in the decision-making process? Who can you contact if your advisor is sick or on vacation? Whether you want to work with one person or an entire firm is your own decision, but you should always know what Plan B is when something happens and your advisor is not available.

5. Investing options that match your personality

My advisor gave me a comprehensive sheet describing the types of investment he offers, complete with an “investing style” quiz. Based on my answers to the questions on the quiz, I get a certain “style” of investing, with some of my options. I already knew I was a conservative investor, yet it was interesting to see which areas I was more willing to be risky in. Your advisor should be able to offer you a wide range of services that allow you to set money aside in funds with varying risk.

If you need help with your investments, we’ve partnered with WiserAdvisor to provide you with access to three vetted Financial Advisors – in your area. Click the image below to sign up. (no obligation when signing up)

6. Your gut feeling

I’m a big fan of going with your gut feeling on certain things. When it comes to selecting someone to manage your money, you can’t place too little value on your intuition! If someone is making you uncomfortable, get out of there. There are many, many investors out there to help you, and the one you choose should make you feel comfortable and secure, and should have all your trust. After all, we’re not all rich enough to not feel fear at the thought of losing money!

Still have question? Check out the Chicago Financial Planner’s “6 Questions to Ask When Choosing a Financial Planner.”

Bio; Alexandra is the owner of Real Simple Finances, where she writes easy finances tips for real people. In addition to fighting off student loan debt, Alexandra is a university English Instructor and will be graduating in May, 2014, with her Master of Arts.

Barbara’s comments: I personally believe that most relatively intelligent investors can invest on their own. If not, check out fee only planners and be very careful with those who are paid solely by commission.

Have you visited a financial planner? What are your tips for choosing a financial advisor?

image credit; Washington Post article_card sourced from Pollack’s chat with Helaine Olen regarding the financial industry