Modern Portfolio Theory in Practice

This week’s module in the MBA Investment’s class I’m teaching unpacks how diversification among various asset classes can increase the investor’s return and reduce risk. For the newbies out there, examples of asset classes are stocks, bonds, real estate, cash equivalents, commodities etc. The degree of correlation among asset classes is what leads to greater or lesser diversification benefits. If asset returns move in the same direction, for example, when fund A goes up 10% and fund B goes up 9.75% the funds are positively correlated. The more closely correlated the investment returns are, the less benefit the investor gets from diversification. The greatest diversification benefit comes when the asset classes are negatively correlated; one fund’s return goes up and the other fund’s return goes down thereby reducing risk and boosting returns.

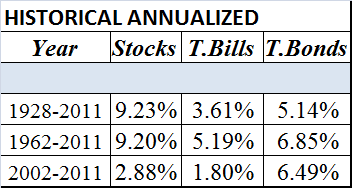

Historically, investors are advised to invest in U.S. and international assets because they are usually negatively correlated. Stock and bond returns typically exhibit less correlation between returns than those of stocks with other stocks. But here’s the problem, in times of economic upheaval and uncertainty, asset class correlation tends to increase. That leads to less diversification benefits from investing across asset classes.

If you assume that a diversified portfolio of US Stocks, International Stocks, Small Capitalization Stocks, and some Bonds will significantly increase returns and reduce volatility you may be surprised to learn, that recently the stock funds are quite highly correlated.

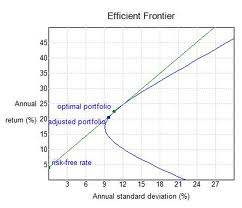

The Efficient Frontier

Harry Markowitz, founder of modern portfolio theory, developed the Efficient Frontier concept. This theory demonstrates that creating portfolios of less correlated assets and adjusting the weight of each asset can yield a portfolio which minimizes the total risk and maximizes total return. The frontier is based upon historical asset returns and standard deviations. The final step is adding a risk free asset like U.S. Treasury bills to the riskier options in order to boost return possibilities while minimizing volatility.

Sounds great, choose a bunch of seemingly uncorrelated asset classes, put them together in a portfolio, invest in appropriate weights so that returns are maximized and risk is minimized. Then throw in some risk free assets in line with your personal risk tolerance. And voila, you have the optimal portfolio.

When the Efficient Frontier Isn’t

What happens when historical returns and standard deviations used to create the model are not predictive of future standard deviations or asset class returns? What if the correlations between portfolio assets becomes higher? What happens if international investing doesn’t add any diversification benefit? What if small capitalization stocks and large capitalization stocks are highly correlated? Does that mean that there’s no benefit from diversification?

In order to demonstrate the concept of the efficient frontier I input (what I thought would be) 5 loosely correlated exchange traded funds (ETF):

- Vanguard Total Stock Market ETF (VTI)

- Vanguard Small Cap Index (VBR)

- I Shares TR MSCI EAFE Index (EFA)

- Vanguard Emerging Markets (VWO)

- iShares Barclays TIPS Bond (TIP)

The portfolio includes four equity index funds including a total US stock fund, a small cap US stock fund, a Europe, Asia, and Far East developed markets fund, and an emerging markets fund. The fifth fund was a US Treasury Inflation Protected Securities fund. I expected that the stock funds, which were varied in size and geography, to have lower correlation coefficients. (In other words, their returns would not move in lockstep). To my surprise, with the exception of the Government TIPS fund, all of the other stock funds were closely correlated. In fact the lowest correlation coefficient among the stock funds was .82 for the Emerging Markets (VWO) and the small cap index (VBR). That means when the emerging markets fund goes up or down 10 percent, the small cap index might only go up or down 8.2 percent. That’s not too much benefit from diversification.

In creating an optimal portfolio, I selected five years historical returns and standard deviations for the funds upon which to build the efficient frontier and put in a risk free rate of 2.1 percent. Since I do not want to include short selling*, I set the maximum weight for any one fund at 100 percent and the minimum weight at 0 percent. According to my stipulations, the optimal portfolio included only a 61.7 percent stake in the Total Stock Market ETF (VTI) and 38.4 percent in the TIPS fund (TIP). There was no allocation to the other three funds (when short selling was excluded).

The optimal weights for the best return for the least amount of risk with this five fund portfolio allowing short selling was 100 percent sold short in the EAFE index fund, and short selling 1.6 percent of the emerging market with positive percentages in the other three funds. In plain English, the optimal portfolio recommended by the efficient frontier model recommended borrowing shares in two funds and buying them back if the price decline, a very risky investment strategy (short selling).

What’s an Investor to do?

From my knowledge of economics and the current global scenario, I would expect that the European markets to rebound from their debt problems and exhibit better asset returns in the future. The efficient frontier calculation, based on the recent five years, takes into the account the poor performance of European assets during the economic downturn. But, it also assumes these international stock funds will continue to exhibit poor returns.

I would not predict this performance for the future. And that is what is wrong with the efficient frontier.

The efficient frontier model is based upon historical data, including returns and risk. There is no guarantee that the historical performance will continue into the future. The takeaway is this, do not put blind faith in any model. As I’ve said many times in the past, it smart to pick out an asset allocation you are comfortable with and stick with it until your personal situation changes. Make sure to throw in a bit of real estate and maybe even a smidgen of a commodities fund along with diversified bond and stock funds. Correlations between asset classes will change and the truth is we only know about the changes in hindsight. And why not add a bit more to the funds during cyclical downturns?

Even if assets become more correlated, diversification is the best tool we have to boost returns and minimize risk. Diversification isn’t perfect and doesn’t work seamlessly all the time, but it is better than putting all of your eggs in one basket.

*Short selling is the selling of a security that the seller does not own, or any sale that is completed by the delivery of a security borrowed by the seller. Short sellers assume that they will be able to buy the stock at a lower amount than the price at which they sold short. (Investopedia)

Thoughts? How is your portfolio allocated?

image credit: google images_investor craft