How to Retire Comfortably

FF at Feeling Financial asks:

What factors play the biggest role in whether or not I’ll retire comfortably? Is it the funds I pick, how much I save, or how often I rebalance?

Recently, when talking about budgeting with my Mom, she mentioned that she and my Dad never budgeted. That really surprised me. They were and still are very financially savvy. My dad came from an impoverished background and my mom’s upbringing was modest. My dad started working at age 10 to help out the family, managed to get out of high school in 3 years and college in 3 as well. Since their financially modest beginnings, they’ve done quite well.

They are my financial role models.

So how were my parents able to retire comfortably and end up financially secure without a budget?

For as long as I can remember, they balanced economy and spending. For example, next to the phone there were cut up sheets of paper for messages. Nothing was wasted; we darned our socks (Who does that anymore?), no food was wasted (‘Leftovers’ meals were on the menu at least once or twice a week), when we ate out, it was usually at a modest restaurant. We typically shopped at the outlet mall or bought clothes on sale. As a child, my (unlucky) younger sister wore my old clothes.

They never kept a budget because, they prioritized saving, and investing. They saved, before they spent.

Click this button to learn how to retire comfortably with investing.Mom and dad retired wealthier than they could have imagined. Their habits inspired my interest in investing. Learn from their financial success as well as my education and experience about how to make wise money choices today in order to retire comfortably tomorrow.

How to Retire Comfortably (or Wealthy) – Without Great Sacrifice

-

Start Early-Saving and Investing

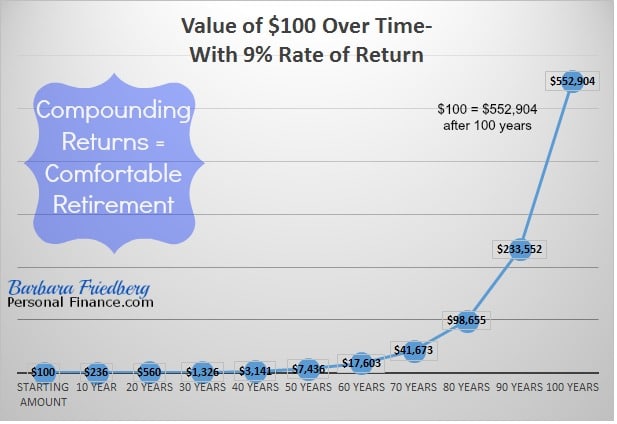

One of my MBA professors, Patrick Cusatis said anyone can be wealthy if they just have enough time. Check out this compounding example to see what he meant.

Start with $100. Invest the $100 in a diversified stock mutual fund. Reinvest all the dividends and capital gains. Assume that the $100 earns 9 percent returns, consistent with the historical stock market average annual growth.

After 100 years, that $100 is worth $522,904. And if you wanted the money earlier, you can see it’s value on the graph above. It’s crucial to understand that the greatest amount of compounding comes at the end of the time periods.

It’s hard to grasp that $100 invested in the U.S. stock market for 100 years would be worth more than half a million dollars a century later.

Length of time in the markets is the greatest indicator of compounding of returns and can be one the most reliable signs of whether you’ll retire comfortably.

What’s the practical application of this example? After all, very few people will live to age 100 and begin investing at age 1. But, imagine if you started putting away 10-15 percent of your salary into a retirement fund at age 25 and invested the monies into stock and bond mutual funds. At age 65 you would likely have a seven figure investment account.

Even if you started later, you can still build up a decent nest egg with consistent investing.

-

Develop smart lifetime spending habits. No matter how much you earn, if you don’t save and invest part of your earnings today, you’ll lack a secure future or comfortable retirement.

Although earning a large income is helpful for building wealth, it’s not crucial. There are many people that earn a lot of money-and spend it all.

By starting now and creating spending habits in line with what matters most, you’ll live a fulfilling life; during your working life and in retirement.

How do you do this? If you are one who thinks before you spend, and doesn’t do a lot of impulse shopping then you’re probably already spending smart. If you tell yourself, “I’m worth it, I can splurge” frequently, then you probably are spending more now than is helpful to create a comfortable retirement.

The best way to create smart spending habits is to plan, pause and think.

Plan what’s important to you. Since you don’t have unlimited money, you need to spend on what gives you the most value. I don’t care about cars one way or the other. They just aren’t important to me. So my car is a 1998 Isuzu Trooper. It has 124,000 miles on it and drives just fine. The insurance and maintenance costs are minimal. So, I don’t spend much money on my car (the second largest expense for most people). That way, I have more money to spend on things that are important to me.

One of the top articles on this site is about a guy who buys a new car every two years. The article talks about how this strategy is just fine-for him. Only you can decide what’s important and where to spend.

Pause before spending. And I’m not only referring to expensive items. Even $5.00 per day spent on coffee and snacks can turn into tens of thousands of dollars over the years. For snacks, soda, and coffee – bring coffee from home and keep sodas and snacks bought at the grocery in the car.

Certainly, pause before spending on big ticket items. In fact, it’s a good idea to institute a waiting period before making any large purchases.

Think about how you want your life to look-now and later. I think a lot about people living in the luxury apartment complex next door to our condominium. Many of these renters drive expensive cars. I ponder how they will be able to build wealth for the future if they’re shelling out up to $3,000 per month on rent and hundreds of dollars on car payments, maintenance, and insurance.

Think about how you want to spread out your earnings from your working years, to last your entire life.

-

Save and invest every pay period.

When investing, be consistent and sensible. Forget the fads, the lottery, and looking for the quick buck. Don’t worry about the guy you heard about who “struck it rich” with his invention. He’s likely one in a million.

Most of us need to work, save and invest to build wealth-the old fashioned way.

Have you heard about someone who’s lost a lot of weight quickly, and kept it off- those people are rare. Most people lose weight and keep it off by cutting calories and exercise.

The same goes for building money for a comfortable retirement. Start saving and investing early and keep it up over your working life. As you saw with the former compounding example, with enough time, in the financial markets, small amounts of money can turn into great sums.

What about the funds I pick, the amount of money I save, and how often I rebalance?

These factors are important. It’s better to choose low cost index funds, save as much as you can, and rebalance annually. But these aren’t the biggest contributors to a comfortable retirement.

To drill down a bit more into smart investing practice, click this button and check out Invest and Beat the Pros-Create and Manage a Successful Investment Portfolio.Don’t forget to learn from all of our reader questions and answers.