The Stock Market Returns are Volatile

Early 2022 has been a rocky ride for investors. After an S&P 500 26.89% gain in 2021, year to date returns are a loss of -12.26% as of March 21, 2022. While not quite an official bear market, it’s enough to give investors pause.

If you’ve only been investing for a few years, you might think that markets only go up. And if they fall, they rebound very quickly. That short-term view, hides the long term ups and downs of investment markets.

In December 2015, the Fed Funds interest rate was 0.25%. From 2005 to 2015, the S&P 500 annualized stock market return was 7.60%, well below the 9.0% long term stock market returns.

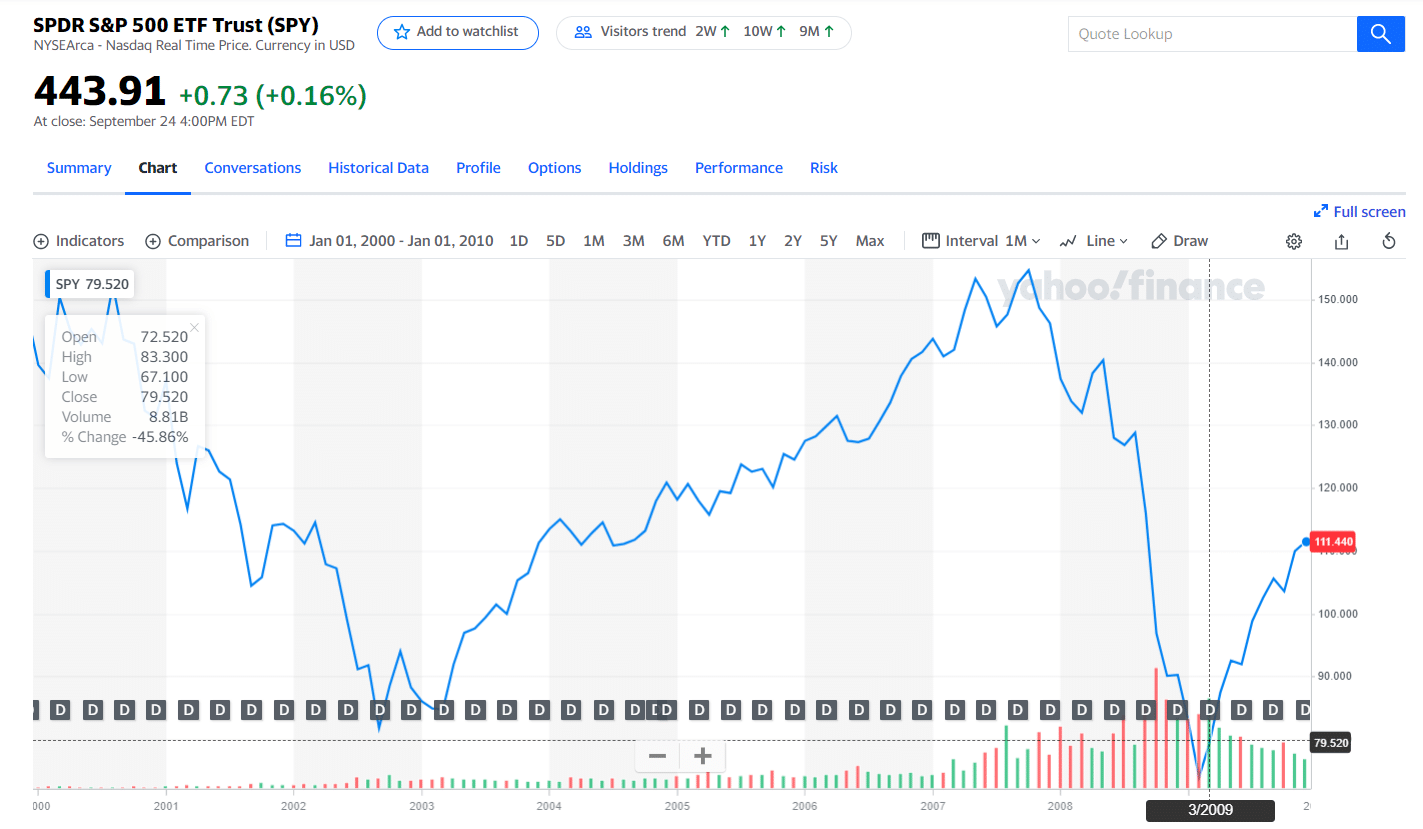

While, during the first decade of the millennium, the stock market lost value. The market reacted to the the frothy technology stock bubble of the late 1990’s by crashing for a few years and then reached new highs in 2007, only to crash again from another mania, the easy money of the housing boom. The mortgage debt crisis followed and crashed the market again.

After the 2007 peak, stocks declined and ended the decade lower than they began.

Global events that impacted stock market prices during the first ten years of the century:

- Recession

- Mortgage Meltdown

- Sub Prime Lending Crisis

- European Debt Crisis

- The 9 September 11, 2001 terror attacks

- Wars in the middle east

- Growth of China as a major world competitor

There are always outside forces that play on our economy and investment returns. These forces are called systematic or market risks. These risks are unavoidable and plague nearly all market participants. No matter how diversified your portfolio is, you cannot avoid systematic market risk.

Read more; Is Buy and Hold Finished?>>>

Just 7 years later, the S&P 500 returns look quite different. On February 4, 2022, SPY the SPDR S&P 500 Investment Trust ETF is valued at $450.46. Compare that with the $145.44 value on January 3, 2000. But, as the chart below reflects, the tripling of the S&P 500 ETF wasn’t a smooth ride. In fact, the most extreme growth occurred after 2015.

Since 1928, the stock market earned an average annual return of approximately 9% to 10% . You might assume that rates went smoothly upward. Actually, that average hides a bumpy road. Returns on stocks over that time period ranged from annual double digit losses to annual double digit gains. Growth in investing is fraught with ups and downs – similar to life itself.

Is There a Pattern to Economic Growth and What it Means for You?

Economic growth typically follows a path that looks a bit like a roller coaster, with gradual increases, leading to a high point of strong economic growth, followed by slowing GDP and usually a recession. This type of growth is certain, where the mystery comes in is the “when”. Cyclical growth is certain; but when the trend changes is unknown.

Even after a 5% pullback in the S&P in January 2022, we don’t know if the trend will continue, or reverse.

The cyclical pattern of investment markets means several things for investors:

- Investing is a long term endeavor.

- Don’t even think about investing any money in the stock market that you will need within the next 5 years.

- Stock market returns are too volatile for short-term investing.

- Knowledge of market behavior will help you stay the course during market fluctuations.

Once you understand that the ups and downs in the economy and investment returns are normal occurrences, you can expect periodic market declines. In fact, expect that every few years, there will be a year with negative stock and/or bond returns.

Accept the market cycles and you can benefit from cyclical investment markets.

What Factors Could Impact Stock Prices?

In 2021, we were uncharted waters, with massive returns. Here are current economic and political factors that could impact future stock prices:

- Covid 19 Pandemic – Variants and regulations continue.

- Russian invasion into Ukraine.

- Supply Chain Constraints – Commerce is experiencing shortages and the inability to obtain needed consumer goods.

- Increasing inflation – As inflation increases, so do consumer prices.

- Higher interest rates – Can lead to slowing economic growth.

- China’s economic issues – Including exploding debt levels.

- Overvalued stock prices – Stock valuations (as measured by the Shiller PE) are double historic levels.

How to Profit From Cyclical Investment Markets

The future is unknowable and it’s important to be prepared for potential market outcomes. Although there are technical traders that jump in and out of markets. Many studies have shown it’s very difficult to consistently predict stock market movements.

Here is a simple plan to stay the course and maintain your investment strategy during volatile markets.

1. Choose an asset allocation you can live with.

2. Select diversified low cost index funds from a range of asset classes for your investment portfolio.

3. Contribute regularly to your investment account during market ups and downs. In fact, contributing assets in a declining market yields the greatest rewards.

4. After a financial market decline, don’t sell – consider buying more. As long as global businesses continue to grow, so will your investment dollars.

5. Be patient. Despite the promises of fast profits, in the long run, the patient investor typically wins.

4. Regular investing over time yields great rewards. Invest $4,000 per year from ages 25 to 65 in a diversified investment portfolio with 7.6% average annual return and retire with $1 million.

5. Keep money needed for short term expenses in conservative cash and short term bond investments.

Accept the ups and downs in the market as a reality and profit.

Related

How To Invest And Make Money Daily

Use The Premortem To Prevent Investing Mistakes

Investing And The Fed | How Will My Investments Be Impacted?

Conservative Options Strategies | Boost Your Investment Returns

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t personally believe is valuable.

Empower Advisors Corporation (“PCAC”) compensates Wealth Media, LLC. (“Company”) for new leads. Wealth Media is not an investment client of PCAC.