Can I Retire Early? Get the Answer

Big and even small regular expenses can sabotage a comfy retirement.

Are you curious about how decisions about car purchases and lattes, might affect plans for retirement?

Maybe you’ve never thought about the relationship between your new car and your retirement date.

Can I Retire Early? OnTrajectory Shows If You’re On Track for Retirement

What is OnTrajectory and How Can it Help Me?

OnTrajectory.com is a “fin-tech” startup helping you map your current and future financial journey. This platform gives you vivid illustrations of your income, expenses, and investments. After inputting some basic information, you gain an immediate sense of the path you’re on – whether it’s toward financial freedom, or financial disaster. (OnTrajectory is currently best suited for desktop and viewing on tablets, phone version will be available in the future.)

OnTrajectory’s Tool Is Easy to Use

Sign-up is quick and requires users to answer four simple questions about your financial situation. From the baseline of data, OnTrajectory estimates the arc of your possible financial future. Inputting additional data is just as easy, allowing users to see the interplay between their income, expenses and investments over time.

You can create multiple scenarios to find out how each one will impact your retirement lifestyle.

What about Required Minimum Distributions (RMDs) and IRA Early Withdrawal Rules?

OnTrajectory automatically enforces certain rules during retirement, such as RMDs (Required Minimum Distributions) and warns users if their plan violates pre-retirement rules, such as Early Withdrawal Penalties. To supplement the OnTrajectory graph, data is available so that users can see the math behind calculations.

‘Can I Retire Early?’ Answers All In One Place

On the internet today, you can find many tools focused on bits and pieces of your financial life such as monthly budget keepers, college/529 calculators, 401k and IRA growth trackers, and retirement number calculators.

But how do you answer the question ‘Can I retire early?’ and others such as:

- If I set aside this much for my kids’ college, do I jeopardize my retirement?

- Will I have enough socked away by the time the kids start college?

- What are the long term effects of making small changes in my spending now – and will those changes have a significant impact on a particular future purchase?

- If I sell my house and downsize, will that buy me a few years of early-retirement?

- How can I retire early at 55?

OnTrajectory brings many tools together into a single, interactive application. Users can tweak and experiment, create multiple scenarios, or use advanced analyses such as Monte Carlo or historical simulations. You can monitor and validate the growth of individual accounts, create future goals, or view a complete history of your progress – all for free.

Bonus; Amass $70,000 By Changing One Lifestyle Habit

Just recently they added the option to add in an ‘employer match’ for your 401k or 403b retirement contributions. This new feature allows you to count your company’s retirement plan contributions along with your own.

Let’s Look at a Few Retirement Scenarios…

Can I Retire Early if I Buy a Daily Latte?

Optimizing Your Money: Curious about the answer to ‘Can I retire early?’ question if you have your daily Starbucks?

Find out the long-term cost of a Starbucks venti latte each day. At $3.95 those venti lattes come to $27.65 per week – which is about $189k over a lifetime! (in today’s dollars assuming moderate 3% inflation and 5% tax-deferred growth on the savings). Spending $189,000 on coffee sounds pretty crazy, doesn’t it?

The graph above shows the trajectory of forgone wealth the latte is borrowing from your retirement. In other words, if instead of buying the $3.95 daily latte starting at age 25 you invested that money, it would grow to an astonishing $189,328 during your lifetime.

Even if you stopped buying the daily latte upon retirement, the value of that daily coffee habit is almost $100,000 at age 67.

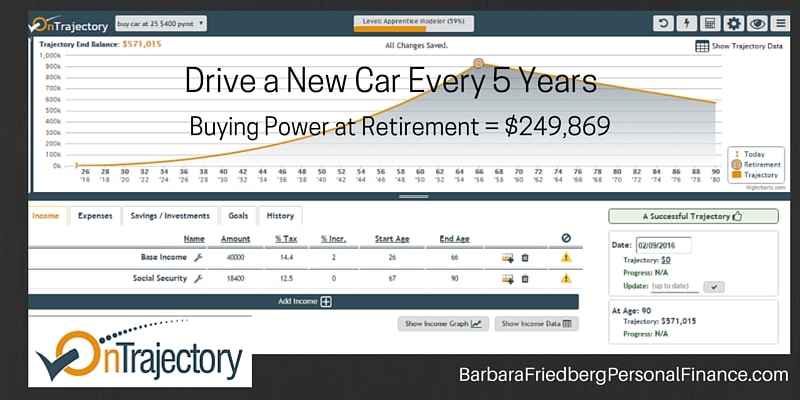

Can I Retire Early if I Drive a New Car?

Effects on Retirement: Curious about the answer to ‘Can I retire early?’ if you buy a new car every 5 years during your working life?

Are you curious about how car buying decisions, affect plans for retirement?

Let’s assume that you love your new car and don’t want to give it up! You replace your car about every 5 years (during your working life) – see how many retirement dollars are lost purchasing a car and paying a $400 per month car note. Or, if you prefer, the example works just as well if you spend $400 per month leasing a car during your working life. The final impact upon your retirement fund is the same.

Let’s look at the assumptions for Carlos, who loves his cars and must have a new model every 5 years:

- Age 26

- Income $40,000 per year (or $3,333 per month)

- Effective tax rate-13.75% per month

- General expenses-$2362 per month

- Car note-$400 per month

- Savings per month-3%-$100 per month (7% rate of return on Carlos’ investments during his working years and 4% rate of return in retirement)

- Employer 401k match of full 3% retirement contribution.

- Expect Carlos’ salary and expenses to increase at the rate of inflation.

Given those assumptions, Carlos will have a juicy $811,821 at retirement, even if he pays $400 every month for his new car. Although $811k sounds like a lot of money, if you factor in a reasonable inflation rate, that pot of cash will only buy what $248,869 will purchase today!

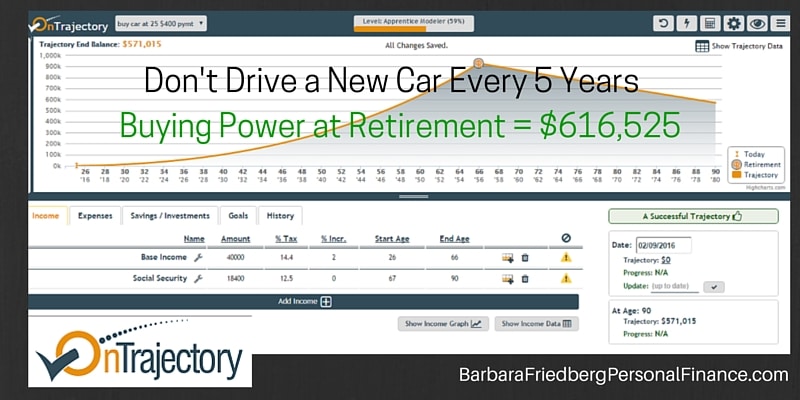

For comparison sake, let’s see how Carlo’s retirement plays out if we completely eliminate that $400 monthly car payment.

At age 66, Carlos now has $2,011,127 in retirement dollars , versus $811,821 if he pays $400 for a month for a vehicle. In the second scenario, his retirement money never runs out and he even has cash left to pass on to his heirs.

Realistically, it’s likely that during some of Carlo’s adult life he will have a car payment. But if he keeps his car longer and reduces his monthly car payment, you can see how much better off he’ll be in retirement.

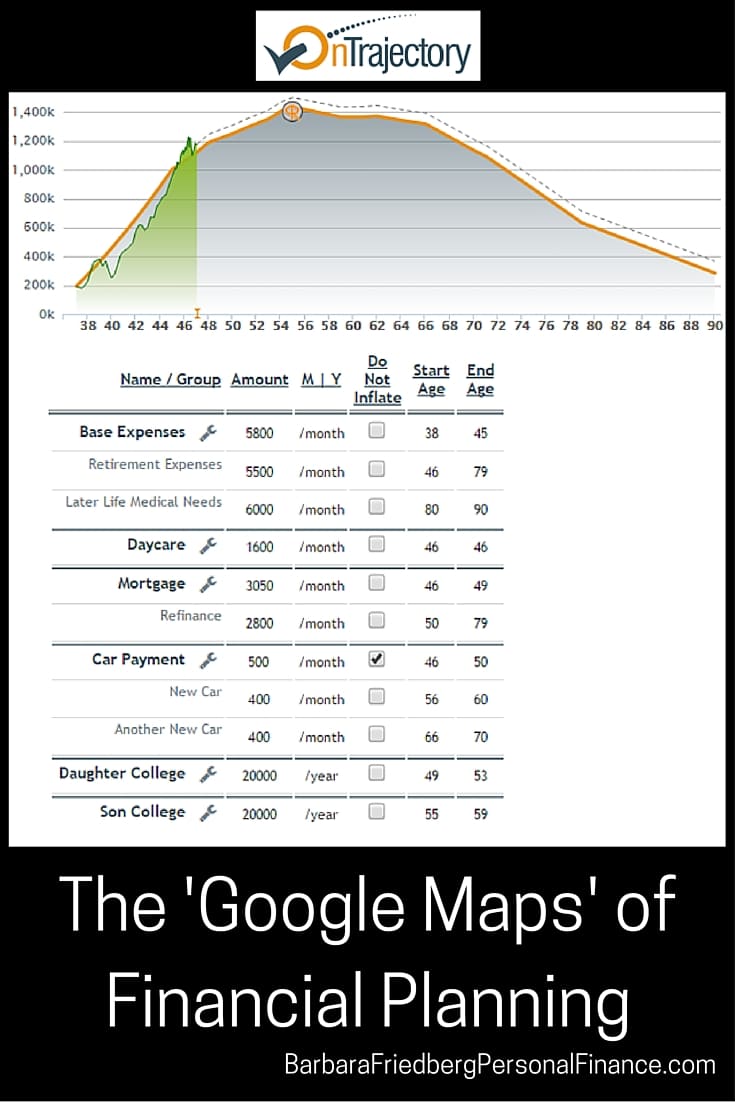

Bringing It All Together: As a final and more complete example of OnTrajectory’s potential, the picture below demonstrates the interplay between income / expenses / investments, and it shows how a whole-life view can help to make sense of it all. Wondering whether you can retire at age 55 instead of age 67?

With OnTrajectory, you can create many scenarios with varying amounts of income and expenses, all adjusted by year. The image below illustrates how one person’s changing expenses impacts his future retirement funds.

Newest OnTrajectory Features

The Home Equity tool helps you track the equity in your home over the life of your mortgage loan.

With the IRA Conversion feature – you can model the conversion of a Traditional IRA to a Roth IRA and see if it would be a long-term benefit to you.

Bonus offer: If you refer others to the OnTrajectory PowerPlan, you get fees waived for a certain time period.Not only can OnTrajectory aid in navigating difficult financial terrain, their blog and social media pages on Facebook, Twitter, and Google+ provide savings tips and financial modeling advice. The folks at OnTrajectory believe a solid financial education helps remove fear from one’s financial journey – and with their map in hand, anyone can reach the destination we all seek: living happily and financially secure.