“I would like your opinion and advice on how to pick mutual funds. I’m choosing mutual funds for my investments and my daughter’s investments among mutual funds. Both our accounts are with Fidelity. I am 56 and plan to retire at 60. I have $400,000 in IRAs (Traditional and Roth). My daughter is 24 and has $65,000 in an individual acct and $50,000 in both Roth and rollover IRA. There are so many funds to choose from and I feel overwhelmed. Any suggestions for which mutual funds to invest in would be helpful.”

John

When Choosing Mutual Funds, More Information Isn’t Always Better

There is scientific evidence that it is more difficult to make a decision when confronted with a large number of choices, than when given just a few choices. The Paradox of Choice, one of my favorite books, is devoted to this topic. The author, Barry Schwartz claims that we are paralyzed by too many choices, and that this paralysis leads to inaction. I think this is particularly true when it comes to investing in mutual funds.

Did you know there are more individual mutual funds than individual stocks?

How is someone able to decide among the over abundance of fund offerings?

Make investing simple and learn how to choose mutual funds by defining your risk level, financial goals and learning to buy the right funds.

What is a Mutual Fund?

A mutual fund is a type of investment vehicle where many contribute their money and the fund managers buy one or more types of investment assets. These financial assets might include bonds, stocks, commodities, currencies or other types of investments. The mutual fund is managed by an individual portfolio manager or group who abide by a particular strategy.

Mutual fund categories include passive and actively managed offers. Some mutual funds copy the investments that are owned in a particular index like the S&P 500, Nasdaq 100, government bond, or corporate bond indices. These passively managed funds are comprised of index funds where portfolio managers attempt to match the returns of their underlying indices. Actively managed funds choose another strategy in an effort to beat the market returns.

Mutual funds are similar to exchange traded funds or ETFs. Although both invest in similar assets, mutual funds are priced only at the end of the day and do not trade throughout the day like ETFs.

When investing in mutual funds, it’s important to match your financial objectives and risk tolerance with the fund’s investment strategy. You also need to consider the fund’s expense ratio.

It’s likely that John and his daughter will have distinct financial goals and risk tolerance levels.

Determine Your Risk Level and Investment Objectives

Before considering how many and what type of funds to choose, you must figure out how much volatility or risk you can stomach. Those who cannot sleep when their investment portfolio goes up and down, should have less invested in stock investments and more in fixed or bond type investments. Additionally, younger folks, with more time until they need their money are able to invest more aggressively.

Stocks and stock mutual funds are quite volatile and over the short term (which can be up to five years) go up or down in value. Over periods of more than ten or twenty years, their normal trajectory for stock prices is upward.

It’s risky to invest money in the stock market which you will need within the next five years.

Bonds are less volatile, yet long term historical data suggests that they offer lower levels of return than stocks.

In general, if you are close to retirement and cautious about risk you should have a more conservative portfolio with a larger percentage of your money in bond funds, CDs, and money market funds and less in stock mutual funds.

John’s 24 year old daughter has a long working life ahead of her, time to make up any investment losses and should think about investing more aggressively, especially in her IRAs. His daughter can afford to invest with a greater percent allocated to stock mutual funds, because, she has decades to make up any losses.

Many financial professionals recommend that those younger than 40, who are saving for retirement should allocate up to 90% of their investment dollars into stock funds. I’ve never been that aggressive, yet, probably should have been.

Had I invested more heavily in stock funds in my younger years, my net worth would be greater today.

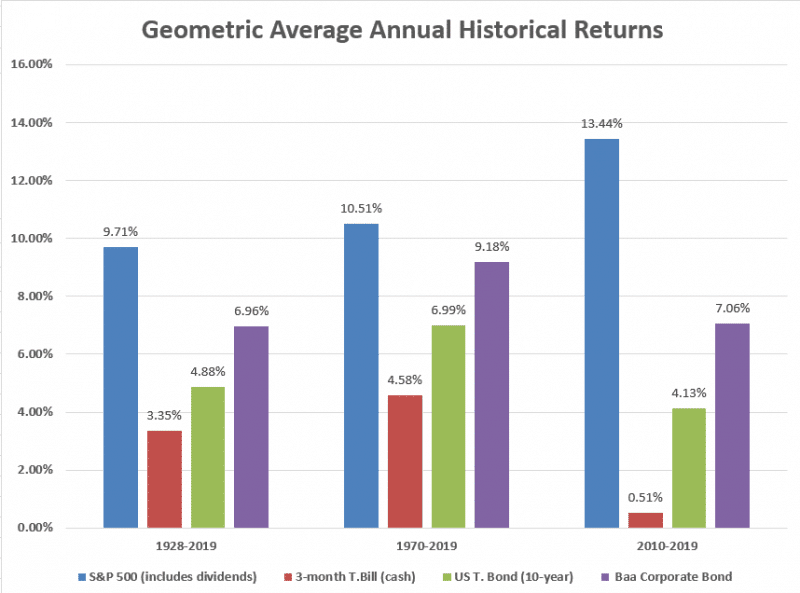

The most important factors in investment wealth building are to pick an asset allocation and stay invested through thick and thin. This chart of historical returns illustrates that long term asset performance is generally positive.

Following are the historical returns for a variety of investment assets. The higher the return, the greater potential for short term loses.

Historical Returns for Various Asset Classes

The S&P 500 represents the performance of the stock market.

The 3-month T bill represents the performance of cash-like assets.

The US T bond represents the performance of 10 treasury or governement bonds.

The Baa corporate bond represents medium-credit risk investment grade bonds.

So now that you have the asset allocation basics, on to which funds to choose.

Which Mutual Funds to Choose?

When choosing mutual or exchange traded funds (ETFs) narrow your universe first. The performance research is abundantly clear, passive index fund investing outperforms actively managed funds roughly 70% of the time. Even if a fund manager beats the returns of a passively managed index fund one year, it’s unlikely that she or he will outperform index returns in the long term.

So, your first mutual fund selection activity is to concentrate on passively managed index funds.

Expense ratios are also lower in passively managed index funds, leaving more of your money to go into the investment markets and less into the fund managers pocket’s.

Many of the investment brokers offer offer commission free index ETFs and mutual funds.

Check out the fees of the funds and strive for a reasonable level of diversification.

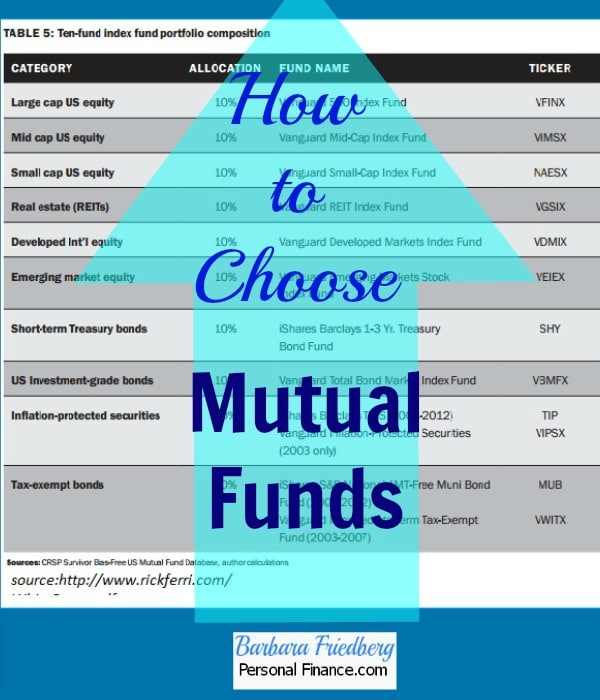

Here’s my Friedberg Family Portfolio. The majority of our funds are passively managed index funds. We own a few individual stocks and actively managed funds in our 401ks.

Actually, choosing a mutual fund is a much easier task than you would think. You only need a few index funds to have an optimal portfolio.

Since John’s accounts are at Fidelity, I’ve included some Exchange Traded Funds (ETFs) which can be bought commission free at Fidelity. Most of these funds and ETF’s are generic index funds with low expense ratios.

For more investment ideas read: My Best Lazy Investment Portfolio

Mutual Fund Alternatives – ETFs

If you’re investing within a 401k or 403b retirement account, there might be a limited selection of funds. But within a self-directed IRA or taxable brokerage account, there are many passively managed ETFs with lower expense ratios than their comparable mutual funds. So, don’t limit yourself to mutual funds, but consider ETFs as well.

Following are sample Mutual and exchange traded index funds from a variety of families.

Invest in Mutual Funds and ETFs from Diverse Categories

Total U.S. Stock Market Index Fund

- Vanguard Total Stock Market Index Fund (VTSMX)-Fidelity charges a fee to buy this mutual fund

- Russell 3000 Index Fund (IWV)- Exchange Traded Fund with no commissions from Fidelity

International Index Fund

- Fidelity Spartan International Index Fund (FSIIX)

Bond Index Fund

- Vanguard Total Bond Market Index Fund (VBMFX)-Fidelity charges a fee to buy this mutual fund.

- Barclays Aggregate Bond Fund (AGG)-Exchange Traded Fund with no commissions from Fidelity

If you want to get fancy, you can diversify a bit more with a real estate investment trust (REIT) fund. Or, you might consider a mid-cap or small-cap equity index fund.

Target date funds are also viable as they provide a diversified portfolio within one investment. You choose your expected retirement date (or the date when you’ll need the funds) and the portfolio becomes more conservative as that date approaches. Most fund families offer a target date fund or asset allocation fund.

The percentages you invest in each fund depend on your risk tolerance and preferred asset allocation. To learn more, read this free microbook, How to Invest and Outperform Most Active Mutual Fund Managers ($10.99 value). There are sections on determining your risk tolerance and asset allocation.

Although no one knows what the future holds, if history is any guide and if you believe the USA and world economies will continue to prosper, your investments will increase in value over time.

Related

Little Known Investing Secrets – How to Buy Low

Why You Should Invest in Index Funds

What are Index Funds and Asset Classes Investing?

10 Steps to Take Before Investing

Caveat; This article will touch on the topics to consider when choosing mutual funds. Please do not take this as personal advice for your individual situation. There are many considerations when planning an investment portfolio. For any specific investing information, please contact your own investment advisor or CPA. Fidelity and other investment companies have advisors on staff that can help with investment questions as well. Personal disclosure-I have an account at Fidelity.