How To Figure Out the Best Asset Allocation For You

Graham from Moneystepper asks;

What metric (rule of thumb) would you recommend for asset allocation based on age and risk appetite?

Choosing your best asset allocation is not as simple as it might seem. Let’s attack it from several investment angles and throw in a bit of research as well.

What Is Asset Allocation?

The asset allocation decision divides total investable funds by percent into specific investment categories. An asset allocation represents the investor’s choice of broad asset classes and the percentages distributed across the categories.

The two most common asset classes are stocks and fixed, which includes bonds and cash.

Based upon the seminal study by Brinson, Hood, and Beebower, “Determinants of Portfolio Performance”, from the August 1986 Financial Analysts Journal, asset allocation is widely considered the largest contributor to a portfolio’s return.

In other words, the individual stocks, bonds, and funds you choose or when you buy or sell is less important to your ultimate return than the percent allocated to various asset classes. That still doesn’t answer the question, “What is the best asset allocation for you?”

If you invest in a diversified mix of 50% in stocks and 50% in bonds, your return will closely approximate the market return of 50% stocks and 50% bonds.

Asset allocation is very important because it creates portfolio diversification and reduces an investment portfolio’s risk.

Click here for free investing gifts.Adjust the Classic Advice to Find Your Best Asset Allocation

The classic asset allocation advice is very simple:

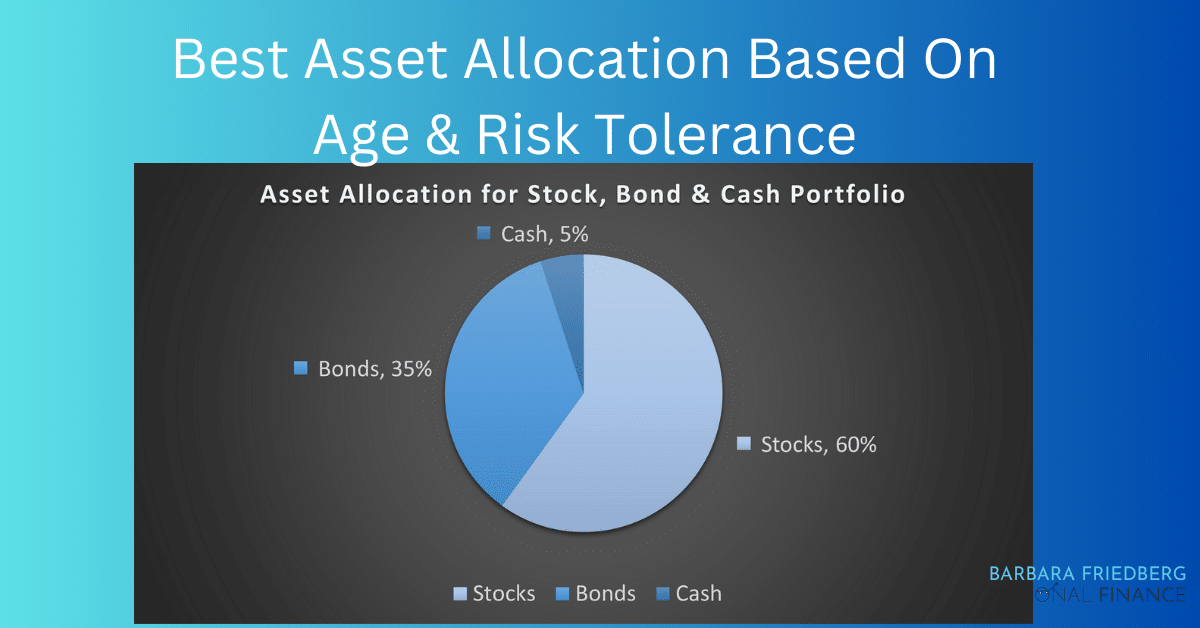

Take your age and subtract it from 100. Then invest the resultant percent in stock assets with the remaining percent in fixed assets.

If you are 40 years old, according to the classic advice, you should have 60% in stocks and 40% in fixed assets. Like the graph above. (100-40 years old=60% stock assets)

We’re living a lot longer than in the past. That’s why the updated best asset asset allocation strategy is to subtract your age from 120 and use the remainder to invest in stocks.

If you’re 50 years old, subtract that from 120 and you’re left with 70. So the new thinking suggests a typical 50 year old should have 70% of her assets in stock investments and 30% in bonds.

This advice is a good starting point, but incomplete.

If you want step by step help with asset allocation and investment management, check out low fee digital investment managers like SoFi Invest or M1 Finance.

Automatically invest for retirement with a tax-advantaged brokerage account. Custom-build your portfolio or choose a pre-made Expert Pie based on your long-term goals.Know Your Risk Tolerance

The historical wisdom suggests that if you are young, with many working years ahead, you are more risk tolerant. This theory goes on to imply that if you suffer a big loss in your investment portfolio at age 30, you have many working years ahead to replace the lost funds. Thus, younger investors are typically advised to own more stocks and less bonds since stocks offer the prospect of greater long term returns (albeit with more risk).

What happens when the market tanks?

Your portfolio = 70% Stocks and 30% Bonds

Imagine this scenario, it’s the end of 2008, you are 30 years old and your investment portfolio holds 70% stock mutual funds and 30% bond mutual funds. Your stock funds fall 33.8% (Dow Jones Average 2008 loss), the worst drop since 1931, according to an ABC News report. (And if you were especially unlucky, your General Motors stock fell 87.1%.)

2008 is an example of stomach churning investment losses.

Fortunately, the bond portfolio (proxy; Barclay’s aggregate bond index) returned 5.24% in 2008.

Thus, if you invested 70% in a Dow Jones index fund and 30% in a diversified bond index fund, your return in 2008 would have been; -22.09%. ((.70 x -.338) + (.30 x .0524))

If you had a $25,000 portfolio on January 1, 2008, on December 31, 2008 the value would have fallen to $19,478. In 2008, $5,522.50 of wealth would have vanished in one year.

Although a 22% loss isn’t great, it’s a better return than that of an all stock portfolio.

Had your stock fund been invested in a broader market index, the Standard and Poor’s 500 in 2008, your stock allocation loss would have been a whopping 36.55%.

After a quick signup, Empower will provide a FREE investment checkup:

Consider a ‘worst case scenario’ and do a gut check.

Regardless of your age, if you are extremely risk averse and cannot tolerate drops in your portfolio value, you may want a greater percentage in fixed/bond assets and a lesser percent in stocks.

Michael Kitces, a well known investment advisor and prolific writer alleges that risk tolerance is stable and can be measured. There are a variety of online risk tolerance quizzes, but equally important as taking a quiz is to imagine how you would feel if your investment values fell various percentages. Because you want to avoid one of the worst investing mistakes; to panic after a market drop, and sell. That locks in your losses and robs you of the chance to enjoy the upswing as stock and bond prices rebound.

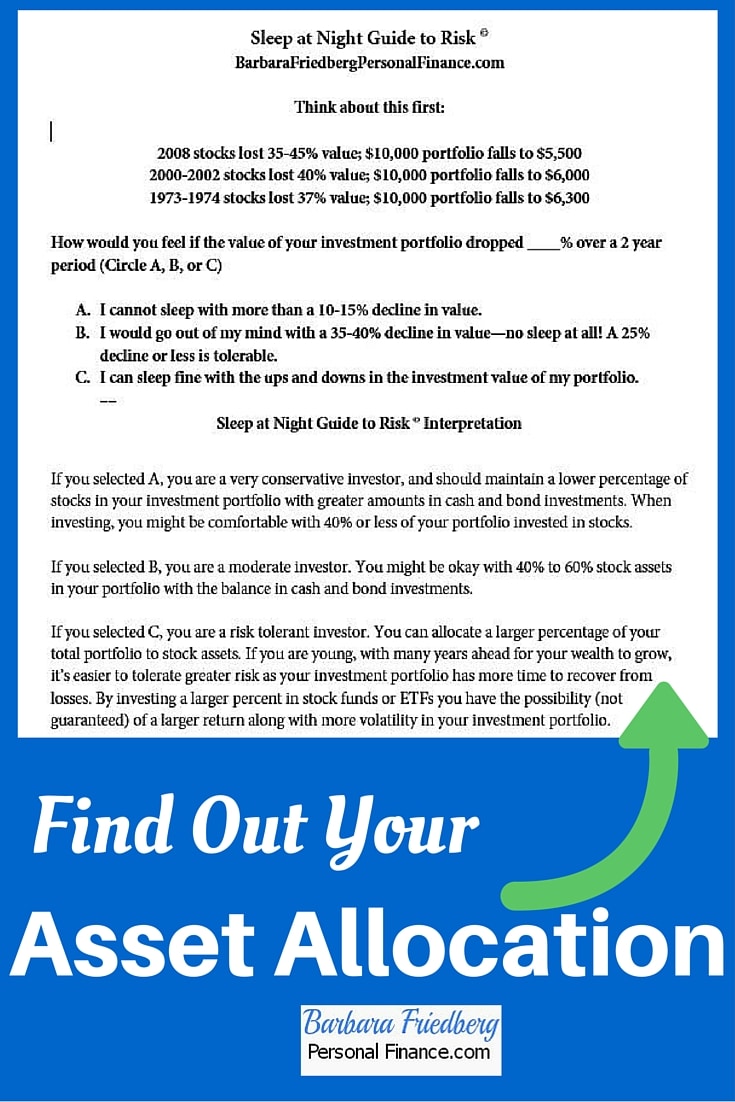

If you want a quick and easy risk tolerance measure, try my Sleep at Night Guide to Risk:

Source; Invest and Beat the Pros

Your age doesn’t always correlate with your risk tolerance.

Many young investors can’t handle all but the smallest declines in their investment portfolios. So, more risk averse investors need a greater percent in fixed assets.

What Is the Best Asset Allocation Based On Age and Risk Tolerance?

The best asset allocation for you should consider your age, risk tolerance, how long you expect to work (your human capital) as well as where you work. If you work in the investment industry, you may want to direct a lower percent towards stock investments. That’s because your job is dependent upon the financial markets. You do not want to experience a drop in your stock portfolio and a layoff because the market tanked.

If your income is erratic or uncertain, be sure to ramp up your cash investments.

If you want guidance, I’ve partnered with WiserAdvisor to offer you ready access to three vetted fee-only financial planners, in your area:

Best Asset Allocation Funds

If you’re seeking a set-it and forget-it path to asset allocation, you might consider an asset allocation fund. Within one mutual fund or exchange traded fund, you get a completely diversified portfolio of stocks and bonds. Some asset allocation funds are designed for investors with varying risk-tolerances. For example, a conservative asset allocation fund would own more fixed income and bonds and a smaller percent of stock assets. While the aggressive asset allocation fund would be stock-heavy, with only a small allotment to more conservative bond funds.

Target date funds are a distinct type of asset allocation funds. You buy a target date fund, with a date that corresponds with the year you expect to retire. If you’re 35 and expect to retire at age 65, they you’ll buy a target date 2055 fund. The fund adjusts the percentages of stocks vs bonds and fixed assets to become more conservative as the retirement date approaches. Many 401(k) and employer sponsored retirement accounts offer target date funds among their investment choices.

M1 Finance offers a range of asset allocation funds in their “expert portfolios.”

Asset Allocation Action Steps

1. Spend a bit of time understanding yourself and the markets. If you’re interested in an excellent 100 page book on investing, I recommend The Elements of Investing, by Malkiel and Ellis.

2. Take a risk tolerance quiz and assess how you will feel when your portfolio experiences an inevitable cyclical decline.

3. Create an asset allocation considering your age, risk tolerance, security of your job, and industry. If you’re job is insecure, you want lesser amounts in stocks and bonds and more in cash assets.

4. For more on this topic, click the link to read my free ebook: How to Invest and Outperform Most Fund Managers.

Bonus; Sample asset allocation investment portfolios

Related

- Strategic vs Tactical vs Dynamic Asset Allocation – Which Is Best For You?

- SoFi Relay Review – Analyze Your Investment Portfolio

- Contrast The Difference Between Short-, Medium- and Long-term Goals to Build Wealth

- Best Investing and Personal Finance Websites – Excluding Blogs

- M1 Finance Expert Pies – Which Are The Best For You?

Disclosure: Please note that this article may contain affiliate links which means that – at zero cost to you – I might earn a commission if you sign up or buy through the affiliate link. That said, I never recommend anything I don’t personally believe is valuable.

Empower Advisors Corporation (“PCAC”) compensates Wealth Media, LLC. (“Company”) for new leads. Wealth Media is not an investment client of PCAC.