My Savings CD Account Passbook & Links

I’m on a cleaning and purging binge. It boosts my personal wealth and well being to live in an environment free of clutter (well maybe not clutter free, but with less clutter). The more I focus on what matters most, the better life is.

In my obsessive purging I found some old bank records ready for the shredder.

Records from the late 1980’s and early 1990’s can easily be discarded so I tried to run the whole envelope through the shredder.

But the envelope was too thick to run through the shredder so I opened it up and found an old savings account passbook. For those born after the late 1980’s you may not realize that banks recorded your balance in a booklet, along with the interest rate.

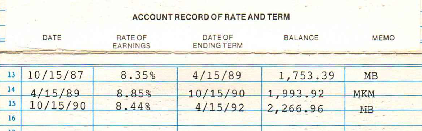

Here’s the record of a certificate of deposit from a Savings and Loan account :

I know 23+ years ago is a lifetime for some. But this CD savings account passbook was a reminder that the only constant in life is that things change.

Several decades ago, I would never have believed that savings rates could drop to below 1%.

Granted, inflation was much higher then. In fact, in 1989, inflation ranged from 4.3 to 5.4%. Yet, even with such high inflation rates, the real rate of return on that certificate of deposit was near 3% (that’s over 2% higher than today’s real rate of return).

The point of this information is to be aware that no one knows the future, and the past may or may not be indicative of what’s next.

Even at rock bottom interest rates, everyone needs some cash to access for emergencies, short term spending goals, and day to day expenses. Here are some articles about investing and where to put that short term cash.

Barbara Recommends-Fixed Income and Investing Links

Treasury Bills; A Smart Bet for Conservative Investors by The College Investor-With the stock markets increasing daily, it’s a good idea to attend to the fixed and cash portions of your portfolio. Along with I Bonds, Government Treasury Bills are not a bad idea for your cash. Learn about them here.

Doing the Math on an Online Savings Account by Joe Taxpayer-We all need some ready cash; for emergencies, short term goals; and walking around money. With interest rates in the sub basement, online bank accounts offer a less horrible interest rate. Why not

Asset Allocation of Bonds at Learn Bonds.com. This article delves into one of my favorite topics, asset allocation, and discusses how much of your portfolio should be in the fixed bonds category.

Consumption Smoothing and Your Financial Future at Financial Ramblings. Saving versus spending, the age old question. Just a reminder that we can’t have it all now. Or if we try, we won’t have much in the future.

3 Ways Your 401(k) Lowers Your Tax Bill at the White Coat Investor. As a long time contributor to any tax advantaged plan around, this article underscores why to invest as much as possible into your workplace retirement account. And if possible, invest in a Roth or Traditional IRA as well.

Safeguarding Your Asset Allocation at the Oblivious Investor. Stick with the asset allocation you decided upon and don’t do a lot of trading and rejiggering. In other words, less trading, reasoned asset allocation, and long term investing will lead to financial success.

Six Important Year End Portfolio Performance Must Dos at the Jemstep Blog. It’s that time again when investors review their portfolios, sell holdings to harvest the tax losses, and take actions to cut tax bills and maintain their portfolios. This article offers some handy reminders.

23 Financial Experts Share Their Best Investing Secrets at Investor Junkie. Investors with varying ranges of experience share their tips and secrets. Even if you think you know it all about investing, you might find a nugget to boost your wealth.

1%-A Small Number with Big Implications from The Chicago Financial Planner– Boost savings by 1% and notice the outsized impact of compounding. Time in the markets will compound your returns and even a 1% increase can yield a big return.

What is the highest return you have ever received on a cash investment? Today, where are you looking to boost your cash returns?