Is Stock Market Going to Crash?

Investors in the stock market have benefited from the recent Federal Reserve Bank’s low interest rate monetary policy. The years of quantitative easing were the Federal Reserve Bank’s efforts to stimulate the economy, encourage banks to lend, consumers to borrow, and employers to grow their businesses. The goal was for employers to hire more workers and reduce unemployment levels.

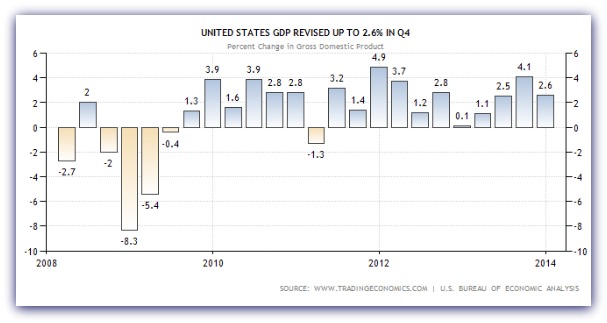

Since January 2010, the US economy, as measured by the Gross Domestic Product (GDP), reversed its negative trend and has been growing steadily. It seems as though the quantitative easing helped the economy grow.

So the economy is going in the right direction, why worry?

The quantitative easing is slowing down and interest rates will begin to increase. Investors are getting scared.

Here’s some help in understanding the current economic picture and suggestions on how to go forward.

Take a look at recent headlines:

“Nasdaq Closes Below 4000, As Stocks Fall” WSJ.com

“Producer Prices Rise 0.5%; But It’s Too Soon to Say Whether Pickup Augurs an Inflation Increase”, WSJ.com.

CNN Money reports: “Stocks: Heading for the Exits”

Just as low interest rates promote economic growth, higher interest rates can stall growth. Growing sales and earnings propel stock prices upward, whereas slowing growth sends market prices south.

After several years of positive stock market returns, its normal for stocks to take a breather.

So If the Economy is Improving, Why is the Stock Market Falling?

Investors fear slowing growth and as the U.S. stock market is a leading economic indicator, when there’s a sign of rising rates, investors get scared and sell, pushing stock prices down.

Although the economic growth is clear, the economy is improving, albeit at a moderate pace, the headlines tell a story of fear and apprehension. The headlines underline investors’ tendency to panic and run at the first signs of higher interest rates.

What Will Happen to Stock Prices When Interest Rates Rise?

Given the fact that at some point in the future the Federal Reserve will raise interest rates and will stop completely the $85 billion per month bond-buying program, how should investors prepare?

What should investors do?

Will the markets crash?

I know for a fact that no one can predict the future. I also know that at some time in the future, stock market prices will continue to decline and they will also go back up. That is the nature of the investment markets. They go up and down. Over decades, the direction of stock prices has been up, but there is no guarantee that the future stock market performance will replicate the past.

If you want to be certain that you avoid any future downturn in investment markets, you can sell all of your stock investments now (which I do not recommend). Then you will avoid any future losses. Or will you?

Devil’s Advocate Position; Sell All of Your Stocks Now (I do not recommend this position)

Here’s the outcome if you sell now.

- You will miss any future upward price movement in the stock market.

- Even if the stock market is overvalued right now (although I believe it is fairly valued), it can stay overvalued for a long time.

- If inflation kicks up, your uninvested cash will lose purchasing power and be worth less.

- You may miss further losses in the stock market, but how will you know when to get back in?

- If you sell now, you need to be right twice, first, when you sell, and second, when to buy back in.

Does this mean I’m telling you not to sell?

Not necessarily.

Should I Sell All My Stocks Now Because When Interest Rates Rise Stock Prices May Fall Further?

I cannot answer this question for you. If you hate to lose any money, then you shouldn’t be invested in the stock market at all. Stock investing is risky and values go up and down. Following is stock market data from the past. The difficult part of investing is that although there is an abundance of historical data, no one has developed the sure fire method of predicting the future.

Growth of $1.00 from 1926-2000

In 1926, invest $1.00 in the U.S. Stock Market.

In 2000, that dollar grows to $2,285.00. That’s right, your one dollar, invested for 74 years, increased over 10 percent per year.

Let’s assume that you were the worst investor ever and traded in and out of the market. And your trading caused you to be out of the market during the best 37 months of that 74 year period. In 2000, instead of $2,285.00 your $1.00 investment is worth $17.42. That’s correct, miss the best performing 3 years and the $1.00 investment is worth $17.42 for a 3.9 percent return.

If you are investing for retirement, or goals far in the future, and you want an opportunity for growth and can tolerate a few down years along the way, then consider stock market investing. If you need your money in the next 5 to 7 years, it should not be in the stock market! Stock market returns are way too volatile in the short run.

Any money needed in the next 5 to 7 years should be in a Government Inflation Protected (I Bond) Bond, savings account, or money market mutual fund.

When interest rates rise, it is possible stock market returns may fall further. It is up to you to decide whether to stay the course or panic and flee.

What happens when the Fed exits from stimulus? We are quite certain interest rates will rise, and it’s likely we’ll see a tic up in the inflation rate. Yet, students of market history know that there are always events which cause markets to go up and down, and picking the right time to get in and out is quite difficult.

I’m sticking with my predetermined asset allocation, and if the market continues to fall, I expect to boost my investing a bit and capitalize on the lower prices.

What are your current and future investing plans?

Are you worried about a decline in your investments? Are you considering selling any investments now?

A version of this article was previously published and comments remain intact.

How To Profit From Cyclical Investment Markets?