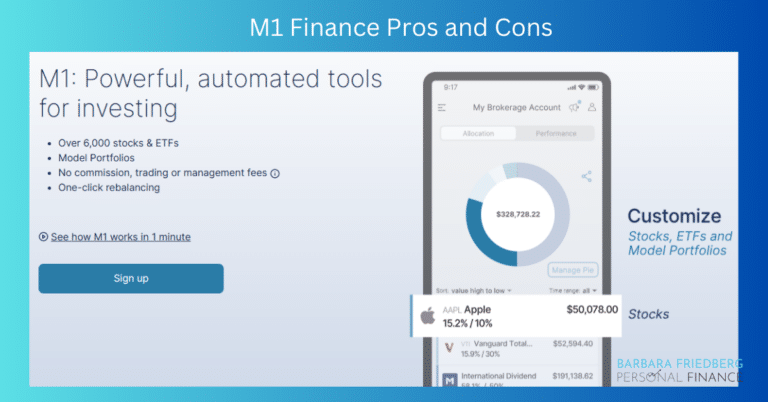

Pros And Cons Of M1 Finance

M1 Finance Pros and Cons delves into the distinguishing features of this investment app, and those that are more common. In this M1 Review and Tutorial, with video, you’ll learn whether M1 Finance is a good financial app for you, or not.